During my final stint at KPCB back in 2012 I was researching the OT cybersecurity space. I met with approx. 10 companies and the clear leader back then was Waterfall Security. I loved the concept: bring world class cybersecurity techniques to critical infrastructure. The only issue was that our critical infrastructure firms were still in education mode and there was no budget for OT cybersecurity. Case in point is that the total revenue size for those top 10 companies was less than $15M.

I watched the space closely over the next 6 years and when I joined Energize I had a good sense that the OT and IoT cybersecurity market and customer interest was finally sizable. After a 2016 and 2017 market map with Juan Muldoon we really connected with Edgard, Andrea and Moreno at Nozomi. They saw the future convergence between OT and IT and we led the $15M Series B in Q4 2017. It was my first investment with Energize and my first board seat. Juan Muldoon is an observer and we ran a great diligence process where we uncovered some truly differentiated insights that we still talk about today.

I visited the broader Nozomi team in Mendrisio Switzerland shortly thereafter and have been every year since and can’t wait to get back this year.

Today, Nozomi announced a $100M Series D. Nozomi’s contracts with a single customer now approach the entire market size a decade ago. Our new critical infrastructure, with energy leading the way, is increasingly decentralized and digitally connected. Nozomi Networks now helps firms of all types: energy, healthcare, smart cities, automotive, etc. protect their assets through new, innovative AI-enabled techniques.

After Energize led the Series B, we have invested at least our pro-rata in each subsequent financing. The market size for Nozomi is growing, the team is world-class, and the product is second to none. The company intends to go public in the future, and I am excited for that future opportunity.

The Biden administration has been vocal in it’s intent to advance an infrastructure bill that will help improve America’s critical infrastructure. The size and scope of the bill has varied dramatically over the past 6 months.

Earlier this week, a bill with bipartisan support finally emerged. The chart below shows the sector-specific capital allocations within the bill, and how the amounts have changed since the first proposal.

One area of critique in the energy community is the decline in scale of electric vehicle (& related) support. Most EV drivers receive a tax rebate with the purchase of an electric vehicle and the scale of that program going forward is going to get smaller.

I think that the lower tax incentive is just fine. Tax incentives are meant to help early adopters: in the 2010s, the cost to develop and deliver a new EV was quite high. By having a $7,500 per vehicle tax rebate for the purchaser, auto OEMs were more willing to commit to EV development knowing that a consumer would pay an effectively lower rate. But now, just read the news: EVs are going mainstream and as the technology goes mainstream, the tax support should subside.

Other areas, like our grid infrastructure, should receive the capital to help asset owners and capital providers increase the rate of return on traditionally low-return investments. EV charging straddles this logic: infrastructure but in the earlier stage of development and deployment. In my opinion, fiscal support should last another 3-5 years there until we have more consistent charging networks. But in general, I suspect the corporate community (destinations, OEMs) will take the reigns on driving EV charging network growth.

Overall, good to see our elected officials get a moderate infrastructure bill across the line.

M&A Tracker: Power Factors, a Sign of the Renewable Times

The costs to develop utility scale solar and wind have dropped by ~10% per year for over a decade. The decline in costs has resulted in the installation of tens of gigawatts of solar and wind and an even larger upcoming pipeline. To-date the majority of economics in the space have gone to developers and those associated with putting new assets in the ground.

Now that the scale of in-ground, operating renewable assets is so meaningful, I expect the emergence of sizable software and technology businesses built around the maintenance and optimization of these newer power units.

One of those scaling software businesses serving the space is Power Factors. Power Factors is a mature (primarily) software company serving the renewables market. The company’s core product, the Power Factors Drive Pro, is a cloud-based asset performance management (APM) solution that integrates all the key data owners, operators and asset managers need to monitor, manage and optimize the performance of renewable energy assets throughout the asset lifecycle.

As seen in the article below, Power Factors was acquired by Vista Equity Partners. Vista is a well-known technology growth equity/PE firm and this acquisition is a signal to the recent maturity of the renewables O&M market. Wind farms and solar farms have 10-20 year operations contracts with their offtakers. Developers and utilities will look for long-term software contracts to help monitor and optimize asset operations over a similar time period. Firms like Power Factors are well-positioned to lock in these long-term deals and capture the many upcoming GWs in the process of being integrated into the grid. I expect Vista will implement a bolt-on M&A strategy to bring more technology solutions to the Power Factors platform and am bullish on the company going forward.

On the surface, ESG-related investing should be immune to attack. The promise of delivering financial and ESG-positive returns are the holy grail to an institutional investor. And yet, the ESG space isn’t exactly squeaky clean. The public market equities screening for “ESG-positive” firms is particularly terrible. Why?

The ability to track and quantify a corporations environmental, societal and governance policies and impacts is actually quite nebulous. Case in point, as see in this Stanford study “The World May be Better Off Without ESG Investing”. This part of the article really capture the problem that originate with fundamentally weak ESG ratings agencies:

“At the core of the problem is how ESG ratings, offered by ratings firms such as MSCI and Sustainalytics, are computed. Contrary to what many investors think, most ratings don’t have anything to do with actual corporate responsibility as it relates to ESG factors. Instead, what they measure is the degree to which a company’s economic value is at risk due to ESG factors. For example, a company could be a significant source of emissions but still get a decent ESG score, if the ratings firm sees the pollutive behavior as being managed well or as non-threatening to the company’s financial value. This could explain why Exxon and BP, which pose existential threats to the planet, get an average (“BBB”) aggregate score from MSCI, one of the leading rating companies. It could also be why Phillip Morris made it onto the DJSI. The company recently committed itself to a “smoke-free” future, which ratings agencies might perceive as reducing regulatory risk even though its next generation of products remain addictive and harmful.

The second problem involves how ratings firms assign weights to each ESG factor. To compute a company’s ESG score, ratings firms score every company on a variety of ESG factors and assign weights to each of these factors, aggregating the results into a composite ESG score. A strong ESG performer might get a triple-A composite score, while an ESG laggard might be assigned a triple-C score. These scores form the basis for how ESG indexes and ESG funds construct their portfolios. This may seem like a legitimate approach, but it’s not. It is subject to human judgment and inconsistent access to ESG information, making for tremendous variability across raters. But more detrimentally, it permits companies to achieve high composite scores even if they cause significant harm to one or more stakeholders but do well on all other parameters.

Take the case of Pepsi and Coca Cola. Both companies get high ESG scores from the biggest ratings firms. They are also typically amongst the largest holdings for ESG funds, largely because they rank high on parameters such as corporate governance and greenhouse gas emissions. However, their core businesses involve the manufacturing and marketing of addictive products that are a major cause of diabetes, obesity, and early mortality. Pepsi and Coke leverage their power to prevent taxes and regulation on their businesses and fund large amounts of research to divert attention away from the health impact of their products. With the cost of diabetes now over $300 billion annually in the United States alone, the human and economic harm caused by these companies may outweigh their economic contribution.”

This ESG tracking problem is admittedly easier to solve at the earlier stage of a company’s life. Policies and impact are easier to measure and a company’s mission can be more directly tied to the product being sold. The “E” in ESG is also more measurable than the S and G. I suspect that better, data-driven products are coming to market to reveal some of these ratings inaccuracies or the whole theme is going to devolve into useless marketing jargon.

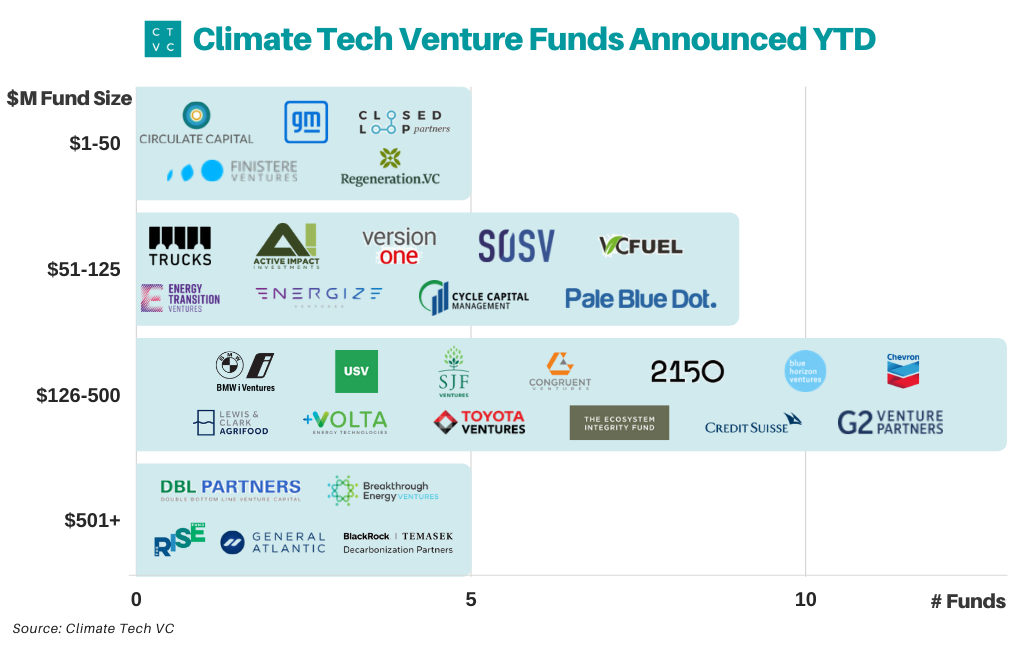

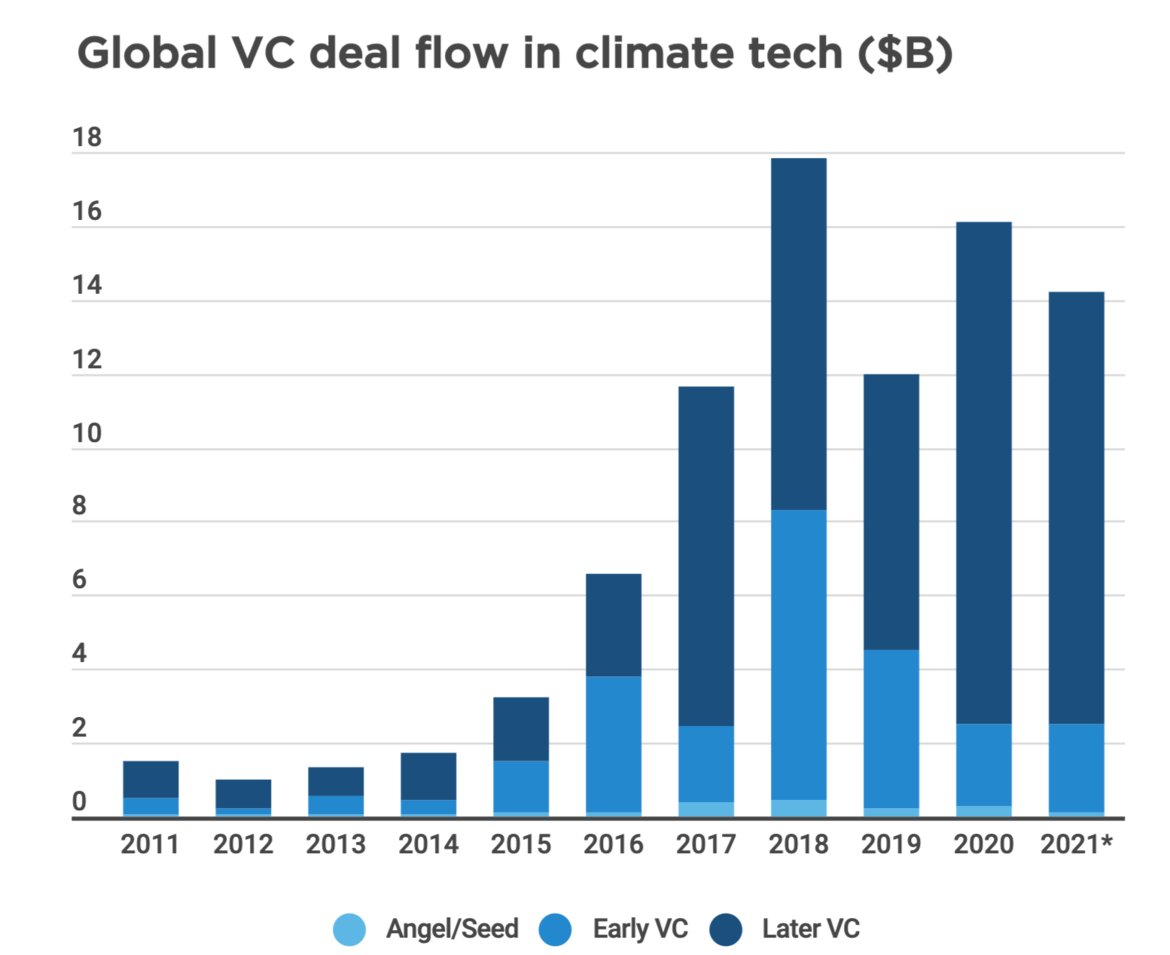

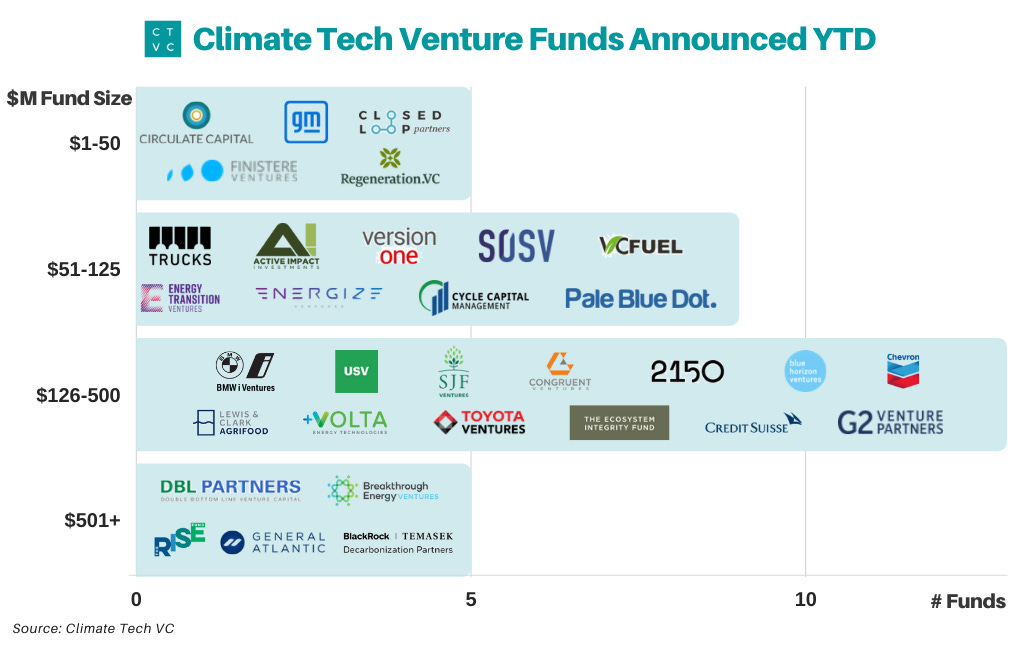

I don’t fully associate Energize’s focus as “climate tech” but there is certainly overlap in our interests and the theme. Two charts came across my thread this morning that show just how much interest there now is in climate tech/sustainability…

First, is a chart from Sonam Velani that shows that deal flow into climate tech is already at 88% of the 2020 totals and on pace to nearly 2x 2020 figures.

The second is a graphic from Climate Tech VC, a weekly publisher on the theme, that shows the number of funds announced year-to-date. Within this list they also capture Energize’s specific $125M CDPQ co-investment fund. I am expecting many more firms (and funds from existing firms!) to be added to this list by year end.

The supporting data shows that more climate-related funds are being launched in 2021 than the previous 5 years combined. Who is coming to market? We have traditional PE and asset managers like BlackRock, General Atlantic coming to market. We also have traditional VC firms entering climate, like USV and we have a number of corporates (GM, Chevron, BMW, Toyota) launching specific efforts.

I am the most pleased to see the experienced names in the space like G2 Venture Partners, DBL, and Congruent are also raising new capital to accelerate the sustainable transition. There are a lot of nuances to investing in the energy and broader sustainable transition and the newest entrants would benefit from studying these established firms.

2020 forced decentralization upon the workforce. At Energize we handled that by revamping our process and focusing on over-communication. This year is a little different. Since ~March we have been back in the office 3-4 days per week. The balance of home/office work feels good.

One of the benefits that is hard to overcome in a fully remote structure is the spontaneity of education and training. In my experience, learning together in an office with a whiteboard remains the best way of transferring intra-team knowledge. Education and training brings a team together and forces team members to make the implicit explicit.

For example, a few weeks back I ran a session on sales efficiency and the nuances to quota ramping and sales cycles. The topic originated when we were discussing a portfolio company’s revenue strategy and I realized some of the team wasn’t as comfortable with the investment (team, capital) required by the company to hit their goals. These session (and others to come) also help elevate the different backgrounds and strengths of our investor group.

There are a lot of reasons to work remote. There are a lot of reasons to have an office. I believe the best way to train and grow a team of investors is in-person. We have hired a number of new professionals here at Energize over the past 12 months and have a few more on the way. To the new employees under consideration for our open roles: we can’t wait to learn alongside you and from your new, additive experiences.

Oh, and Chicago is a great home base. 😎

Fast Radius merger with ECP Environmental Growth Opportunities Corp. at a post-transaction Equity Value of $1.4 billion

Exciting update from the Energize portfolio today. Please see our blog post here, and copied below. (also coverage in the WSJ and the company’s own blog post). Kudos to Lou, Pat, and the entire Fast Radius team for their continued progress.

—

Fast Radius, the leading provider of cloud manufacturing solutions and an Energize portfolio company, today announced that is has entered into a definitive business combination agreement with ECP Environmental Growth Opportunities Corp. (NASDAQ: ENNV), a publicly traded special purpose acquisition company (SPAC). The combined company will have an estimated post-transaction equity value of $1.4 billion.

The net proceeds raised from the transaction will be used to support Fast Radius’ continued growth across customer acquisition, software development, and micro-factory expansion. Founders Lou Rassey, Pat McCusker, Bill King and John Nanry will continue to lead the company and remain committed to executing Fast Radius’ proven business model and driving value for all stakeholders.

The intersection of new technology and traditional manufacturing

The manufacturing industry is reaching an inflection point and is primed for digital innovation. In the past, the sector has been dominated by analog and often outdated operational processes, often lagging behind other industries in terms of technology adoption. And while there are many digital tools available to help simplify manufacturing operations and enhance customer experience, the problem is that many of these technologies do not integrate well with the existing infrastructure. We have seen a need among industrial manufacturers for solutions that can help address complex challenges that come with managing global supply chains. At the same time, the industry needs innovation that can help further drive down costs and optimize efficiency – both of which benefit the end consumer.

Fast Radius’ integrated digital and physical platform simplifies the way parts are designed, made and moved around the world. We believe their Cloud Manufacturing Platform technology is poised to have a profound impact on the future of the industry.

Our relationship with Fast Radius

We first met the Fast Radius team in 2019, initially invested in their Series B in early 2020, and then followed up with another investment – including capital deployed from our growth fund – in Q1 2021. Both Energize and Fast Radius being based in Chicago, we had the opportunity to walk over to their headquarters to tour their factory, get to know the team and learn more about their product. We left that initial meeting with a strong feeling that the technology we just saw would be the future of manufacturing.

Lou Rassey presenting at Energize Demo Day in Chicago in 2019

At Energize, we are big believers in the decentralization of industrial processes to increase operational efficiency, lower costs and improve sustainability. Fast Radius’ Cloud Manufacturing Platform enables seamless and on-demand production of parts, helping customers address supply chain challenges and efficiently scale their business, all while operating more sustainably.

While Fast Radius has a strong track record with customers in industries like healthcare and robotics, we are also seeing new opportunities arise to unlock value in energy and sustainable industry – such as the design and manufacturing of parts for solar installation and electric vehicles. In our partnership with the team, we have focused on helping them accelerate expansion of their software platform, identify and launch new applications, and scale their production-grade cloud manufacturing capacity.

An exciting milestone for a deserving team

An extremely important piece in Energize’s due diligence process and evaluation of a potential investment is the team. A technology can be world-class and poised to disrupt an industry, but without the guidance and leadership of the right team, it is not a good investment. Fast Radius’ team, led by Lou, Pat, Bill and John has expertise that runs deep and wide across manufacturing, engineering, industrial innovation and technology. More importantly, they are relentlessly committed to their customers. Fast Radius is not a design or fulfillment shop, but a long-term partner in helping make customers’ visions a reality.

We are thrilled to support Fast Radius in this next step and are excited for what’s to come as they continue to transform the manufacturing industry throughs software innovation.

I would venture that ~80% of the people I engage with over email on a weekly basis are also readers here.

So, if I am slightly slower in responding the next 2 weeks, it is because I am out on vacation with my family. Need time to recharge… and am aiming to cap work at 1-2 hours per day. Yesterday had the hours creep back up… but there are exciting developments underway here at Energize. And sometimes (increasingly all of the time) the work feels like the “fun”.

We kicked off our midyear review process here at Energize last week and I held my 1:1s with my team this week.

Every year we have a robust planning and strategy session for the firm’s top 5 goals. Then every individual (investor, platform) identifies how they will contribute towards those efforts through individual and team-oriented metrics. As a team we have truly embraced the structure and it is one of my happier implementations here at Energize.

Investing can become a single player game. Almost all of our development efforts are around enforcing a team approach where we feel success in the firm’s collaborative advancement. I kick off every review with a 2-3 page summary of my sentiment towards the firm’s current status. VC funds tend to define success in longer (5-10 year) increments that match the development of the portfolio. Investment firms can have an even longer horizon as talent and multiple portfolios develop. Balancing the short term quarterly progress with the long-term horizon can be hard. In my midyear review I talked about that trade-off and wanted to share it here:

In many ways I judge our near-term success by constantly asking myself these three questions

Are we making long-term investments, and avoiding short-term thinking?

Are the correct teammates in positions where their strengths can be maximized?

Are we responding to our stakeholders (entrepreneurs, LPs, co-investors) and iterating to stay sharp on near-term execution?

These questions stirred some good internal conversations. I will post some of the takeaways over the coming weeks.

I worked at UBS right after undergrad. It was the mid-to-late 2000s and there was an abundance of press (and hysteria) around two key items: Private Equity, and Oil & Gas prices.

Blackstone, as the face of mega-PE, went public to a heap of fanfare in 2007. Oil and gas peaked in June 2008 at $170/ barrel. Both topics covered CNBC for months. Due almost entirely to the financial collapse, the subsequent 3-4 years were quite dismal for both themes.

PE began bouncing back in the early 2010s and oil-related commodity prices have stayed depressed over the past decade. While there has been some recent resurgence on oil prices, the O&G private equity firms that dominated the markets in the 2000s are far less influential than their earlier vintages. Some of those oil & gas firms are pivoting to renewables.

One of the most traditional O&G names that is attempting a renewables pivot is EnCap. Long a carbon-based investor (and still has exposure there) the firm is beginning to invest a fair amount into renewable efforts. One of those examples is Jupiter Power, a battery developer, where a number of great contacts I met through Energize’s LP base are now working.

Another pillar of the the traditional infrastructure PE world is EQT. They used to invest in more carbon-based firms, but now are moving to next-generation infrastructure, including renewables. They had previously founded O2 Power, a utility-scale renewables-focused developer JV with with Temasek.

EQT announced another interesting deal today, with the acquisition of renewable energy developer Cypress Creek Renewables. Cypress has developed over 11 GW of power and currently operates nearly 2 GW of assets. My suspicion is that EQT is not investing here just for the asset in its’ current form, or even the current trajectory. I suspect that EQT is also going to be adding a lot of capital to EQT’s balance sheet to help Cypress grow to meet the major demand for community solar and utility scale projects in the US. Net while this is a full buyout, I expect there to be a “growth equity” looking incremental capitalization to the company.

This may seem like a more standard deal, but this buyout + growth capitalization deal is specifically new to the energy transition. Most of these transactions to-date have been exclusively project finance or growth equity. The shift for EQT to control ownership shows a desire to be a larger player in the space, and also shows greater conviction on renewables as an asset class. Given EQT’s brand presence, I predict that more large PE players will be entering the renewables arena.