In business school the phrase was a reference to Eugene Fama’s “Efficient Market Theory”. But in today’s market it feels like this statement is now the valuation expert’s way of throwing their hand in the area and saying “who knows!?!”

I am not going to comment on Gamestop. Instead I am going to focus on how there is no real private market for late stage growth equity serving deeptech and cleantech businesses.

Cleantech and deeptech are generally long-horizon investments with sizable step-wise technical and commercial gains. In many ways these investments resemble pharmaceutical-related investments cycles and payouts. A number of high profile and developmentally expensive drugs don’t move to the next stage… but when a mass-market drug is FDA approved, the windfall covers the costs of the lost trials elsewhere.

There are many high-growth sustainability, electrification and broader deeptech-themed investments hitting the market at high profile valuations. As a private market investor, the valuation jumps these companies earn from the private-to-public move can be surprising.

A lot of people are pointing to public market froth as the logical explanation. The reality of SPAC transactions is that they are a big source of cash … and dilution for the target companies. But these same hi-growth private companies have been mostly starved of capital in the private markets. As a result, executives in the deeptech field are now trained to view financing risk as the primary barrier to investing in IP and subsequently hitting the big payout events.

Meanwhile, the SaaS vertical has every valuation metric meticulously analyzed around pricing. It’s the closest to a liquid market I’ve seen in the private markets: there are indices and the multiples are tracked religiously. There are still bumps when these SaaS companies go public, but the range is knowable. The reason this path to public is more streamlined for traditional SaaS companies is because there is a very healthy and robust late-stage growth equity market acting as a pre-public pool of capital.

The SPAC is effectively becoming the late-stage growth equity vehicle for the deeptech markets. As a result in some cases the future year valuations are being pulled (slightly) forward. And while it is easy to point to froth, I take the opposite view. These are clearly important and valuable companies with aligned economy, humanity and shareholder upside. I am glad that public market investors will be able to participate in the asset appreciation.

But, it’s a shame that our private growth equity markets weren’t able to help these companies grow a bit longer outside of the public eye. And so while it is helpful to have the SPACs in market, I actually believe the story here is the incredible opportunity for growth equity capital that serves the deeptech and cleantech environment.

Knowing the Energize team’s entrepreneurial approach, I expect we are going to do something about this…

Sitetracker’s $42M Series C: Energizing the Future

The best part of my job is getting to meet with entrepreneurs who share with me their vision of the future. At Energize we meet around 500 qualified companies every year. We look for a CEOs storytelling ability and his or her conviction around what will be different and new in the coming years.

Through our own experience, our LPs and our continued learnings, we also develop ‘prepared mind’ theses to our areas of focus. One of those areas is the future state of our critical infrastructure. At Energize we thoroughly believe that our centralized critical infrastructure is dispersing to the edge. Big power plants are being decentralized into wind and solar farms. Rooftop solar and electric vehicle charging infrastructure are infiltrating houses, apartment buildings and commercial buildings. Cell towers are going from huge structures to rooftop cell relay sites. Critical infrastructure is atomizing and distributing. And the new energy economy is at the heart of this change.

When we first met Giuseppe Incitti and the Sitetracker team in 2018, we knew we had an Energize thesis-entrepreneur-future vision match. In addition to that thesis alignment, we also learned that the Sitetracker team had the level of customer respect and sales gumption required to win over the traditionally slow-moving critical infrastructure verticals. Critical infrastructure decisions move slowly by design: there can be no downtime and… once the product is in place… it is probably in place for a 20+ year relationship! The long-term investments that Sitetracker was making in 2018 into product and sales cycles drove us get creative when we led the Series B-2.

Since our investment, Sitetracker has continued to masterfully execute their plan to be the de-facto software platform for the next generation of critical infrastructure. We are thrilled to double down on Sitetracker and their progress. We are co-leading the $42M Series C alongside H.I.G Capital and are thrilled to bring them into the company. We are also happy to welcome new investors Deutsche Telecom Capital Partners, Energy Impact Partners and Clearvision Ventures to the cap table. Existing investors NEA, Wells Fargo, National Grid, and Salesforce Ventures also participated.

I joined the Sitetracker board during the Series B-2 and am excited to announce that our Energize Partner, Katie McClain, is joining the board as well. This is the first company where Energize holds two board seats and we are excited to double down Sitetracker’s growth efforts in the new energy economy.

Below is a press release that Energize wrote about today’s Volta Charging Series D.

While today’s announcement is a mini celebration along Volta’s EV journey… I have two items to elevate:

The line of success is never up and to the right.Rather, the story arc is a chaotic, meandering menace. To survive and thrive in the market swings of 2020 requires management and employees dedicated to the mission. Volta’s perseverance and growth in 2020 truly reminded me about the importance of mission and conviction. And Scott, Chris and the Volta team deserve a (brief) respite and congratulations for their efforts.

At different stages over the past 3+ years every member of the Energize team has helped with Volta. While Tyler and I are involved in board-related governance, I really enjoy how much team-driven support has gone into the investment. Katie has helped with policy intros and messaging… and pounded the table for increased investment in 2020. Juan has been steadily supporting financial analysis since our original 2018 investment. Tyler is a machine on key metrics, and utility introductions for the data product and Kelly is whipping together press and messaging as you read this. Even in his recency, Mark has helped with our most recent Volta investment. The best companies bring everyone involved along for the ride with a feeling of togetherness, and Volta has done that to Energize.

Energize Ventures is amped to announce its participation in Volta Charging’s $125 million Series D. This funding brings Volta’s total equity raised to more than $200 million.Goldman Sachs acted as exclusive placement agent to the company in connection with the financing. Energize managing partner John Tough will continue serving on Volta’s board as lead director, while principal Tyler Lancaster acts as a board observer.

Electricity will fuel the future

If you – like us – believe electric vehicles (EVs) will dominate the future of transportation, then ubiquitous charging infrastructure is required to power the movement of people and goods. We’ll need EV chargers at businesses, in parking lots and alongside highways, near supermarkets, stadiums and other places we all frequent. Volta Charging is meeting that need by building a free public electric fueling network “at the places you like to go.” How? Volta monetizes the network with advertising and real estate site partners, increasing the value of parking lot real estate and attracting EV drivers to the stores, shops, businesses and entertainment centers where they go.

In a wake-up call of sorts, COVID-19 has exposed that we can live with clean air by reducing or outright removing pollution caused by combustion vehicles. As we recharge our economy, it is more important than ever to accelerate the transition to electrified transportation. President Biden plans to push for legislation appropriating $5 billion to support the installation of more than 500,000 EV charging stations by 2030, according to Bloomberg Green. Rapidly electrifying the transportation sector will create thousands of jobs in construction and manufacturing, while cleaning the air in local communities at the places “you like to go.” We believe Volta is poised to lead as the most capital-efficient and highly utilized EV charging network in the U.S.

Capital-efficient EV charging infrastructure

Energize originally led Volta’s Series C in 2018, doubled down to lead the C-2 in 2019, and is tripling down in 2021 with this Series D. After closely tracking the EV charging market for years, we observed firsthand the challenges associated with building a profitable EV charging business by selling electricity or charging hardware alone. Like its gas station predecessors where most revenue comes from sales of coffee and snacks, the EV charging market was begging for a creative approach to monetize with revenue streams beyond selling electrons.

Enter Volta, whose brilliant business model not only can pay off infrastructure costs, but also drives industry-leading utilization – ensuring the EV charging infrastructure we build is actually used. Volta installs EV charging stations with large digital screens in premier parking spots, gives away electricity, and generates revenue from advertising and site hosts. That revenue has the potential to more than covers the costs of charging equipment capital and ongoing maintenance and electricity, which would provide healthy margins as well.

When Energize first met Volta founders Scott Mercer (CEO) and Chris Wendel (President) in 2018, they had deployed a few hundred EV charging stations in Hawaii and California to prove the model. Their team had grand aspirations to expand nationally, and we had plenty of questions on if and how they could replicate their success in other geographies across the U.S. The EV charging landscape was then littered with the corpses of failed pursuits. However, we gained conviction in the team’s single-minded pursuit to build a scalable, profitable EV charging business. We believed their striking product, superior unit economics and long-term contracts with site hosts were strong competitive moats.

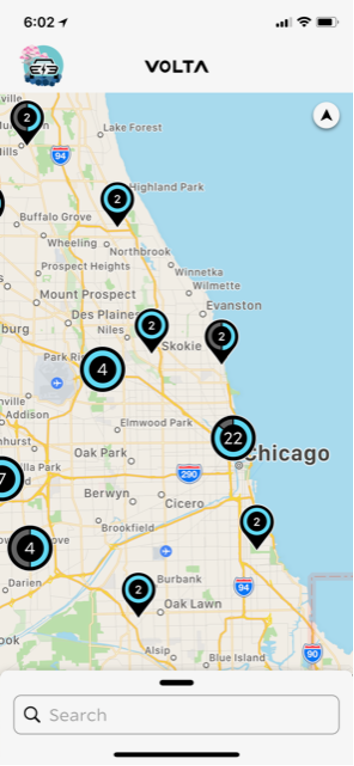

Fast forward to today: Volta operates a network of 1,500 EV charging stations around the continental U.S. – including 200 stations here in Energize’s home base of Chicago. The company recently launched a DC fast charging offering to complement its core Level 2 charging product. Additionally, Volta’s internal software can intelligently site EV charging stations, helping utilities evaluate the impact of electric vehicles on electricity demand and plan grid infrastructure upgrades. Volta truly is a full-stack EV charging network.

An EV charging pioneer reaches scale

The Series D capital infusion will enable Volta to expand their network by installing thousands of new EV charging stations – which we believe will create a ripple effect across the market and broader economy. Volta’s infrastructure will be a key platform to publicize the launch of myriad new electric vehicle options planned for release by automotive OEMs over the next five years. It draws EV drivers to retail locations, increasing revenue at a time when many local businesses are struggling. Hundreds of electricians and construction workers will help build and maintain Volta’s EV chargers, employing skilled trade workers on the heels of COVID. Investing large amounts of capital in Volta’s network will create tremendous benefits for communities and the environment, right when we need it most.

Congratulations to Scott, Chris and the entire Volta team on what they’ve built so far! Energize knows that this is just the beginning in the company’s mission to replace fossil fuel molecules with electrons, helping people get where they “like to go” entirely with electricity.

I prefer writing, but occasionally share some of my market sentiment through audio channels! And so, today I am pleased to share that I spoke with my “Industrial Exit Tracker” partner in crime on his podcast…

Ty Findlay @ IRONSPRING Ventures is the host of the “Heavy Hitters” podcast. The podcast speaks with investors and operators in/around the digital industrial ecosystem.

In this podcast we covered some lessons I learned from the initial energy investing wave. I also cover the internal evaluation parameters for an Energize investment… as well as some of the average statistics for our investments. And perhaps define a new term… “pre-growth”.

I recorded a podcast with Ty Findlay at @ironspringVC to share my pulse on entrepreneurial state of the energy & industrial markets. Lots of nuggets in here how @EnergizeVc works as well… https://t.co/9jApYTdbJf

About a decade ago scientists, entrepreneurs, government and capitalists unified to focus on decarbonizing energy generation. As a result, the cost curve for new power solutions plummeted.

As Michael Polsky says “nobody built renewables because they needed electricity”… the fact is that the cumulative we had to come together for the long term benefit of our environment and drive efficiencies and growth in a new technology. The cost to deliver utility scale wind, solar and batteries is now dropping 5-10% each year. The focus and execution of the “we” won.

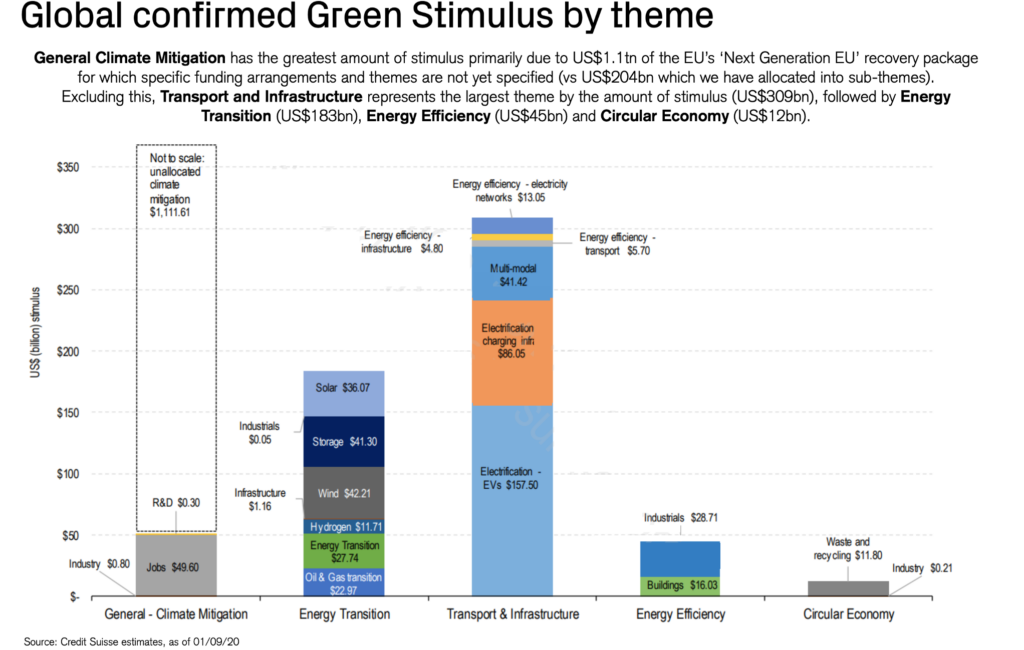

The same group of technology actors, policymakers and financiers is now focusing on the next sector: the decarbonization of mobility. Earlier this month Credit Suisse posted a report called “Energy Transition in 2021”

The most interesting page for me in the report is where the capital for the 2021-2022 “green stimulus” in Europe/US is focused:

“Electrification of EVs” “Electrification Charging Inrastructure” “Multi-modal transport support”… all about decarbonizing ground-based transportation

This capital towards EVs now far outpaces energy generation and industrial / building energy efficiency. Given our previous success effecting change in energy generation through focused innovation and investment in the 2010s, I am very bullish on significant changes ahead in our mobility sector. Whatever the “LCOE” equivalent for mobility… the cost of the decarbonized mobility solutions will plummet. Change creates opportunity and as electrification and hydrogen grow in usage, a number of new businesses and business models will emerge. New titans are being built now.

The scale of change ahead will make our current mobility market unrecognizable by 2030. Here we go!

An important industrial tech M&A event happened earlier this month: PTC acquired Arena Solutions for $715M… marrying PTC’s CAD software with Arena’s Product Lifecycle Management solutions.

The Acquirer

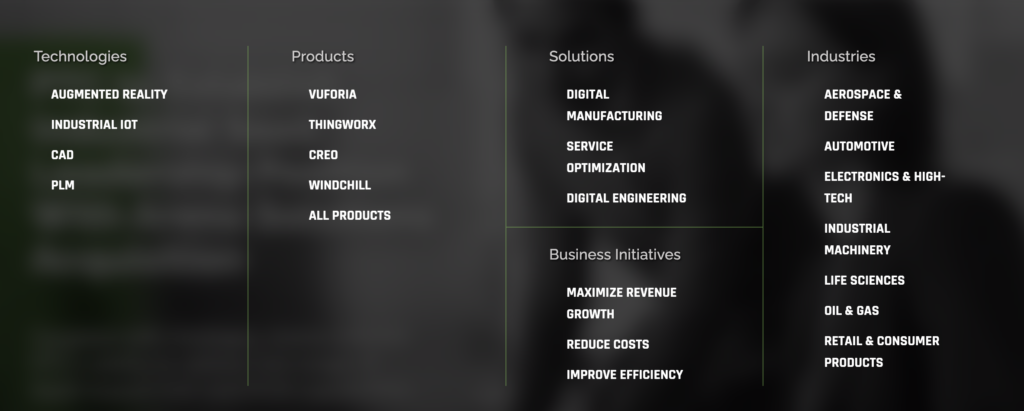

PTC is a pillar of the industrial technology scene. the company has nearly $1.5 billion in software and related services revenue. The company received a $1 billion strategic investment from Rockwell in 2018. PTC’s core products and solutions can be seen here:

PTC is currently worth approximately $14 billion in the public markets, implying an ~10x revenue multiple. The company’s valuation multiples are depressed relative to the stat-up comps due to the slower growth (sub 5%) for the firm.

But PTC has a very strong brand and strong existing customer relationships. Given PTC’s existing Onshape brand and that Computer Aided Design (CAD) expertise, it was a logical bolt-on as Arena’s Product Lifecycle Management (PLM), naturally works alongside CAD.

The Target

PTC claims that Arena will add $50M of recurring revenue for calendar year-end 2020, and no change in cash flow. This means that PTC acquired the company for 14x 2020 revenues.

1- There is a “sweetspot” where these larger industrial technology firms want to see a firm hit in revenue and it usually starts at the $40-50M in revenue range. Anything less than that amount and the target’s financial impact is too small to make an impact. And if the company is too small then the acquirer is concerned the existing culture will stall the start-up’s growth. Most industrial tech firms actually want these technology subsidiaries to retain independence.

2- Arena Solutions was probably growing closer to the OSIsoft benchmark of 10% yearly growth versus the 50-100% of most start-ups. PTC acquired Arena for 14x revenue… a healthy multiple but a far cry from other recent start-up valuations. This is an important lessons for the VC and start-up community: the industrial tech firms HATE paying big multiples. They would rather purchase a slower growing firm for a lower multiple than the market leader for an egregiously high multiple.

3- This was a 20 YEAR story. The firm was founded in 2000 and had its’ last venture round in 2014. These businesses take time to grow in the industrial technology space… plan accordingly.

The “built on Salesforce” technology stack now has a number of winners.

The original and most epic example is Veeva Systems. Veeva took less than $10M of capital, and is now a $41BN value company. The company was so efficient because it leverages the Salesforce infrastructure to build a vertical-specific solution. In the process, Veeva’s additional application layer gave hospitals and healthcare firms greater value… and charged a boatload more. The company has $1.4 billion of trailing twelve month (TTM) revenue and $340M of operating income. This represents a 30x revenue multiple and a

Since then, many other firms have come forward:

nCino is also built on Salesforce’s platform. nCino used the basic infrastructure and built a banking and finance focused operating system. The company is now a $7.4 billion public company with $170M of LTM. Not a shabby 40x multiple.

Conga and Apptus were some of the earliest platform adopters. These companies, now merged, have nearly $500M in TTM revenue and provide contract lifecycle management.

Today’s announcement by Honeywell brings another “Built on Salesforce” company to the forefront. Honeywell announced the $1.3 billion acquisition of Sparta Systems. The target company’s ore product is a quality management software delivered as a service with artificial intelligence. According to their website, Sparta Systems has “two primary platforms include TrackWise Digital, which is built on Salesforce’s platform, and QualityWise.ai. QualityWise.ai brings natural language processing, signal detection and confidence levels for recommendations to TrackWise Digital.”

The product will integrate with Forge, and the M&A is consistent with my past analysis of Honeywell’s digital strategy. Perhaps the most important part of the narrative, however, is Honeywell’s continued integration with traditional IT firms as Honeywell is already cozying up with Microsoft and now Salesforce. Given that Salesforce (and Microsoft) are where existing industrial customers go to shop for IT, Honeywell is wisely associating their OT stack.

With the $1.3 billion price tag and the other recent comps listed above I suspect Sparta Systems had somewhere around $40-90M in revenue. As the company has more implementations (non-software) revenue I suspect Honeywell paid a slightly lower multiple and the company had $60-90M of revenue.

I worked with Kevin Stevens at Choose Energy. He is now a Partner at Intelis Capital. According to Kevin’s website, Intelis Capital makes long-term investments in the next generation of energy titans accelerating the widespread adoption of novel technologies creating a more resilient and sustainable energy ecosystem.

Kevin recently wrote an excellent post about C3.AI and the company’s recent S-1. C3.ai is a leading enterprise AI software provider for accelerating digital transformation. The proven C3 AI Suite provides comprehensive services to build enterprise-scale AI applications more efficiently and cost-effectively than alternative approaches.

A company issues a S-1 as a lead into an IPO. Instead of doing my own analysis here, I wanted to elevate Kevin’s work.

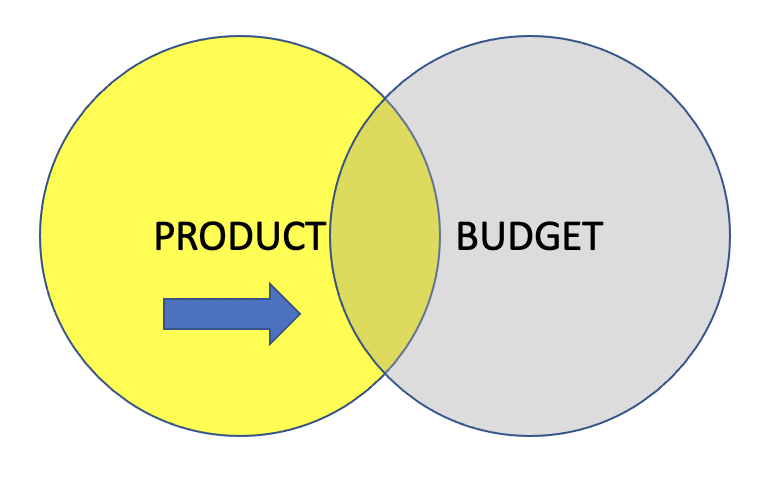

At Energize we are fortunate to see many next-generation technologies. As an investor with a commercial focus, I usually ask the entrepreneur something along the lines of: “what budget or line item at the customer do you think funds this technology purchase?”

Less commercially aware CEOs will answer this question by proclaiming of a new line item or a new approach to the customer’s budget. In my years of venture, this “create a new budget” approach typically leads to sales pain and capital inefficient growth.

The start-up’s technology may be next generation. And the start-up may be using NEW technology to solve an old problem in a NEW way.

However, the most experienced execs will do everything in their power to jerry-rig their technology solution to an existing budget.

Seasoned execs know that if a line item budget exists at a customer, the customer has previously determined they will pay (internal or external resources) for value delivered. By aligning the new technology solution to the outcome-validated budget, a startup backs into budget access and approval.

I call this product-budget fit.

The best start-ups think through product-budget fit from the earliest days of the company. With this awareness, a company fine tunes product development, go to market, and commercialization techniques accordingly. I enjoy seeing this narrative come together at a high growth company and Team Energize thrives in working alongside entrepreneurs at this stage.

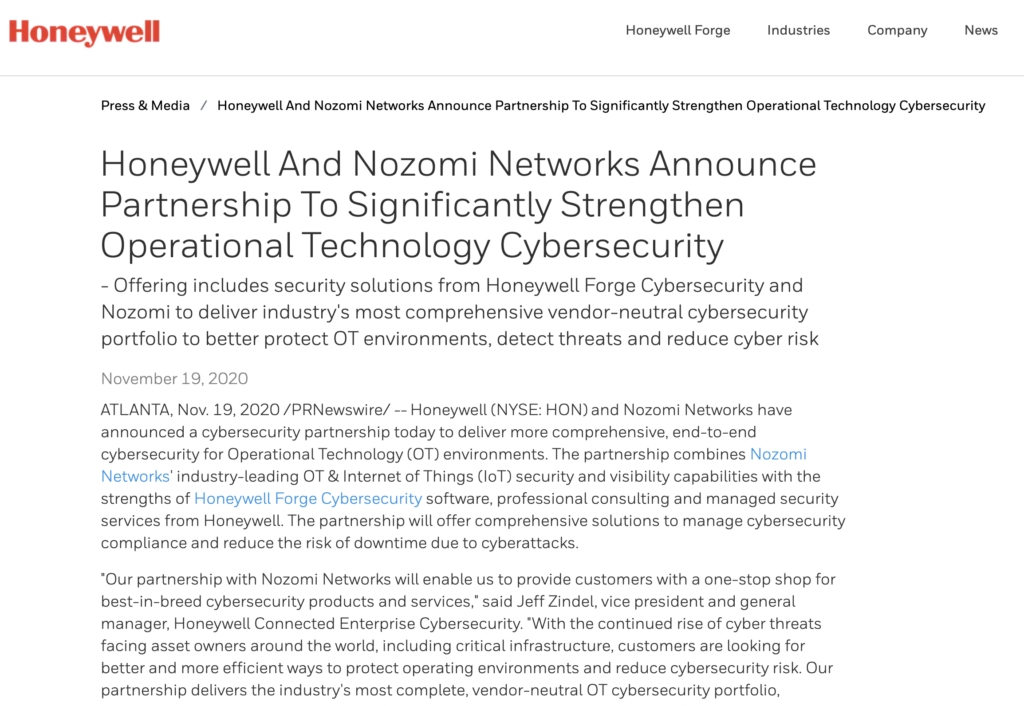

Digital Industrial Partnership: Honeywell Forge + Nozomi Networks

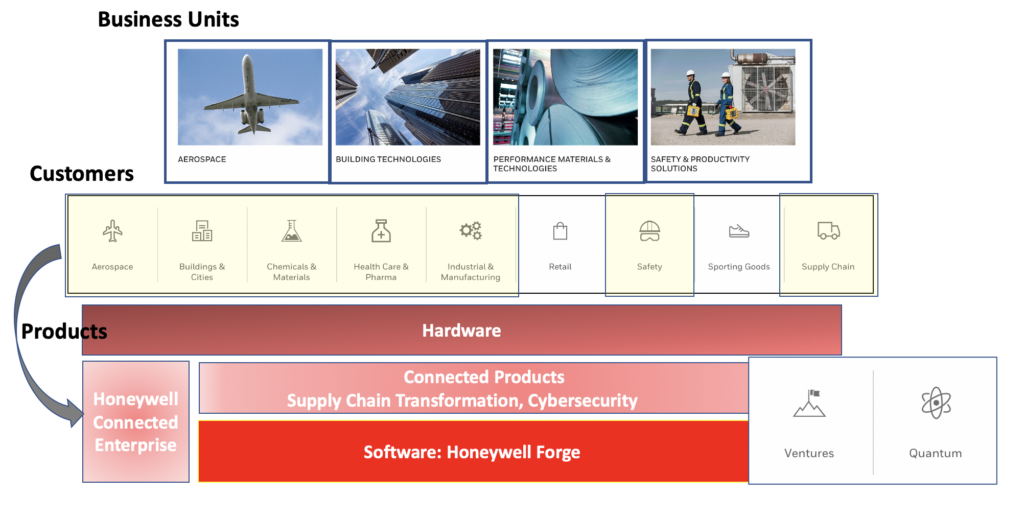

Honeywell CEO, Darius Adamcyzk, was also recently on CNBC touting Honeywell’s capabilities around control systems and digital technologies that blend hardware and software. At the bottom of this post is my framework for Honeywell’s approach to digital technologies. In their digital goals, Honeywell has stated interest in OT and IoT cybersecurity.

So what is a tangible example of Honeywell leaning into digital industrial solutions? Perfect timing…!

Last week Honeywell announced a partnership with Nozomi Networks to strengthen HCE’s Forge OT cybersecurity offering. Nozomi is a portfolio company of Energize Ventures and is the leader in OT and IoT security and visibility. Through a software platform, Nozomi accelerates digital transformation by unifying cybersecurity visibility for the largest critical infrastructure, energy, manufacturing, mining, transportation, building automation and other OT sites around the world.

I am very excited to see how Nozomi will succeed within Honeywell’s industrial network. Here is a screenshot of the press release.