Two of the top media / research firm in the climate space are Canary Media and CleanTech VC. They collaborate to publish market and fundraising statistics on a semi-annual basis. Today they released their 1H 2023 results, and the figures are below.

Here are some of the takeaways:

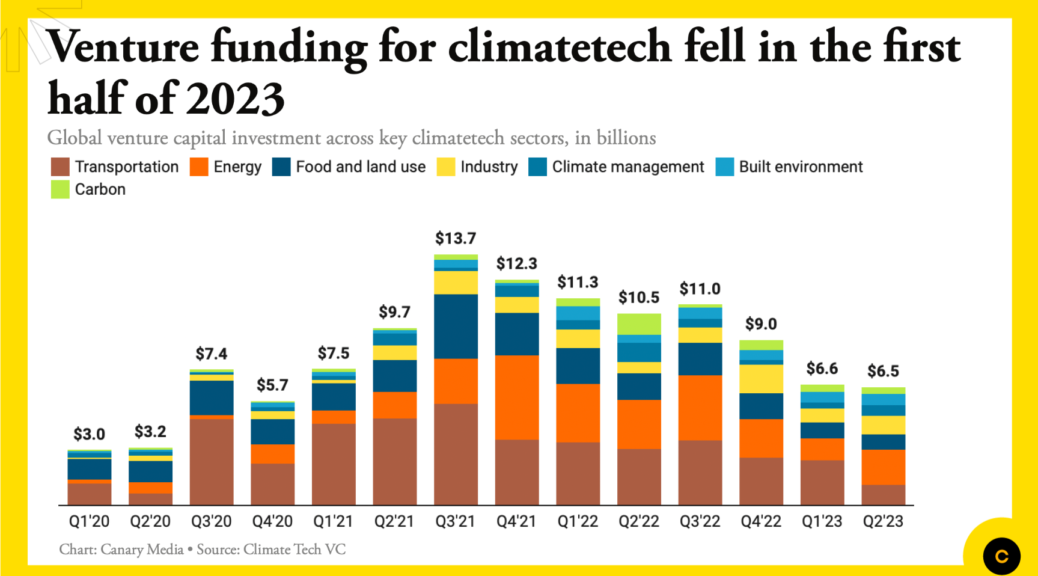

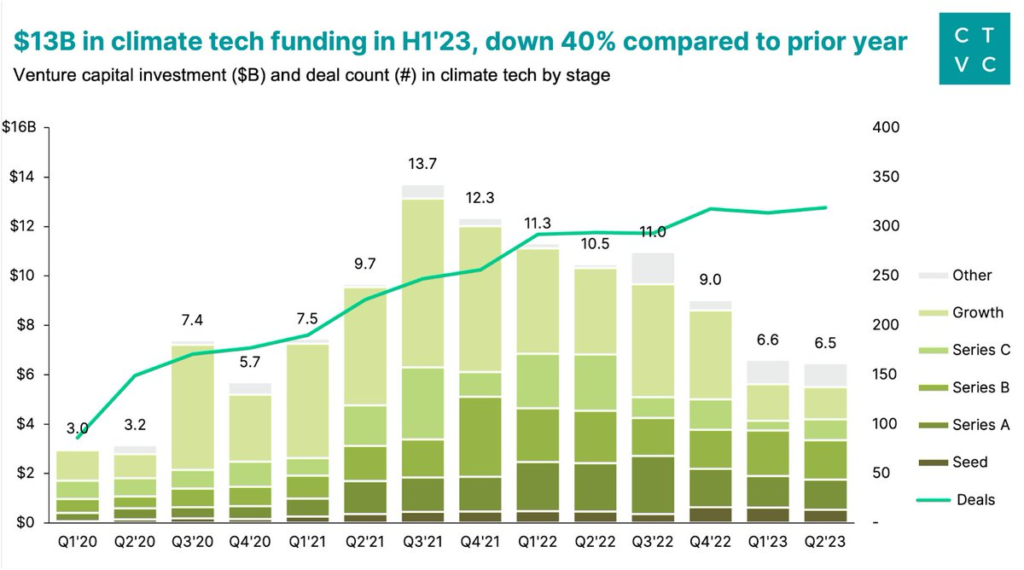

Climate tech venture funding totaled $13.1B in H1 2023. Compared to H1’22:

Total funding down 40%

Overall deal count increased 8%

Growth funding plummeted 64%

Seed funding grew 23%

Average deal size decreased 44%

These trends are consistent with what I have been seeing in the market. The growth/late stage market is effectively shut down and the larger crowd has moved to seed. As someone who has been in the space long enough, this isn’t a new trend when the market gets hard. But the second order affect is that the technologies that can deliver financial and impact return today or in the near-term are all in the growth stage, and those firms are likely to be starved of the capital they need to reach scale. I’ve covered this here and directly with our LPs… and 2H 2023 will be one to watch closely.

Capital Goods Valuations – Current Market Disconnect

The climate sector currently has several private companies attempting to raise enormous funding rounds. Most of these companies raised $100-500M as recently as 12 months ago and are back in market already for similar, or larger rounds. Why? At their core, these climate companies are capital goods business with heavy capex requirements… for example: businesses that are building battery factories recycling factories, battery assembly plants, solar facilities, new hydrogen or nuclear related equipment. The ambitions are admirable, but the buzz-saw of the current market is not being kind to the raises and we are seeing “pay for play” provisions return and heavy preference stacks being offered to entice new investors into these deals. I’ve rarely seen that work out well…

I was speaking with the Head of Corporate Development at a Fortune 50 company this past week. His company has exposure and interest in the climate sector and is a likely acquirer for some of these emerging capex-type products. The firm had seen many of the prospective rounds and his commentary really struck a chord:

“These are all capital goods or industrial machinery businesses. The private market is valuing them like technology companies… 5-10x 2028E revenues…. but if these companies commercially succeed, and only a few of them will, we would look to buy them for the standard capital goods valuation levels… 6-8x EBITDA… and the disconnect between the current valuations and the success-dependent fair market value is already too wide”

We spoke for a bit longer, but the general takeaway was clear: just because a product is new & shiny, does not mean the business model or the eventual valuation, will settle in a different range than the underlying business model. Manufacturing and industrial businesses, whether for EV batteries or regular industrial products, settle around that 5-8x EBITDA multiple when achieving scale.

Last week Blackstone announced another capital infusion into Invenergy. I’ve written about Invenergy in the past for a few reasons: firstly, Invenergy is the largest privately held renewable energy developer and represents the best of the energy transition. The company now manages over $50 billion of assets and is taking on increasingly larger ambitions. Secondly, Energize is fortunate to have access to Invenergy engineers when we evaluate specific software solutions that will could help scale the sustainability movement. We also have Michael Polsky (cofounder & CEO) and Jim Murphy (cofounder & President) of Invenergy as members of Energize’s investment committee alongside me and Katie McClain.

The Invenergy story is increasingly exciting. Why? In addition to the mammoth wind, solar & battery renewables business, the company has recently launched a…

multi-billion dollar transmission business,

multi-billion dollar offshore wind business,

Illuminate: a $600M JV with LONGI to make 5GW of solar panels annually in Ohio

Reactivate: a high growth community solar platform, targeting 3GW of deployed assets by 2030

a hydrogen concept

This investment is in addition to the $3 billion investment from late 2021 and Invenergy’s scale represents the overall new opportunities emerging in the energy transition.

The energy transition is just beginning. I’ve covered here before how wind and (especially) solar have seen massive step-ups in deployment scale over the past decade. That scale was driven by:

a) select technological innovations

b) increased investment in capital goods factories to deliver the necessary materials

c) improved utilization of software to lower soft costs, manage scale

These three actions resulted in 90%+ cost declines of key energy technologies, and the lower costs brought these energy solutions to cost parity (or better) than hydrocarbon solutions, resulting in big deployment figures.

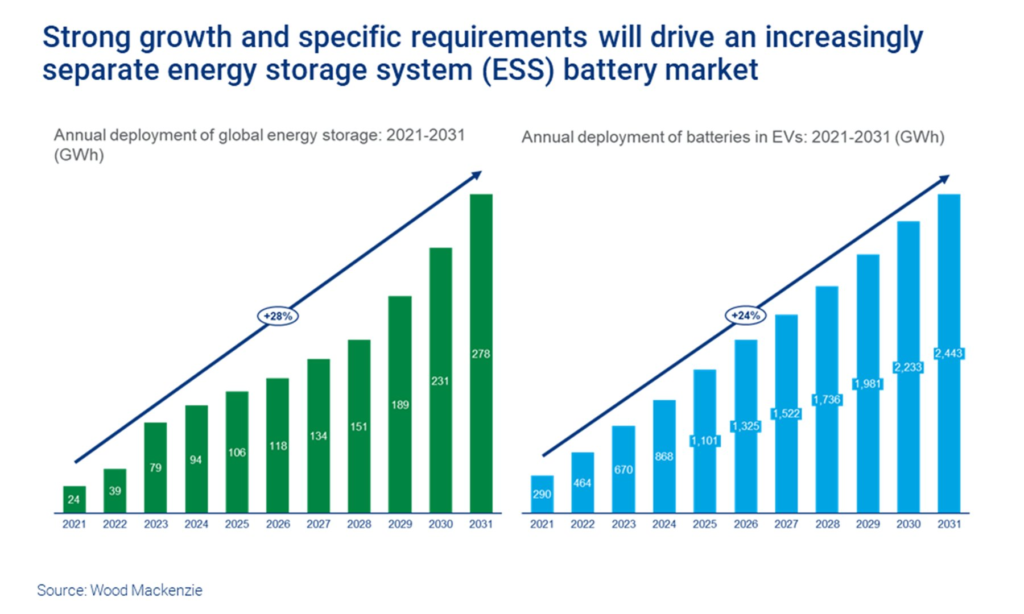

If solar is the story of the 2020s, then solar & batteries will be the energy transition narrative of the late 2020s and 2030s. EV batteries and storage batteries are starting from a small scale today but the absolute % growth that is planned for the asset type is going to alter the entire energy system. I saw a few graphs this week that reveal this scale, and wanted to share:

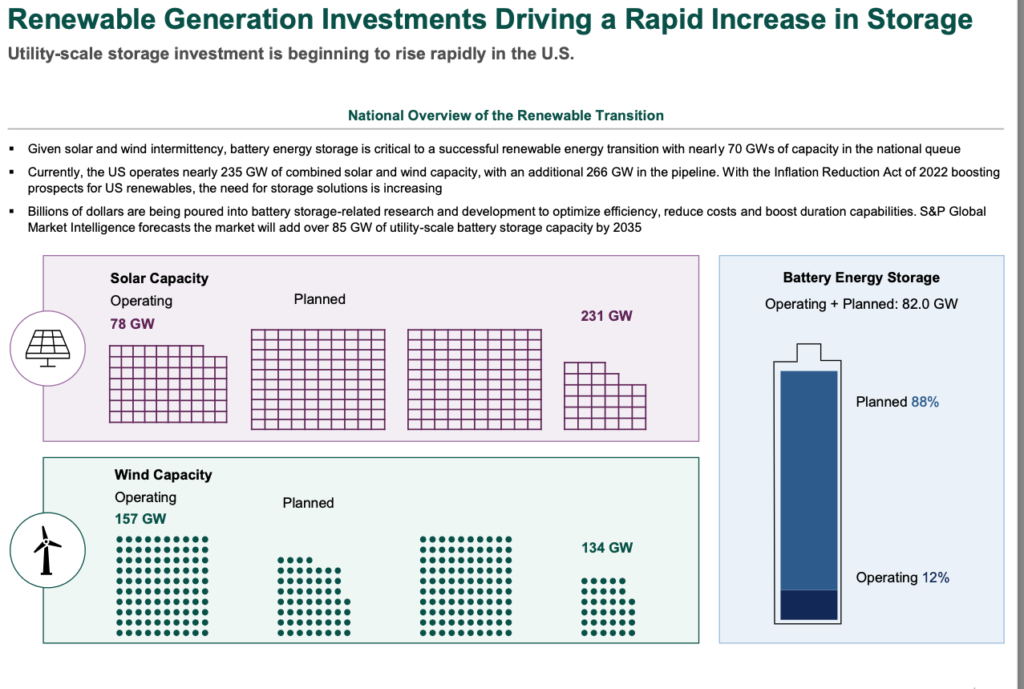

The top chart is from a Greenhill report, and shows that 78 GW of solar are installed in the US, and 231 GW are in the process of being installed, or 25% of total pipeline is actually in the ground today. When running a similar analysis for batteries, only 10 GW of batteries are in the ground today, but 72 GW are under development. When comparing that data with the bottom chart from Wood Mackenzie, you can see the true scale of the global battery market as all economies move to adopt and integrate energy storage and electric vehicles into their energy footprint.

To put the Wood Mackenzie report in perspective: today, there is 160 GW of battery storage globally. We are now adding that much stationary storage every 2 to 2.5 years and by 2029 will be adding more capacity annually than our existing volumes. Importantly, those figures do NOT include the chart on the right. This chart shows the scale of batteries in EVs and software defined systems will help those batteries become grid resources as well. At Energize we love these tailwinds and believe the distributed and controllable battery assets are perfect candidates for our digital thesis. Should be fun to watch this play out over the next decade.

Making Climate Software Tangible: ZEDEDA and new Mobility

Energize and Lux Capital co-led the Series A investment in ZEDEDA back in 2018. ZEDEDA is a technology infrastructure company that helps deliver cloud-level applications to the edge of the network. Why did we make the investment? The desktop worker is fortunate to have a computer with continuous WiFi and a computer powerful enough to handle local apps and internet to access the cloud.

Edge devices are usually independent and isolated machines that have low, local compute, poor IT infrastructure, and low connectivity to central HQ. As an infrastructure IT company, most of our impact-focused Limited Partners wanted more detail on how this tool helps enable a more sustainable future.

4+ years into the investment and many of those examples have emerged and I want to highlight two of them:

1- The gearbox in a wind turbine is very valuable asset. It sounds rudimentary, but the noise (clanks, bangs, friction) the gearbox makes is the simplest way to know the health of the asset. So how does a utility or energy operator listen to a gearbox from a thousand miles away? Simple: you put a small microphone inside the wind turbine’s gearbox area, and control it through a ZEDEDA node controller. This way, the O&M team at central HQ can turn on/off the microphone remotely…. and when “on” the ZEDEDA node controller can also run an “analytics app” on it locally that matches sound patters with fault issues… all digitally and automatically. The node then send back basic intel (limited by remote bandwidth!) and keeps preventative maintenance on track. The energy transition is increasingly decentralized and remote, and the ability to engage with and analyze these assets without having to deploy expensive engineers helps lower costs and increase safety. ZEDEDA helps deliver this edge architecture, and BIG energy companies use this software around the world for similar use cases.

2- The modern car is a computer. The pace of change from analog to digital is being accelerated with the electrification of mobility as OEMs are re-thinking their entire architecture. A major OEM is deploying ZEDEDA edge architecture across every dealership to help automate “over the air” software updates for vehicles in a more simple, and less invasive way. This is meant to deliver a better experience for EV drivers, further enabling the energy transition.

In summary, ZEDEDA is invisible to most people in the energy transition, but their technology is a key part of the new digital backbone for sustainability-focused corporates.

A couple months back I was on the “Entrepreneurs for Impact” podcast with Chris Wedding. At the end of the call he asked who else he should speak with, and we mentioned Mike at DroneDeploy and Casper at Monta. Well, Mike and Casper agreed and their podcasts were similarly released over the last few weeks. I think they are both worth listening to, and the links / summaries are below.

– Why he was happy to have an angry customer in the early days – How drones can help reduce costs for climate and renewable energy solutions – What a digital twin is and why they matter – How they’re making work on critical infrastructure safer, quicker, and more productive by avoiding dull, dirty, and dangerous work – How his love of remote control helicopters and a trip to South Africa helped start this business – The role of timing in determining the success of a startup – How AI and robots can make us superhuman – How to procrastinate in a productive way

Casper, Monta

Here is a link to Casper’s episode, they talk about: – How he grew his company from 0 to 150+ employees in just over 2 years – What led investors to commit more than $60M to his company’s growth – Why Monta aims to be the “Android of EV charging software” – How their technology allows EV owners to optimize for the lowest power cost and GHG emissions for their charging – Various hypotheses that they tried and abandoned for the current business model – How beer among the early team at a summer house led to the core values they have today – What radical transparency means for them around salary, equity, and financial disclosure to all employees – Why half of the team is focused on R&D and innovation – What led to EVs being 50-90% of new car purchases in Denmark, Sweden, and Norway

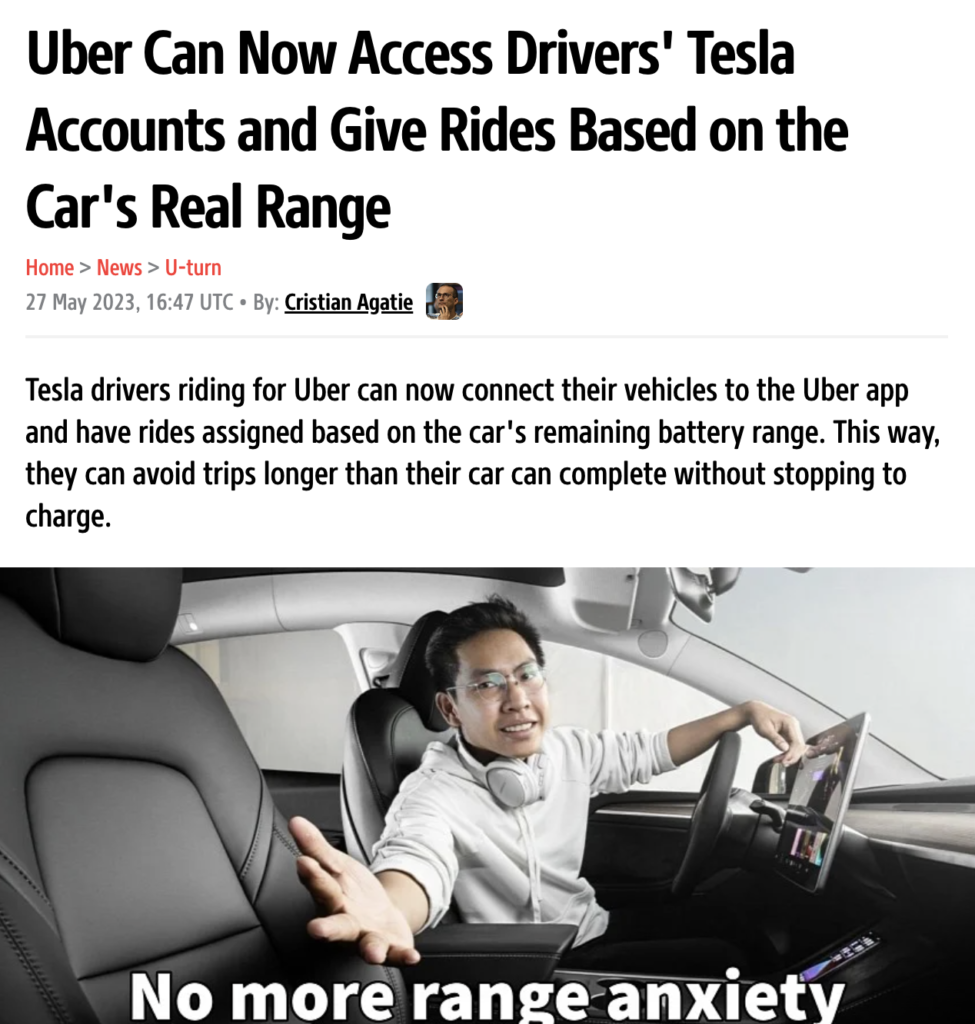

Making Climate Software Tangible: Smartcar and…. Uber!

Energize led the $24M Series B into Smartcar in January 2022. We had performed extensive research on how innovation in the mobility landscape could enable the electrification of mobility. Ultimately we wanted to identify and invest in a software company that served as many stakeholders in the mobility space as possible. We felt there would be several bespoke solutions and believed that the software that connected all parties would be valuable.

What is Smartcar? As they define it… Smartcar is leading the way to open up access to those APIs, powering a new community of innovators in the mobility space.

When you read that sentence, the energy / electrification / sustainability movement does not immediately jump out. And yet, we saw the roadmap to those solutions. This week, one of the applications we knew was on the horizon was finally revealed! Uber intends for their entire fleet to be electric. About 5% of rides today are electric and those used to be planned irregardless of the state of battery charge for the EV driver. The announcement this week is that Uber now connects with the driver’s electric vehicles to match trip length with battery charge & availability… and that communications protocol is all done through Smartcar.

In addition to that type of announcement the company has built the communications and control layer for several EV charging applications that utilities, building owners, and fleet managers leverage to integrate, manage, and optimize EV charging.

In addition to the charging management applications, the company is also the communications layer for several of the emerging EV charging networks themselves. Network use cases include helping customers make reservations, understanding state of charge, and proximity to charger are all shared (with customer approval) through Smartcar.

Smartcar is truly the digital communication highways for the EV movement. This is how an API company is accelerating sustainability.

We have some investments in the climate software arena that are very tangible combinations of digital and climate: Aurora Solar designing rooftop solar, Patch as a marketplace for the carbon markets, etc.

We also have a few investments at that “digital X climate” intersection where the climate connection is harder to grasp. These companies tend to be more “digital infrastructure” and the pipes behind the emerging asset owners, managers, or parties driving new business model innovation. When we make these investments, some of our more climate focused LPs tend to scratch their heads. But these companies are equally important in the sustainability transition and we now have the data and commercial progress to prove those initial expectations. Examples from the portfolio include:

Smartcar: API platform for the connected car

DroneDeploy: reality capture platform (air, ground) and analytics

Sitetracker: project management and deployment software for decentralized assets

Nozomi Networks: OT cybersecurity for connected assets

Handle: payments flow for construction

Beekeeper: frontline employee communications and engagement

I’m going to cover these companies and their sustainability use cases in the next few weeks. In some customer/industry cases, I am happy that Energize had the foresight to see how emerging technology could be leverages in the sustainability markets. In other cases, the use cases ended up different than even we expected! Overall, should be an interesting topic.

JT

Pragmatism executed at speed better than perfection delivered too late

Last week I was fortunate to be part of the Morgan Stanley Sustainable Finance conference. My conversation was a fireside chat with a leading executive at Morgan Stanley and the topic was “Climate Earthshots”.

MS defines Earthshots as more realistic, near-term versions of pie-in-the-sky moonshots. The topics included: 1- Potential scale of technologies that are available today: solar, batteries, wind 2- Nascent but enduring trends: electrification of mobility, carbon markets 3- Emerging solutions: hydrogen, renewable natural gas, fusion, geothermal 4- Blockers to accelerating the sustainability movement: permits, labor, soft costs, cost of capital, risk-off mentalit 5- The opportunities enabled by emerging technologies, like AI and LLM

During the Q&A section I shared my position that non-presently-operating technologies (non-industrial hydrogen, fusion, direct air capture, etc.) are nowhere near market readiness and cost feasibility. After the discussion one of the members of the audience claimed “rare for a climate investor to be so bearish”…

I don’t get swayed by frothy, hopeful headlines and I am fortunate that Energize has access to public and private datasets on the state of the sustainability market. Based on that data I believe the current environment (higher interest rates, recessionary indications, lighter private funding) moves 5 year technology targets to 10 years. But I don’t view this approach as negative because I believe the inverse to the current market opportunity is also true: technologies that are here TODAY are going to be the runaway leaders and far greater scale than anyone imagined. Batteries, solar, wind, industrial IoT technologies,nature-based carbon markets, electrification of mobility, decentralized asset development and management. These technologies are all here today and they now enjoy another 5-10 years of iteration and improvement. The future technologies are not competing with the cost of today’s technologies, but the cost curve of those solutions in a decade. This framework is why I have been using one of my management techniques to discuss the current approach to investing in sustainability: “pragmatism executed at speed is better than perfection delivered too late”…

Last summer, Energize released our comprehensive “Electrifying Everything” investment thesis, including our proprietary deep dive research report, the culmination of our 10-part blog series and our list of the top 30 software innovators applying digital solutions to help accelerate widespread electrification. In brief, we believe electrifying everything – and powering those electrons with zero-carbon clean energy – is the optimal near-term strategy to achieve decarbonization. And we believe the software companies helping deploy electrification technologies (from solar panels to electric vehicles) faster and more efficiently are in a prime position to grow their enterprise value.

Of course, anyone who has been following the markets in the last year knows that the startup and technology environment has been turbulent. So how has the landscape of companies “Electrifying Everything” changed in the last year? And how have the climate software companies from our class of 2022 fared? Roughly 12 months later, we’ve revisited our thesis and added 11 new companies to our list in the 2023 Edition of “Electrifying Everything.”

Download the full report here, and read on for a snapshot of the report’s insights.

Energize’s Top 30 Software Innovators of 2022: Where Are They Now?

Despite the last year’s challenging market environment, the climate software sector has shown remarkable resilience. Look no further than our “Top 30 Software Innovators of 2022” list for substantiation. Based on The BVP Nasdaq Emerging Cloud Index’s metrics, the performance of emerging public cloud software providers across the industry has decreased by 24.6 percent year over year, while the performance of the median company on our top 30 list has increased 140 percent. All 30 companies remain in operation, and many have achieved significant performance milestones.

Additionally, in the past 12 months, our 2022 Top 30 cohort:

– Raised $1.8 billion in total capital.

– Had a median YoY valuation increase of 2.4x.

– Achieved an aggregate enterprise value of $19 billion.

Source: PitchBook, Publicly Available Company Filings, Energize Internal Analysis

This resiliency was also evident across the broader market. Software companies launched new products and partnerships that are quickening the pace of electrification, from Aurora Solar’s integration with Mosaic to streamline solar sales and project financing, to Voltus’ and Resideo’s demand response program expansion, to Monta’s partnership with Fastned to make electric vehicle (EV) charging more accessible throughout Europe. And despite a downturn for M&A activity at the macroeconomic level, “Electrifying Everything” companies were involved in eight major acquisitions – either as the strategic acquirer or the acquired – within the last year alone.

Source: PitchBook, Energize Internal Analysis

How Software is Electrifying Everything: Energize’s Top Five Themes of 2023

As we look ahead to the next year, we believe the urgency and opportunity for climate software innovators remains, though with new considerations given the current conditions of the climate tech market. At Energize, we’ve identified five top themes that we’re watching as we evaluate the most promising software companies powering climate innovation.

1. Clean energy installers and developers are now heavyweight software buyers.

As renewables installers and developers increasingly outsource functions like project design and management to third parties, companies that offer automated and scalable software solutions for renewables – like PVcase and Pexapark – are quickly growing their revenues and total addressable markets (TAMs). We are seeing renewable energy customers purchase multimillion annual contract value software deals with increasing frequency within our portfolio and the companies we evaluate. Meanwhile, these contracts are expanding at a rapid clip – the top five renewable energy and EV customers for four of our portfolio companies expanded their contracts by 845 percent over the past five years!

2. High interest rate environments put CFO offices in the limelight.

The cost of capital has surged throughout the last year, highlighting the value of technology that can help reduce financing and transaction costs and risks. According to internal analysis, we estimate that a sustained high interest rate environment of more than four percent could add 25 to 40 percent lifecycle costs for electrification projects. And as shakeups in the banking sector continue to underscore the need for fintech innovation, we believe the potential for sustainable infrastructure project finance software like Banyan Infrastructure (an Energize portfolio company), Perl Street and Odyssey shines even brighter.

3. The “soaring soft costs” challenge is replicating across energy technologies.

U.S. residential solar soft costs remain stubborn at 65 percent of upfront costs. The cost breakdown for EV charging is no better – we estimate 80 percent of project costs in EV charging are driven by soft costs. We hypothesize that virtual power plants (VPPs) and residential heat pumps will be the next two emerging electrification technologies to face rising soft costs alongside declining unit costs (for a complete breakdown, see Energize’s mental model for energy technology innovation cycles). Software companies that automate time- and labor-intensive processes in these markets to drive down costs – like Sealed – will be increasingly valued.

4. Interconnection and siting challenges open the door for software solutions.

Bottlenecks from long interconnection queues and intensive pre-construction processes are currently slowing the pace of renewables deployment. We believe companies that can help open the floodgates by increasing transmission capacity and simplifying site assessments will be rewarded. We have now seen numerous examples of how transmission grid enhancing technologies (GETs) could increase available transmission capacity by 50 to 100 percent (or more) at minimal cost. Climate software companies like Neara are already stepping up to provide streamlined risk mitigation and assessment solutions.

5. Europe is the mad science lab fostering the rapid electrification of everything.

For a glimpse into the future of rapid electrification, look no further than Europe, where adoption rates of solar, EVs, heat pumps and grid flexibility markets are five to 10 years ahead of North American adoption rates. EV share of new car sales exceeds five percent in 15 separate European countries, with many above 15 to 20 percent (the U.S. crossed five percent in Q4 2021). European heat pump sales are outpacing the U.S. by more than two times. We believe the software companies helping increase the scale and efficiency of electrification technologies in these geographies – like our portfolio companies Monta and TWAICE (based in Denmark and Germany respectively) – are poised to grow alongside the booming markets they serve.

Introducing the Top 30 Software Innovators: Class of 2023

With these themes in mind, we present the full list of Energize’s Top 30 Software Innovators of 2023 across each of our “Electrifying Everything” categories. These software innovators are becoming the operating systems for economy-wide electrification. They’re helping deploy today’s climate solutions at scale, and they’re doing so while tagging themselves to top growth trends – helping tackle deployment barriers while serving high-revenue verticals and geographies. We’re excited to track their progress, and we look forward to continuing to support mass electrification throughout 2023 and beyond.

Source: Energize Internal Data

Per our election criteria, each company in the list should have the following characteristics:

Private company that has not announced intent to IPO or SPAC

Software or asset-light business model. This does not include pureplay manufacturers, novel chemical or material processors, project developers, installers, etc. but does include firms that have developed a novel software or digital architecture to scale a non-SaaS business model

Significant portion of revenue comes from “Electrifying Everything”-specific use cases

Should not be recently acquired or a subsidiary of a larger company

Should have a clear GHG (greenhouse gas) reduction impact via “Electrifying Everything”

In our belief, these firms should be most likely to achieve highest enterprise value over the course of time by internal Energize analysis

Full List of 2023 Top 30 Software Innovators in Electrifying Everything: