A few days ago a new coalition was announced. The Zeta2030 program is the Zero Emissions Transportation Association that is looking to accelerate adoption of electric vehicles here in the United States. As summarized by Axios, ZETA is calling for five key policy pillars that can, in aggregate, put American on the pathway to full EV adoption by 2030. Those pillars are listed below. Here is my take:

MY TAKE here is that this 2030 goal is likely aggressive. But most importantly, this narrative is simply the arc of our future. Whether it is 2028, 2030 or 2035… this electric transportation movement is happening. I wouldn’t have made such a bold claim even 18 months ago. But here we are: technology is driving down the costs of batteries, more countries are realizing the economic and health benefits of EVs alongside renewable energy mandates, and automakers are finally jumping two feet into the EV movement. Our charging networks are being built and utilities now have clear paths to monetize and participate in the buildout.

It is not a question of IF electric vehicles are the future of mobility. It is merely a question of WHEN the FUTURE is here. I am pleased with the logos endorsing this movement and suspect we will see many more utilities and energy transition firms added to this list in the coming months.Of note, an Energize Ventures portfolio company, Volta Charging, is on this list.

1. Outcome-driven consumer EV incentives. Point-of-sale consumer incentives drive adoption, provide cost reductions and achieve real results in pushing transportation electrification. In addition, incentivizing early retirements while encouraging EV adoption will speed the transition and meet the urgency of the moment.

2. Emissions / performance standards enabling full electrification by 2030. Emission targets are a key piece of protecting public health and sending the correct market signals to support and accelerate the transition to zero emission transportation.

3. Infrastructure investments. Strong federal charging infrastructure investments will drive the electric transportation transition and ensure that the United States is leading the way in a clean recovery where everyone is better off.

4. Domestic manufacturing. We should not only accelerate U.S. transportation electrification, but also work to ensure that we secure domestic economic growth and leadership in EV manufacturing. Federal policies must encourage job creation and economic activity across the entire EV supply chain and lifecycle, from critical materials to vehicles.

5. Federal leadership and cooperation with sub-national entities. Federal support should invest in research and development, provide an aligned vision for electrification, and ensure local leaders are empowered with the expertise and resources to support full vehicle electrification.

The 2007 movie thriller There Will be Blood portrayed the ruthless quest for wealth throughout the 1920s oil boom. Wannabe oil barons menacingly clamored for land and used any method to extract and convert crude oil to wealth.

Fast forward to 2020 and we have a new script being written as the oil industry moves from thriller to horror story: Oil demand is getting crushed by a COVID-related slowdown. The accelerating electric mobility movement is limiting demand for transportation fuels. En masse corporations are revisiting environmental impact and carbon footprint metrics. Meanwhile the everyday consumer is now face-first with a continuous barrage of oceanic and land-based climate disasters. This confluence of events is leading to an unavoidable event: messy and major consolidation amongst the traditional energy superpowers.

And here is the first move on the oilfield: Exxon should acquire BP.

These two stalwarts are down 50% year to-date. And while both stocks are being decimated by lower demand for oil and expected heavier regulations, BP offers an important lifeline to Exxon. Why?

Renewables are the future, and BP is focused on renewables. Aiming to be net zero by 2050, BP has built up the organizational structure, wind & solar assets, retail sites, and power trading capabilities to capitalize on renewables growth. Exxon doesn’t have any of these assets at scale.

Investor sentiment has declined across the O&G sector and institutions and endowments are divesting from O&G for ESG purposes. Exxon is the largest carbon emitter with no plans on changing. A “bolt on” acquisition of BP would improve ExxonMobil’s carbon footprint and improve investor ESG sentiment.

A focused subsidiary can drive internal change at the larger Exxon: in their most recent annual report, bp references “renewable”, wind, “solar” 124 times. Exxon? only 16 times.

Exxon trades at nearly 3x the scale of BP, meaning the combined company would be bolster an approximate $225 billion market capitalization.

The Energize Ventures team evaluated the prospective joint businesses by analyzing 3 key business units: Low Carbon & Renewables, Retail & Trading, and Oil & Gas framework. Mark Tomasovic brought many keen insights into how a traditional energy firm can use M&A to capitalize on the energy transition.

Renewables & Low Carbon

Wind & Solar: Exxon could operate BP Renewables as a standalone business to get exposure into the growing renewables category, improving investor sentiment, acquiring power expertise, and capitalizing on cost declines in wind & solar

BP currently owns 2.5 GW and wants to develop 20 GW of renewables by 2025

Exxon has no renewables or power generating assets in their portfolio

LNG Portfolio: BP’s strategy to becoming greener includes increasing their LNG portfolio

BP wants to increase their LNG production from 15 MTA to 30 MTA by 2030

Exxon is a leader in the LNG business with over 23 MTA of LNG globally and 4 mega projects currently being constructed

Biofuels: BP wants to increase its bioenergy portfolio to 50 kbd by 2025 to reduce emissions

Biofuel research is a strength of Exxon after announcing a gene editing breakthrough in 2017. Exxon is the only major publicly continuing to talk about biofuels and is targeting the capability to produce 10kbd of biofuels by 2025

However, many people still question if biofuels are commercially viable

Retail & Trading

Retail: BP has a strategic advantage with electric vehicle customers

BP has 10M touch-points with customers every day at 2,870 retail gas stations and 7,500 EV charge points

Exxon exited all of their retail sites in 2008. The Exxon and Mobil gas stations remain because they still license their name to retailers

Margins on BP convenience / electrification are 25% and are expected to increase to 35%

BP’s partnership with Uber and Microsoft position the company to capitalize on its EV charging and digital strategy

Trading: BP has a strong trading division for oil, gas, and power

BP’s trading division has significantly improved company top line – specifically in oil trading – and they want to 2x the size of the power trading division

Exxon has only a small trading organization and could benefit from trading expertise

Oil & Gas

1- Upstream Oil & Gas

BP and Exxon both want to high-grade their investments to the best basins and divest from old dry gas assets; the strategies are aligned here

BP wants to divest $10B of non-core oil/gas assets

Exxon wants to divest $15B of non-core oil/gas assets

Permian-Specific Assets: Exxon’s huge position in the Permian would be accretive to BP’s small position

Exxon is the third largest landowner in the Permian (1.6M acres), whereas BP only owns 83K acres

BHP Gas Assets: BP has top-tier gas assets in the Haynesville and Eagle Ford that they acquired in 2018 from BHP; these gas assets will significantly improve XTO’s net acreage position in these basins

BPX (BP’s U.S. division) and XTO (Exxon’s U.S. division) both operate as semi-autonomous organizations within BP and Exxon and would be easy to merge

2- Downstream & Chemical

Refining: BP’s refining business is performing better than Exxon’s. Combined downstream organizations will increase purchasing power, add procurement synergies, and improve the efficiencies in BP retail networks

Exxon refining margins are at historic lows and Exxon refining has not been profitable during COVID

BP refining is still profitable

Chemicals

Exxon Chemicals is still growing and profitable due to the company’s strength in plastics and olefins manufacturing

BP divested their chemical company this year, which mainly focused on aromatics and acetyls

The cheap gas from BP would certainly benefit Exxon’s $40B Grow the Gulf chemicals initiative

The energy landscape is changing, and Exxon’s acquisition of BP would provide a pathway towards owning the future of energy. Through the acquisition, Exxon would improve their base business by acquiring strategic U.S. assets while also adding exposure to renewables, retail EV charging sites, and a strong oil/gas/power trading division. During this time of consolidation in the O&G industry, Exxon can use the opportunity to bolster its core business, reduce its carbon footprint, and prepare for renewables growth. With volatile oil prices and historically low margins in O&G, the future remains unknown. But there is one thing for certain: it will be a messy transition and there will be (more) blood.

Own the Demand, Pt 2: The Energy Transition Can Learn from Amazon

This is Part 2 in my series about what it means to “own the demand”. On Wednesday I wrote Part 1: why the energy market changes are making it increasingly important for energy companies to move from a supply mindset to a demand mindset.

Summary

As the world moves to oversupply of power, the smartest energy companies will move from balancing centralized supply and demand, to providing the products and controls for decentralized customers to manage their own supply and demand.

Why?With the decentralization of energy, the customers’ energy products and energy software needs are going to quickly mirror the needs of the utilities themselves.

Therefore, I believe that the winning energy companies are going to find a way to productize their internal IP on proprietary subject matters into more modular tools for 3rd party use. The most advanced energy companies will be comfortable doing joint ventures with technology companies (or buying them) to help bring the software-specific tools into the fold. As a result, the production and load management will move to the edge. And the energy company will own the remote production and control layer.

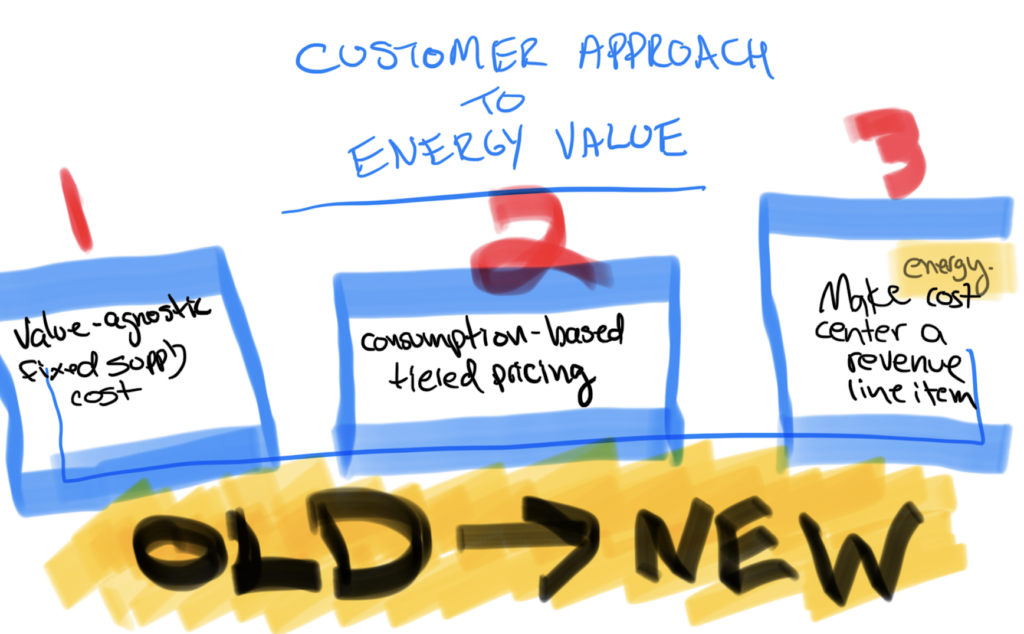

Amazon provides a great precedent here. They have taken internal cost centers, productized them, and made them available for 3rd party use and revenue.

How to Learn from Amazon

In the above graphic, energy companies currently make money in business model #1 (fixed supply price) and business model #2 (consumption-based tiered pricing). I believe that our oversupply of power is going to enable a 3rd business model: productize internal utility energy tools that are currently a cost center and distribute them as a form of new revenue. Luckily for us, there is another firm currently executing this cost center -to- revenue transition masterfully that we can learn from…

How we Learn from Amazon

The analysis (via Tweet) above was from Shai Dardashti, and showed how Amazon turned internal cost centers into productized, 3rd party tools. These repurposed technology assets met a customer need. Therefore, Amazon found a way to turn their cost centers into revenue line items. Amazon accomplished this goal because they knew their customers had the same technology needs as Amazon itself.

Given the increasing decentralization of energy, the energy products and energy software needs of customers are going to quickly mirror the needs of the utilities themselves. The types of solutions that end-consumers will start to seek include more modular and repeatable versions of the following:

Load balancing software for distributed energy management

Energy systems design and bid management: solar, battery, microgrid

Easily purchasable long-term power purchase agreements with nearby utility scale power

On-site power efficiency and weatherization modeling

Power supply optimization /cost management

Pricing mechanisms for peer::peer or 3rd party power sales

Notifications platforms for demand response for optimal pricing

Cogeneration for waste capture or other baseline support

EV charging infrastructure and systems modeling

EV charge-time management, load balancing

EV fleet logistics, charging and balancing

Power quality assurance

Outdoor and long-range network communications tools

Cybersecurity and network management controls

Easily bookable, verified and reputable operations & maintenance electricians/technicians

Decommissioning and relocation services

Utilities offer many of these services for their own assets and networks, and to their largest consuming energy customers. The utilities use these tools to help match supply and demand. As the world moves to oversupply of power, the smartest energy companies will move from balancing centralized supply and demand, to providing the controls for decentralized customers to manage their own supply and demand.

I believe that the winning energy companies are going to find a way to productize their internal IP on these subject matters into more modular tools for 3rd party use. The most advanced energy companies will be comfortable doing joint ventures with technology companies (or buying them) to help bring the software-specific tools into the fold.

A successful outcome here is to help each energy consumer manage their power load through deliverable technology. For most individuals, 1-2 of these tools will suffice. But as renewable generation, EVs and batteries become commonplace, more complex software tools and products are required to balance each edge location. For example: if a local businesses’ microgrid needs to communicate with the neighborhood battery system, a new suite of software-defined data networking tools need to be built to allow instructions to be sent between the assets. And to trust the communication layer for that network, we now need a purpose-built network management and cybersecurity tool to ensure no false signals or nefarious actors.

Over the coming days I will be walking through these examples – and specifically around one firm that has placed themselves at the center of the transition.

An Energize Theme: Electrify Everything (Guest Post from Tyler Lancaster)

The link can be found here. The original post was written by Tyler Lancaster, a Principal at Energize Ventures.

—

Electrifying Everything: The Key to Decarbonization & A More Sustainable Future

Electrification is a key theme to Energize’s investment thesis. We invest in software and business model innovations, many of which directly contribute solutions towards decarbonization by means of electrification. This is the inaugural post in a blog series where we’ll explore this critical transition and the technologies driving and enabling it.

Addressing climate change is the existential challenge for our generation — and decarbonizing human activity is an essential first step. How do we get there? Put simply: Electrify everything.

Rewiring America argues that to effectively decarbonize (limiting global temperature rise below 1.5°C, consistent with the Paris Agreement), we must electrify…everything, and power those electrons with renewable energy. What does electrifying everything look like? It’s transitioning to fully electric cars, converting home appliances like heating and air conditioning to electric heat pumps, installing efficient LED lights instead of wasteful incandescent bulbs, and even using electricity to create heat for industrial processes. Powering an electrified world with zero-carbon energy means primarily generating electricity with the sun and wind. Electrifying everything is the most important climate imperative of the next 20 years.

As an investor in clean energy technologies, I agree with Rewiring America’s thesis that electrifying everything is the most viable path towards decarbonization. Here’s why:

1. Renewable power is the only carbon-free, cost-effective solution readily available at scale today.

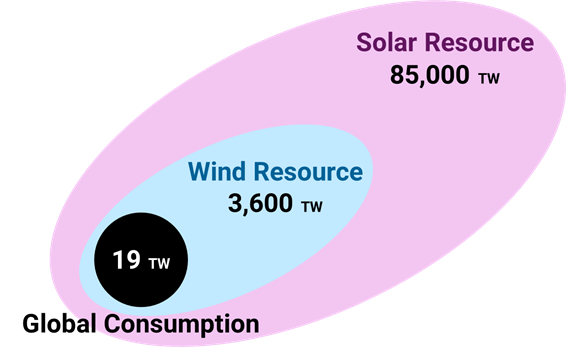

Solar and wind are highly efficient electricity production technologies that represent the largest potential energy sources available on earth. The entire human population consumes approximately 19 terawatts (TW) of energy today. The global solar resource available is 85,000 TW, or 4,500 times the current energy demand. Wind is a 3,600-TW resource, or 190 times demand. As a population, we can afford to both consume much more energy and be incredibly selective about where we put solar panels (rooftops, parking lots, deserts) and wind farms (pastures, fields), while still comfortably covering our energy needs.

Source: Rewiring America

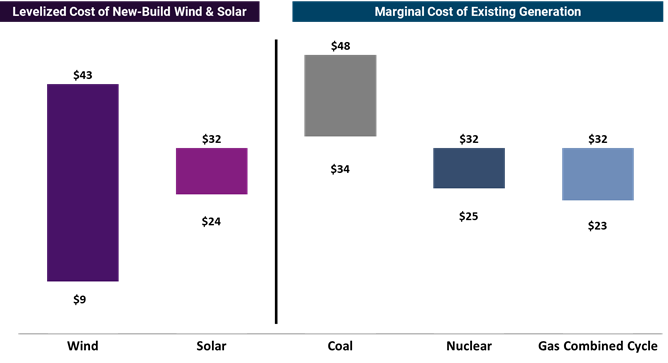

Not only are these renewable resources readily available, they’re also cost-effective. Solar and wind are now cheaper than coal, natural gas and nuclear almost everywhere. Lazard’s 2020 Levelized Cost of Energy (LCOE) update estimates in many cases, even unsubsidized solar and wind are less expensive than the marginal cost of operating existing conventional generation. Yes, that means it is cheaper to build new solar and wind systems than to continue operating fossil fuel power plants. Renewable energy’s economic lead will only grow with further innovation and scale.

Source: Lazard Levelized Cost of Energy, 2020

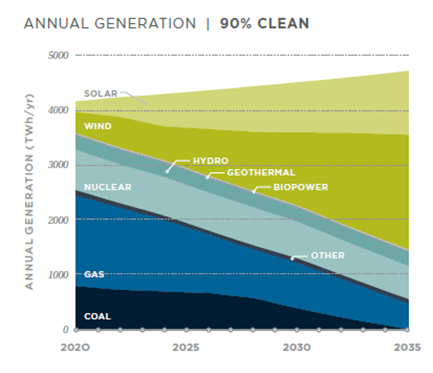

Attaining a 90+ percent clean energy power grid powered primarily with wind and solar is achievable in the next 15 years if we move quickly. Energy Innovation and Policy, an excellent nonpartisan energy and environmental policy firm, recently published the 2035 Report outlining a cost-effective pathway to 90 percent decarbonized grid by 2035. I will caveat that energy storage and flexible zero-carbon generation (hydro, geothermal and nuclear) become even more valuable — and essential — for a 90+ percent clean energy grid with increasingly large amounts of variable wind and solar. If you are interested in the tradeoff of going “all in” on solar and wind, I would encourage you to read the work of Jesse Jenkins, who has conducted extensive research on an optimized and decarbonized energy system.

What about alternatives like carbon capture, advanced nuclear, and green hydrogen? In our experience, these energy resources are not technically feasible or economic at scale today. The clean energy sector is experiencing rapid innovation, and new tools to aid the fight against climate change are emerging every day. We’re excited to add these technologies to the mix when the time is right — but wind and solar are ready to go now.

2. Electrifying everything will create a massive renewable energy economic boom.

Rewiring America estimates that electrifying everything would increase U.S. electricity demand by 3 to 4 times, from 450 GW to 1.5 to 1.8 TW. A mostly electric energy system would necessitate a massive investment in renewable generation, storage, high capacity power lines, and demand-side flexibility. As we electrify the U.S., we need to rapidly scale up investment in renewables to the tune of 1,200+ GW in new wind and solar capacity, injecting $1.7T of investment into the power grid.

The benefits of solar and wind extend beyond the direct investment. Solar and wind reduce local pollution, create jobs, generate revenue for municipalities and landowners, improve public health, increase home values, and preserve the natural landscape. Energy Innovation and Policy estimates a 90% clean power grid would support a total of 29 million job-years cumulatively from 2020 to 2035. Electrifying everything and thereby increasing electricity demand by three to four times would further multiply employment related to decarbonization efforts. The U.S. can employ a generation of workers by powering our economy with renewable electrons.

Clean energy entrepreneur Jigar Shah has argued for years that addressing climate change is the single greatest wealth creation opportunity of our lifetime, to the tune of a $10 trillion economic impact. We agree, and a growing body of interdisciplinary research is forming a clear pathway to unlocking climate wealth in the U.S. by electrifying everything — and powering everything with renewable energy.

3. There is incredible inertia in carbon-based energy consumption systems, and we must start NOW.

Shayle Kann, Managing Director at Energy Impact Partners, recently tweeted a simple framework to focus decarbonization efforts. Eighty-six percent of global greenhouse gas emissions come from five sectors: electricity and heat (25%), agriculture and land use (23%), industry (18%), transportation (14%), and buildings (6%). Decarbonize each quickly, and we are well-positioned to limit global temperature rise below 1.5°C. The problem? Today’s equipment base is heavily committed to future emissions. We need to act now by electrifying quickly.

A furnace lasts 18 years. A car or truck? 20 years. How about a power plant? 50 years. Every time we build or continue to operate a fossil fuel-consuming machine, we are creating “committed emissions” for the entire lifetime of that machine. Energy consumption systems face remarkable inertia from replacement cycles, even with exponential adoption of new technology. If we do not rapidly achieve 100% adoption of electric, renewable, zero-emission machines sooner than later, we cannot prevent global temperatures from charging past 1.5 degrees Celsius.

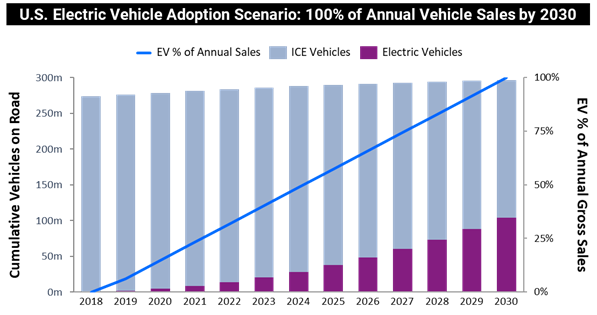

Let’s use electric vehicles (EVs) as a thought experiment. To keep things simple, we’ll assume that EV adoption as a percent of all annual vehicle sales will reach 100 percent by 2030 — much faster than even aggressive forecasts by Bloomberg New Energy Finance. To provide another baseline, we’ll use the data point that in 2018, there were approximately one million EVs in the U.S. market, making up 0.4 percent of all vehicles on the road. In our scenario, when we reach the incredible milestone in 2030 of making every new vehicle sold an EV, cumulative EV adoption would still be just 35 percent. Why? On average, vehicles are replaced once every 20 years (the average vehicle in the U.S. is now 12 years old). We currently have about 280 million gas-burning vehicles on the road. Even after achieving 100% annual EV adoption in 2030, 193 million fossil fuel combustion vehicles would remain on the road.

We have a long journey ahead to fully electrify and decarbonize the machines and equipment that make the modern economy hum. However, I am optimistic sustained market and technology tailwinds behind electric machines and renewable energy will catalyze exponential adoption. Acting now is pivotal to combat the inertia in our energy-consumption systems, from power to transportation, buildings and beyond.

What does “electrifying everything” entail for the energy and industrial start-up ecosystem?

I expect in the next 20 years, most new machines, equipment and appliances will be electric. Increasingly, electricity will be zero-carbon and renewable. Massive growth tailwinds in the U.S. and abroad will create a new class of climate unicorns, generating venture-scale returns for entrepreneurs and investors. Solutions that are technically viable, economic, and simply a better product and customer experience will capture disproportionate market share.

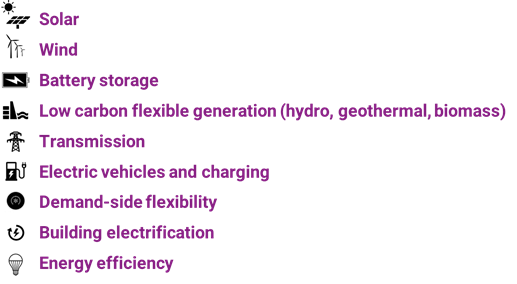

At Energize, we believe the following solutions are best poised to capitalize in the 2020’s:

Energize will continue its focus on asset-lite, software-enabled firms. We believe a multibillion enterprise value software company will be built in each of these categories in the next 20 years.

We are bullish on all nine of the above solutions to decarbonize by electrifying (everything). The ensuing blog series will dive deeper into how we believe software and business model innovation will accelerate each. In my next post, I’ll dig further into solar software…stay tuned!

The best energy firms of the future will not only control supply, but they will also have proprietary access to the demand.

This is why I say that Tesla will ultimately get into the utility business. If you control the demand you should fully integrate and capture the economics gained by controlling the entire stack. In energy there is greater aggregate value in controlling the stack than a simple sum of the parts of each component.

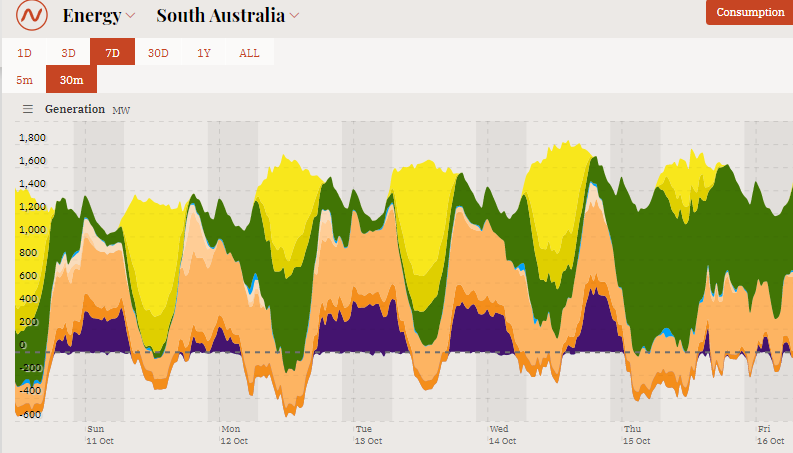

This graph below explains why: a few weeks back South Australia was ~100% solar powered on Sunday and ~100% wind powered on Thursday.

The underlying data of this graph also shows how more energy was produced than consumed and energy prices, therefore, likely went negative every night. In these events, businesses and households are PAID to consume energy.

Oversupply is the future. We can all argue whether it is 4 years, 10 years, or 20 years, but this exact chart is coming to the United States. Texas already has many days where wind power provides >60% of the load and energy prices go negative. The best firms will be able to control and collaborate with demand to always deliver electrons where marginally valuable. So how do energy companies transition to getting paid for controlling demand? First, let’s start with the basic, current status of power supply.

THE WHY

Energy is now officially a deflationary commodity. Therefore, the % contribution to an good’s overall cost is small and dropping

Consumer sentiment and awareness to power source is increasing

Power readiness and power quality is of more value

An increasing number of businesses or power-consuming assets will have timing flexibility to their energy consumption profile

Higher margin goods driving the “electrify everything” movement, such as Electric Vehicles, water heaters, and air conditioners have the majority of their variable expense come from power cost

Tomorrow I am going to reference the “HOW” and cover a precedent example already underway in the technology ecosystem.

I recently wrote a post about Honeywell’s digital aspirations. The anchor to the digital transformation is Honeywell Connected Enterprise’s ‘Forge’ Product. The Forge Product is an enterprise performance management system meant to be an operating model for industry. I wrote my post about Honeywell here: Hungry Honeywell.

I also recently wrote about Microsoft’s “Energy Wildcatter” presence. Microsoft is partnering up with the leading firms of the energy landscape. Through a mix of power purchase agreements and algorithmic treaties, Microsoft is locking in its’ IT operating system within the new energy OT environment. The moves are very smart. The article can be found here: Microsoft the Surprise Wildcatter.

Well, the two firms are now colliding. Honeywell has selected Microsoft’s Azure cloud platform and Dynamics 365 Field Service platform architecture to be the backbone of Honeywell Forge. This move makes sense for two key reasons:

1- Microsoft suite tools are already the standard IT platform for most energy, industrial and manufacturing customers that Honeywell serves. Defaulting to Microsoft is really just meeting the customer where the customer already is…

2- Honeywell is a leader in OT. Pairing subject matter expertise in OT with the traditional leader in IT brings topical and architectural expertise together.

The initial use cases where Honeywell and Microsoft will collaborate are on: digitized maintenance, energy optimization, and OT cybersecurity. Energy & industrial customers are quite savvy on these topics and the market is ready for them now – meaning these should be good launching points for the Forge-Azure partnership.

Finally, this move is very smart for Microsoft. They are clearly not intent just being a player in the energy transformation. Microsoft has set its’ sight on being the IT backbone for the industrial transformation as well. This Honeywell contract and the downstream effect for how Honeywell and their customers are committing to the Azure framework will pay dividends to Microsoft for decades to come…

This week I learned about a wind farm shutting down because a portion of the blade fell off. And it made me realize how different and minimal our future “energy disasters” will be versus our existing carbon-based energy disasters.

Yes, EV fires are scary get some local press. And yes, a derecho or tornado may take out parts of a wind farm.

But the fact is that highly decentralized, lower cost assets make for less dramatic downside events. And less volatile commodity extraction, operating and transportation conditions make for lower impact disasters.

Reading the news about how parts of a wind blade fell off isn’t great. But if that system error is the new type of our new energy “disaster” then we are going to be alright. In addition to more isolated impact, our more distributed system has far greater redundancy than our legacy energy infrastructure.

How it Started vs How it Ended

Distributed Assets = Better and More Accessible Software

Software that serves the physical environment is usually highly customized. For every $1 of software sold, there is anywhere from $1 to $10 of accompanying implementation and professional services revenue.

Just how much money gets spent in customization?

The average utility has an asset management platform contract that costs $20 million + per year. These asset platforms track everything from substations to big power plants and much of the data is static upon entry. Contracts are usually a baseline price for the software and then tens of thousands of hours of pre-booked professional services. The existing leaders in this asset management space are IBM Maximo, Oracle Primavera, or Infor ERP. These firms offer both the software and the professional services revenue.

Like the long-standing assets they manage, these software platforms are not built for iteration. This is why Energize is incredibly bullish on new asset management platforms like Sitetracker that are purpose-built for more distributed assets. Energy and industrial customers require a new software experience. In the past, critical infrastructure execs looked to solve problems by adding more people and billable hours. The tide is turning. Now the default in the energy and industrial verticals is to attempt to solve a problem with software.

Platforms like Sitetracker (and others) all bring world-class asset management solutions to the new asset bases with an easier onboarding schedule and a lower price-point. These suites are also all built with newer technology stacks allowing for faster iteration and response to customer needs. And the best of these new solutions are enabling applications to integrate with their workflows. Want a predictive AI application for your engine? Here is SparkCognition. How about computer vision detection for QA? Check out Matroid. Worker safety and communications? Beekeeper hits the mark, Just check the box and new applications integrate into field operations. This is the future, happening now. New software giants will take over the asset management vertical.

Better software and faster feedback cycles will drive greater efficiency in our operating environment. It will be a fun space to watch over the coming years.

Yesterday I mentioned how there is an increasingly special group of software companies laying the digital groundwork for the OT market.

With each Energize investment we do our best to put together a framework on market size and near-term opportunity for our prospective investments. Looking back at our Fund 1 portfolio companies there are now a few, clear examples where we underestimated the TAM.

The top 3 consistent themes for underestimating TAM are:

1- Product-led growth allowed the companies to expand into other soft-cost opportunities in the vertical

2- Situational-driven budget expansion as a forcing function to try new products to maintain business operations (COVID, workforce turnover, etc.)

3- Distribution channels built into product accelerate go to market and open up new verticals

Notably, there is no “a-ha” moment from a customer group. Markets get unlocked as small wins compound, team grit persists, and effort-driven “luck”all collide. As the tailwinds for the energy and industrial verticals continue to blow, the winning firms are going to be the ones that continue to iterate and hustle as the market develops.