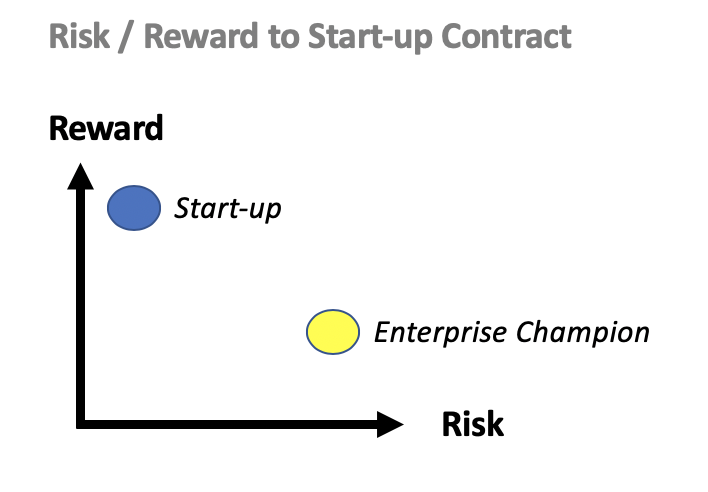

Choosing the Correct Value-Based Pricing Framework

In the low margin energy & industrial verticals, value-based pricing is a requirement. The usual $/seat pricing accustomed in software industry doesn’t work as personnel levels don’t necessarily map to the value of an operating asset. (Jake Saper at Emergence’s post about AI killing the per seat model is very relevant here!)

Learning of this nuance, many start-ups scramble to create/defend a pricing scheme and default to: “this is how much money we will save you.” Using this savings approach means the software vendors usually tie their own budgets to the operations or maintenance line items. For most markets, framing a contract’s value to an O&M budget is a huge mistake as the cost curves for the (non-regulated) energy and industrial verticals are deflationary. (h/t to Shayle Kann for helping frame here)

If a software start-up serving the industrial or unregulated energy market pegs its’ value/revenue to a declining maintenance figure, the start-up’s pricing will fall at least as fast as the cost curve. And while it is natural to hope for an increased install base to outpace the $/asset declines, history shows the budget will face intense renewal scrutiny.

Choose The Better Value Based Pricing Structure

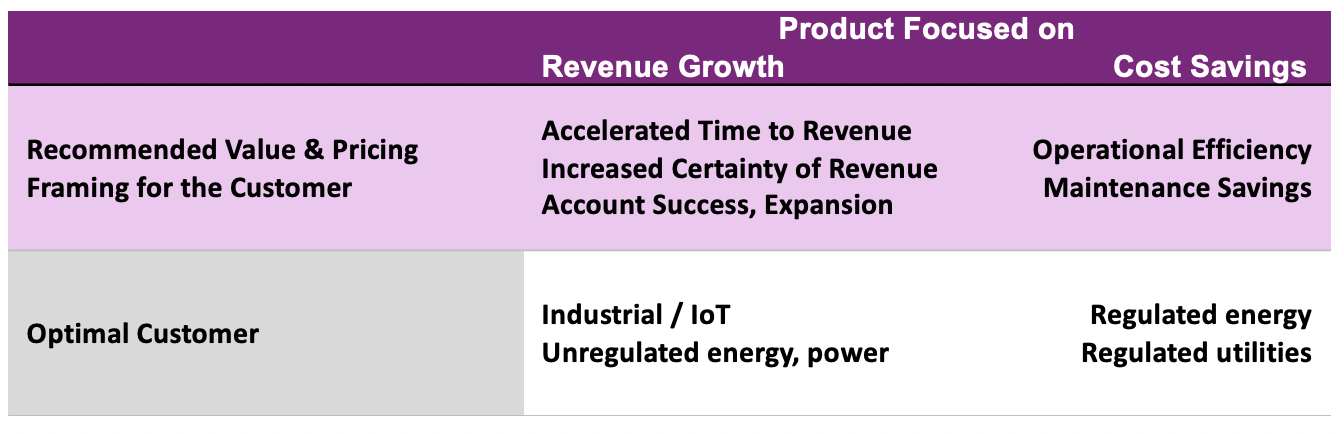

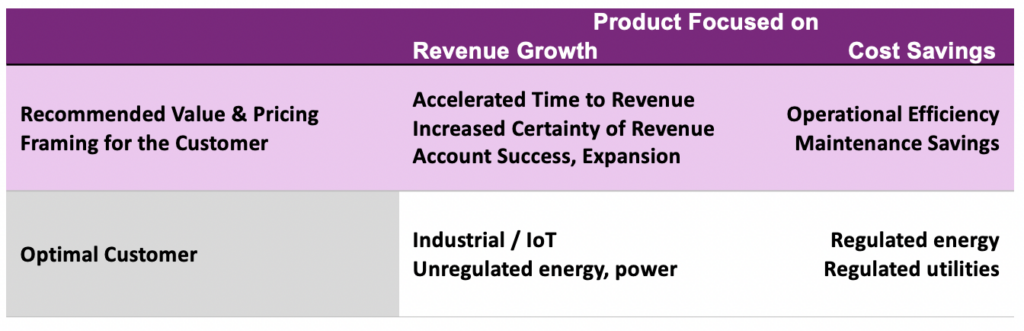

For the majority of start-ups serving the industrial, IoT and unregulated markets, I highly recommend you focus your startup’s marketing narrative and value-based pricing structures on shortening time to revenue and/or increasing certainty of revenue. POCs tied to revenue are prioritized over solutions tied to savings – even when savings are material. If a startup documents an ability to bring forward revenue for a customer, the approval process and integrations suddenly accelerate. Why? New revenue is rewarded at slow-growth F500 companies and rising corporate executives are willing to stick their neck out more for revenue, than savings.

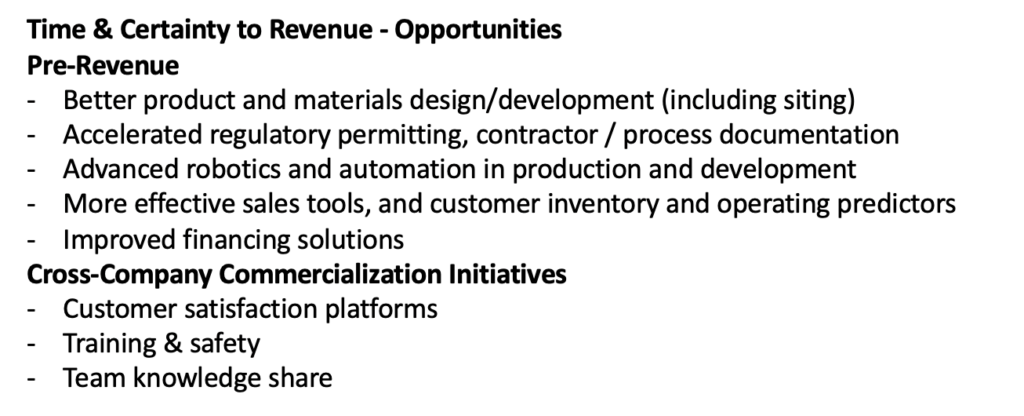

Topline alignment means that growth is good for both parties and the software subsequently faces less pricing pressure at renewal. Here are a few examples of areas that the Energize team believes software can help accelerate revenue:

In summary, in the energy & industrial space, make your topline tied to your customers. It’s more fun, anyway.

Follow-up 1: there will be a separate post on framing value for the regulated energy markets

Follow-up 2: There is a specific exemption to the rule I shared above on selling to industrial and unregulated energy. And I will be covering it tomorrow!