Over the past few months I have seen a few software companies serving the energy and industrial verticals with this head-turning profile:

+ $5-10M of revenue

+ >200% YoY revenue growth

+ Profitable

+ Sizable cash balance

My first thought when seeing these companies? Wow, this scale of efficient growth wasn’t happening before.

My second thought: This firm won’t be raising money, right?Wrong.

COVID changed the energy and industrial verticals. All software purchases are accelerating and new budgets are being formed and consumed. The smartest start-ups realize that these energy & industrial software relationships could extend decades.

These digital-focused start-ups have two early advantages that compound:

access to historically buried and undiscovered data assets that are revealed as firms move from analog to digital-first operations

license for product-driven growth as industry’s new knowledge workers realize the potential to digitize industry’s soft costs

Given the potential to entrench within the customer and iterate with non-transferable assets, software firms serving the energy and industrial vertical are attracting new investors. These investors, it seems, believe that there is potential for the Law of Accelerating Returns in heavy industry’s digital layer. In this structure, winning companies far escape their peers and should continue to invest early and often to capture market share to solidify the #1 market position. I have seen this accelerating return profile in other verticals, but it is a relatively new phenomenon for software companies serving the historically analog verticals.

As a result, the race is on to build the new software operating platforms for the Operating Technology network. I suspect we are at the beginning of a 10-year+ trend in this purchasing cycle and there will be many head-turning financing rounds in the coming quarters for software companies addressing this theme.

The ‘Goodwill to Income’ Framework: Being Early isn’t the Same as Being Wrong

In start-ups there is a common phrase: “being early is the same as being wrong“

That statement is wrong.

Here is a correct version of that phrase: “Being early and spending like you are on-time is the same as being wrong”

From an entrepreneur’s perspective: if you are passionate about a space and you want to dedicate a portion/majority/all of your professional career to an opportunity, then being “early” is just the learning process. Perfecting the skillset or complementing the knowledge base as the opportunity evolves. The early stages are where you can compound domain expertise and network advantages.

From a VC perspective: being early is being wrong only if VCs overcapitalize the business due to HOPING the market is ready now.

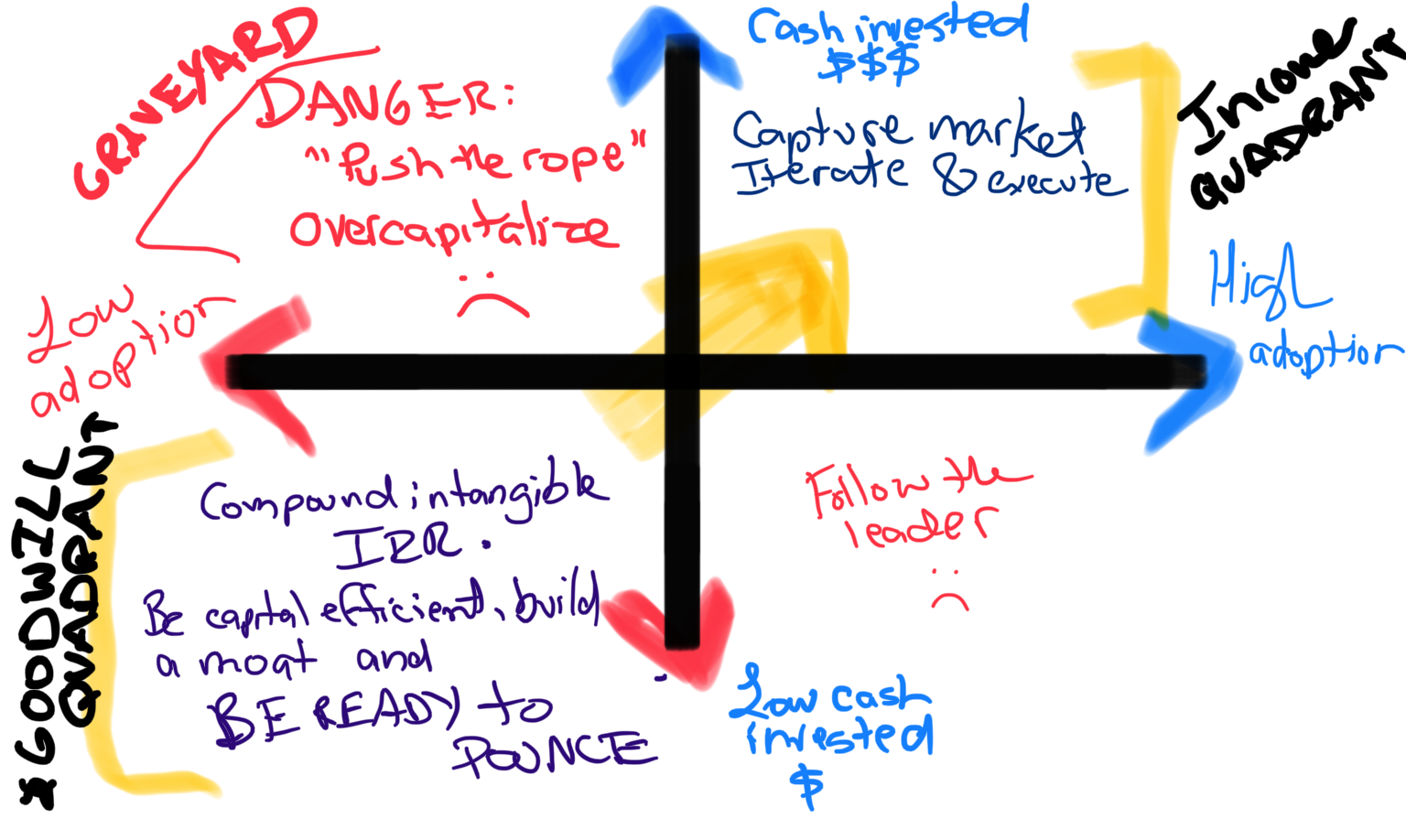

I approach market readiness with a “Goodwill/Income” Mental Framework

Goodwill Stage: returns are primarily intangible, including expanding domain expertise, market know-how, network growth, talent acquisition, discovering the nuance and improving the product’s advantage

Income Stage: Intangible returns continue, but the primary focus of the start-up and market turns to customer adoption and results in revenue and profit KPIs

The latter “Income Stage” growth is what receives most of the focus because the scorecard is more visible. But the compounding returns of the Goodwill Stage are the most powerful part of a businesses’ development. This can occur pre-revenue or in operating pivots as a market evolves. Either way, the scorecard is less trackable.

In our market, the best start-ups remain cash efficient and have excellent IRRs in their Goodwill state. And then the company steadily leans into the post-commercial growth indicators. Time and again I see overcapitalization because a founder or VC wants to believe an opportunity is now. My answer in those cases is for the entrepreneur to stay lean and continue compounding the goodwill side of their growth equation.

New Energy Transition Exit: Generac acquires Enbala

First thing’s first: it is pretty rare for an energy transition M&A event to be on CNBC or Mad Money- but this deal did make primetime TV and the segment can be found here)

Strategic Rationale: Why Generac is now in the software business

Every Wednesday at 10am my house’s Generac generator roars to life for its 2-minute check. The generator is fed by a natural gas line and in the 2.5 years of living here it has been used twice to back-up the house when a storm knocked out the power lines. All the while, sitting in my garage is my Tesla. It has a 100 kWh battery pack mostly sitting idle and plugged in every day.

The cost declines of batteries and the continued progress of distributed energy resources like rooftop solar and at-home batteries mean that the residential back-up power system of the future will look quite different than the past. Instead of supersizing a generator we may just need a better software system to source and route power throughout a house during storms or peak energy hours. And the best software system will then aggregate a neighborhood of household profiles and work with the utility to manage area-wide load.

This narrative is exactly why Generac had to buy Enbala. Based in Waukesha, Wisconsin, Generac sells more than $2 billion of backup power generation products for residential, light commercial and industrial markets. Given how our power systems are decentralizing, Generac has a unique opportunity to capitalize on their distribution network and brand to be a key player in the distributed energy electric hardware and software market. The majority of Generac’s current generators are powered by diesel, gas, or oil. So in addition to building a battery business, the firm has to accelerate its’ software development. The CEO of Generac said this in the deal’s press release: “The deal solidifies Generac’s position as a market leader in Smart Grid 2.0 technologies and opens opportunities for the Company as a grid services provider.”

Enter Enbala, a leader in the Virtual Power Plant vertical

Enbala is a developer of a real-time energy-balancing technology designed to transform energy system operations. The company’s technology captures and aggregates available customer loads, energy storage and renewable energy sources to form a network of continuously controlled energy resources, enabling clients to control, optimize and dispatch distributed energy in real-time.

In simple terms, Enbala’s software helps market participants (utilities, large energy consumers) manage the increasingly distributed load of our power grid. This is called Distributed Energy Resource Management, or ‘DERMS’

Enbala was founded in 2003 and is based in Denver, Colorado. The company’s CEO, Bud Voss, has been at the helm since 2014.

The Financing History

There are a few “fasle-starts” in Enbala’s history that resulted in a recapitalization somewhere along the line. While data shows a 2003 founding, the company’s trajectory meaningfully changed when Bud Voss took the CEO job. With Bud leading the company, Enbala raised about $38M since 2014. The most recent round was an ~$8M Series B-1 with a post-money valuation of $60M. Existing investors included: ABB Technology Ventures, GE Ventures, National Grid, Obvious Ventures and ZOMA Capital.

The Exit

While the exit price-point was not given, it is widely accepted that investors made a nice return on their capital – although that may have been preference driven. Using the last post-$ valuation of $60M as a reference, I am going to assume the purchase price was somewhere between $50-70M. The revenue profile for the company was not detailed but I suspect that Generac paid a very sizable multiple given the strategic and complementary importance of the Enbala asset as detailed earlier.

What are the themes?

1- These businesses take time. A 2003 launch with a 2014 re-launch is a long horizon.

2- Remaining capital efficient is paramount. Most VC investors aim to achieve at least 3x+ cash on cash return. With an upside $100M transaction, this means you would target $30M of invested capital.

3- The buying universe is expanding! Generac is now in the software business. This isn’t your grandpa’s generator company anymore…

Today, Energize Ventures announced our latest investment. The company is Matroid, the category leader in computer vision software. Matroid plans to leverage the new funding to accelerate product development and go-to-market expansion in manufacturing, industrial IOT (IIOT), and video security markets.

The Energize Ventures “Why We Invested” post can be found here. And is also re-posted below for ease.

This investment is an emblematic “Energize investment” with excellent leadership, technology-enabled product advantages, and clear commercial & market awareness. I am thrilled to be working with Reza Zadeh over the coming years.

If you are a reader and in the energy and industrial vertical, you should explore how Matroid can make computer vision accessible and valuable to your organization. We have been showing the power of Matroid to our LPs and energy & industrial network and the adoption is very strong.

Quotes from the Press Release

“Enterprises have tasted the value that software-defined sensors can provide, but are also feeling the pain of rolling out a conventional computer vision team,” said Reza Zadeh, CEO and Founder of Matroid.“Deployments of CV are constrained by Machine Learning engineering time, operator training time, camera interoperability, scaling AI computations, and the difficulty of iterating on neural networks performing important tasks like detailed inspection. With the Matroid product, we set a new standard for ease of use in deploying sensors. With this funding we are excited to take the next steps to bring software-defined sensors to manufacturing and industrial IOT enterprises.”

“Reza and the Matroid team are building a world-class platform that marries the expertise of engineers and operators with next-generation computer vision technologies and machine learning algorithms,”said John Tough, Managing Partner of Energize Ventures. “The Energize team is excited to deploy our financial, operational and industry capital to help Matroid capture market share in energy, industrials and IoT.”

“As the renewable sector continues to grow, we must be on the forefront of new innovations and tools to push us into the future —new digital technologies like Matroid will expedite the energy transition”said Michael Polsky, Founder and CEO of Invenergy. Invenergy is a leading privately held, global developer and operator of sustainable energy solutions, and currently uses video data captured from drones to analyze the state of its wind turbines and other renewable energy sites.

WHY WE INVESTED

Energize Ventures is thrilled to lead the $20M Series B investment in Matroid, a category leader in computer vision software. Existing investors NEA and Intel Capital also participated in the round. Energize Managing Partner John Tough joins Matroid founder and CEO Reza Zadeh along with existing board member Pete Sonsini on the company’s board.

Matroid’s platform makes it simple for enterprises to rapidly deploy computer vision solutions to help automate the process of analyzing imagery data. In a “drag-and-drop” fashion, the software enables domain experts to train machine learning-based detectors that can automatically analyze vast visual data sets, eliminating the need for a data scientist.

Unlocking value in energy and industry

In energy and heavy industry, the physical world is increasingly documented by drones, cameras, satellites and other remote sensing technologies, creating a new bottleneck in analyzing the volume of imagery. Currently, many firms turn to teams of overly-qualified technicians and engineers to manually review troves of images – which is not only inefficient and costly, but also non-scalable and oftentimes inaccurate.

Computer vision is primed to dramatically improve efficiency and safety in these verticals. All energy and industrial companies perform inspections of their infrastructure, plants and equipment on a regular basis to conduct preventative maintenance and pre-empt failure. For example, wind farm operators typically inspect each wind turbine once every three years to identify cracks, lightning strikes, corrosion and other defects that might cause failure. Worker safety and compliance are also core principles for firms operating in dangerous environments. Computer vision can help ensure workers are wearing protective safety gear or identify dangerous gas or chemical spills invisible to the human eye.

Matroid: Making computer vision simple and accessible to everyone

CEO Reza Zadeh launched Matroid in 2016, applying decades of research on computer vision and machine learning approaches to deliver a simple and intuitive solution for enterprises. Reza and the Matroid team recognized early on that typically only internal experts at a company possess the knowledge required to create, tag and deploy well-functioning computer vision solutions. However, most firms lack the experience and/or resources in data science and machine learning to integrate computer vision into their operations in a scalable, repeatable manner. To make better use of their imagery data, they needed a better computer vision tool. Enter Matroid.

An award-winning team obsessed with customer needs

Today, Matroid serves customers across manufacturing, energy, government, retail and security by helping reduce operating costs and increasing efficiency, safety and regulatory compliance. Its growing team of nearly 20 software engineers and data scientists draws from leading machine learning institutions such as Stanford, Carnegie Melon and MIT. In 2019, the company was named a “Cool Vendor” in AI Core Technologies by Gartner. Matroid currently partners with corporates such as Dell, HP Inc. and Eagle Eye Security offer a fully integrated solution across vision hardware, compute, networking and Matroid’s software.

Energize believes computer vision will play a central role in harnessing the expertise of engineers and operators to digitize inspection, compliance and safety, quality assurance, construction and more. With the Series B investment, Matroid will continue developing its enterprise computer vision product features, expand sales, marketing and customer success, and double down on industry-leading research in applied machine learning. We are excited to help Reza and the broader Matroid team build the future of computer vision!

New Energy Transition Exit: Array Technologies IPO

Here is an incredible story about resilience and perseverance in the renewables space:

A 30 year old hardware company previously overlooked and dismissed as selling a niche solar product is now growing >100% year over year with re-accelerating topline growth. The company went from $500M last year through the $1BN revenue mark in 2020… all while being profitable.

And yet, that is exactly the narrative with Array Technologies.

This is a new type of energy transition exit for us to review! Instead of being a start-up, Array Technologies is a mature, private market company playing a big role in the energy transition.

The Company

Array Technology was founded in 1989 and is based in New Mexico. A month ago they filed

Array is a solar tracker company. These are the technology and mechanical systems that help move a solar array in-line with the sun’s arc in the sky. These systems can be quite mechanical and a number of firms are trying to reduce the number of motors (moving parts) required per MW of power capacity. Array claims to have the industry leading efficiency, and uses 1 motor per MW of generation. Less moving parts means less likelihood for mechanical failure! And given that solar sites are expected to operate for 20+ years, the need to have the hardware match the expected duration is key.

The #1 solar tracker is Nextracker, and Nextracker is a subsidiary of the public company Flex. That means that Array Technologies will be the first and largest solar tracking company available for the public markets. Array has over 17GW of utility scale solar using their products.

The utility scale solar market is absolutely booming so investing in Array Technologies is a way to gain exposure to that market opportunity.

Array Technologies Financials

Array Technologies is profitable

The company has $975M of revenue over the past 12 months and as a hardware player is growing a whopping 100%. And on this revenue they have OK gross margins at ~25%. These margins are solid for hardware players in the renewable markets, where margins are usually razor thin. Most impressively, the firms has 13% net income margins.. with this growth! The net income levels show how there is good operating leverage in the business. This operating leverage is driven by the technology differentiation of the product leading to very large purchase orders, on relatively low sales & marketing.

Overall, though, the growth and margin profile combination is quite excellent.

The Deal

Array Technologies is looking to issue $675M of shares in the IPO. The company is tentatively being valued at $2.5 billion. The original IPO goal was a $100M issuance, so the fact that the issuance is now upsized to nearly $700M shows how strong market interest is right now in this theme.

At $2.5 billion in value, the company will trade at ~2.5x revenue and 21x net income. This valuation has increased 3-4x over the past few months as the company’s growth profile and industry tailwinds make it a special asset.

The company is currently majority owned by OakTree. OakTree purchased the company via a LBO through the OakTree Power Opportunities Group.

Similar Companies

Another up and coming name in this space is Sunfolding. Sunfolding uses a compressed air system to optimize solar tracking and maximize energy output. Their unique pneumatic approach should help Sunfolding keep O&M costs low for the energy developers.

In Summary

In summary, Array Technologies is coming to market at a great time. The company is growing ~100% year over year and has a nice income profile. In addition to the current financials, the company will have great tailwinds from the utility scale solar market. I expect the company will find a welcome shareholder base in the public markets.

The energy transition M&A tracker, I codeveloped with Kevin Stevens is now updated with this transaction. Link found here.

A well-known banker in the space reached out after seeing a few of the Energy Transition M&A posts. We talked about the current market trends as well as likely / active engagements. Here are a few key notes from that call:

1-Potential Acquiror Market has broadened: In a recent M&A process there were >25 management presentations. This was because potential buyers for the asset came from many different backgrounds:

Energy management firms

Industrial technology giants

Progressive utilities

Generalist software companies

The normal firms participating in M&A over the past few years have been the energy management firms and industrial technology giants. But, the more progressive utilities showing up looking for ways to expand their own businesses is a NEW addition. And for avoidance of doubt, the presence of traditional software firms playing in the energy transition space is VERY RARE. Over the past decade only a few software firms have acquired an energy transition company- with the headline acquisition being when Oracle acquired OPower.

2- Everyone now understands SaaS: the banker claimed that in years past he would have to give a presentation to the “older school acquirors” about why SaaS gets valued at a premium and to share about the multiples. While education needs to occur to share the new heights of SaaS multiples, the industry execs now appreciate the delta between perpetual sales and SaaS sales.

3- Industrials Pay Premium for Standalone Scale: The largest industrial technology firms have big balance sheets. And despite a lot of public clamoring about wanting to be acquisitive to better enter the software market, these industrial giants tend to only pay the true SaaS multiples when a business reaches scale. Why? A big concern these giants have is that their corporate culture may hinder continued growth of the target. So the M&A heads want these businesses to stand-alone and be a pillar for future M&A opportunities themselves. This usually means a revenue base of at least $50M for an industrial technology firm to get active in the software market. And even when these industrials get comfortable with M&A rarely is a multiple > 10x revenue.

I imagine we will continue to see more “non-traditional” firms be active in the energy transition M&A market.

As a front-row observer to the energy transition, I have the fortunate position to see which firms are making positive strides to enable and ride the movement. While I mostly focus on the early stage environment, I also get to see which incumbent firms are creating pivotal positions in the transition. Microsoft is one of those well-positioned incumbents becoming the technology backbone to the energy transition and industrial technology movement. The how and why was written on my recent Forbes post.

Microsoft is the operating system for the desk worker at most energy and industrial firms. Mac computers are rare and ruggedized PCs bridge the office and the field.

Based on a flurry of recent press, it is evident that Microsoft is interested in expanding their default status in the white-collar cubicle to dominance out in the operating environment. Microsoft’s approach to taking over the energy vertical is much like the technique of the earliest oil renegades: the wildcatter.

Why is Microsoft refocusing here NOW?

A decade ago the cost to digitize and connect remote operations was prohibitively expensive. A decline in sensor costs, networking costs and edge compute costs now allows edge production environments to be big generators of data and consumers of compute. Just as wildcatters speculatively prospect for hidden or previously unloved assets, Microsoft is revisiting the O&G space to see if they can expand technology sales to the new field opportunities. And of course, Microsoft is not alone in this land-grab mode. Like the wild west, the physical operating environment provides sizable greenfield environments and all of the cloud and compute giants like Microsoft, Google, and Amazon are aiming for the new revenues. While the battle will be fierce, Microsoft is making a big land-grab right now.

The Wildcatter: Microsoft + Energy & Industrials

Microsoft represents a story of resilience that the energy and industrial vertical wants to embrace and believe. At one point, Microsoft was written-off as Google and Amazon charged ahead into the enterprise. And yet, under Satya Nadella’s leadership, Microsoft has roared back in the enterprise segment and is solidifying and expanding its’ technology footprint in these asset heavy verticals. Analog firms love this Microsoft story and appreciate the strength of the logo.

Microsoft is employing a consistent technique to expand is these areas:

Step 1: Microsoft acquires a PPA or makes a purchase commitment to get a conversation going with the energy company

Step 2: Microsoft closes the much more lucrative cloud and software contract by promising to infuse “digital” into the more analog firm

Here are the examples:

Microsoft + Shell: Microsoft agreed to purchase power from a Shell-developed renewable energy site. But most importantly both companies agreed to a technology JV, where Shell will utilize Microsoft compute services to develop artificial intelligence technology that helps Shell access real-time data insights and improve the efficiency of their operations, leading to lower emissions. Microsoft also committed to offer new digital tools for Shell to deliver to Shell’s own customers.

Signal: Shell is doubling down on Azure and Shell’s customers are also encouraged to use Microsoft Azure.

Microsoft + BP: Microsoft agreed to purchase power from a bp-developed renewable energy site. (Can you see the trend!) Alongside this PPA, bp and Microsoft agreed to “co-innovate” between Microsoft’s digital expertise and bp’s knowledge of the energy markets. These areas include smart cities and smart consumers.

Signal: BP is doubling down on Microsoft Azure

Microsoft + ENGIE: Microsoft purchased 230MW of utility scale wind from ENGIE. And ENGIE responded by committing to running their entire 15,000 MW energy portfolio on Microsoft’s Azure cloud services. That is a massive win for Microsoft’s cloud product.

WILDCATTERS

Signal: ENGIE worldwide is doubling down on Microsoft Azure

Microsoft + Rockwell: Rockwell is taking steps to build better software solutions for their energy and industrial customers. The firm intends to deliver these products by expanding a partnership with Microsoft, the dominant existing technology partner in the industrial vertical. Case in point: just this week the two firms announced a 5 year co-development effort to deliver all new Rockwell industrial technology applications to customers through Microsoft Azure.

Signal:Rockwell is doubling down on Azure and Rockwell’s customers are also encouraged to use Microsoft Azure.

Conclusion

In the coming quarters I expect we will see many more partnerships between Microsoft and the stalwarts of the energy and industrial verticals. I believe that Microsoft will have an outsized influence on the energy transition and industrial technology movement. Microsoft is leveraging their IT strength into a stronghold on the OT environment and locking in customers that will depend on the Azure cloud for decades. Much like a successful wildcatter, these accounts will be paying dividends to Microsoft well into the future.

Tip #7 for Product-Driven Growth: Customer Conferences

Last week I wrote a post about the top 7 ways that start-ups can deliver product-driven growth. That post can be found here. I left out the 7th tip because I felt it deserved more coverage: conferences.

Conferences allow start-ups to create a broader presence. And I am not talking about a closed-door, customer-only conference. The best company-sponsored conferences find a way to associate the company with the broader industry opportunity, not just one particular outcome. Or as Bilal Zuberi and Glenn Solomon taught me “find a way to own the problem, not just one solution.” When a company transcends to represent an industry’s opportunity, its’ centrality drives greater awareness and commercial success. Glenn has a great interview with Nick Mehta, the CEO of Gainsight, where they cover the topic of Building Community in a New Category.

Here are a few nationwide examples:

RSA Conference: (Link here) has a motto “Where the World Talks Security” and is now synonymous with as the cybersecurity conference.

Dreamforce by Salesforce: (Link here) is synonymous with sales and growing a business.

Pulse by Gainsight: (Link Here) is synonymous with customer success.

Pi World by OSIsoft: (Link here) for connecting and optimizing production assets.

And here are three Energize Ventures portfolio companies that are also beginning to employ conferences with great brand and customer results:

Empower by Aurora Solar: (Link here) is now the de facto gathering for the solar industry. Their phrase is: “where solar company leaders, industry professionals, policy insiders, and growth experts come together to share their knowledge, expertise, and insights”

DDC by DroneDeploy: (Link here) is now the largest conference focused on drones and aerial analytics. “DDC brings together a community of innovators from our ecosystem of industries, including agriculture, construction, energy/oil & gas, mining, and more to discuss the latest drone innovations, best practices, and hot topics impacting operations.

Note: this is October 13th and 14th. Register now!

TimeMachine AI by SparkCognition: (Link here) is now the premier AI conferences in the United States. Last year, over 1000+ people came to learn about the transformative nature of artificial intelligence in key industries around the globe, and walked away with actionable insights to accelerate their businesses.

Who else is doing this well in the energy and industrial verticals? And who is adapting well to the digital-first conference environment of 2020?

Last week, an Energize Ventures portfolio company, Awake Security announced it was acquired by Arista. Arista is a networking company with a $15 billion market cap based in Santa Clara. Awake Security’s CEO, Rahul Kashyap, is a visionary cybersecurity executive and a great leader.

Energize Ventures participated in Awake’s most recent capital raise. That round was a Series C and closed in Q1 2020. At Energize we are big believers that traditional industries need better security tools. New production assets are increasingly distributed and networks span from central HQ all the way out to the wind farm. Similarly, we believe that no energy and industrial firm will be exclusively “cloud”. A hybrid solution of cloud and on-prem technologies will always be used in these verticals. These complex network architectures require new digital solutions- and Awake was perfectly positioned to serve these new security needs.

We invested with the goal to infuse Awake’s cybersecurity platform into utilities, manufacturers, and the broader set of industrial companies. Our conviction proved correct and almost immediately a top 10 US utility adopted the product. Sales cycles that can take years moved to weeks. The reason? When a critical infrastructure firm has a cybersecurity concern, a year-long sales cycle moves to days… and mountains are moved by the customer to find budget.

The product-market fit uncovered by Awake ultimately means that Energize’s investment relationship with Awake was fruitful but short-lived. I wish Rahul and the Awake Security team a successful next chapter within Arista. The combined company is certain to find a lot of customers in the energy and industrial verticals.

Yesterday I wrote about the 3 different ways to expand growth in an energy and industrial account. I highlighted that “Product-led growth tends to be the most stepwise in commercial advancements.” Today I wanted to highlight the techniques that I have seen work well in accelerating a software company’s march through the rest of the organization.

Tip # 1: Keep the Sales Exec on the account post-sale for as long as the original sales cycle. Yes you can bring in Customer Success but maintain strong sales presence. A huge mistake I see is when firms immediately hand-off the sales executive. My rule of thumb is that the sales executive should stay involved post-close for as long as the sales cycle itself. So, in a 9-month sales cycle, the sales exec should stick around for another 9 months.

Tip #2: Set up a “Digital Innovation Meeting” 5 months post-sale with the Customer. Ask the customer to include the budget owner and the lead user. From the start-up side, include the sales exec, customer success rep, and a customer-friendly product manager. This is where your Sales Exec’s “nose for revenue” becomes valuable as the sales exec should identify 1-2 other execs in the customer organization to invite. This is why it is important for the sales executive to stay around: their nose will hear recurring names and themes / problems that could be a next product opportunity.

Tip #3: Establish a Customer Council. Most customers in this space are very keen to make sure that they are keeping up with the peerset. Therefore, an early stage firm providing customer validation is incredibly important. Similarly, no single critical infrastructure firm wants to be the only customer you have in the segment. A customer council gets a similar cohort of customers together to share positive engagement examples and aggregate future product recommendations for the start-up. This gathering can be very powerful to drive both new revenues and demonstrate long-term commitment to the relationship. In summary, energy & industrial customers all want to move forward in new technology endeavors together. By setting up a customer council, a startup easily expands the narrative from a product to a broader technology and software partner.

Tip #4: Have Well-defined and Clear Pricing. Expanding your product internally best happens when there is clarity on the boundaries where the current product’s value and associated pricing ends. Being clear on the purpose, features and intra-company user makes expansion easier later in the engagement.

Tip #5: Write up a Master Services Agreement. Most start-ups will rush to close the contract. More mature entrepreneurs will simultaneously explore a MSA. A MSA is contract reached between the start-up and the customer, in which both parties agree to most of the terms that will govern future transactions or future agreements. This usually brings in more senior sponsorship, and accelerates follow-on sales since there are defined parameters around everything from data treatment, press releases, onsite visits, and vendor validation. And a hidden bonus is that if suddenly a budget becomes available near the end of the year, the start-up can be easily contracted for the software opportunity.

Tip #6: Collaborate with the Customer’s Consulting/Innovation Advisor. Almost every Fortune 1,000 energy and industrial customer has a consultant: Accenture, IBM, Deloitte, etc. These consultants have multi-year relationships and usually have proposed a dozen ways to streamline or digitize the corporate’s operations. These consultants also want to see the concepts materialize and identifying what digital solutions are aligned with a start-ups core competencies can lead to a nice expansion. And be sure to identify ways to compensate the consultant with an integration deal or services recognition thereafter.