In the past two weeks Energize has had job offers accepted by 3 new employees. One of them is a new investor and the other two are going to be taking leadership positions on our platform team.

We were 10 people going into last week and will be at/near 15 by the end of the year. In absolute terms, this isn’t a huge jump. But when you frame the growth from our baseline, a 50% growth figure seems meaningful.

One lesson I have taken from past operating experiences is that onboarding new hires well starts in the recruiting process. Given the small (but mighty) size of our team and the impact potential for each new hire, every single prospective hire was given an insight into our 10 year vision, and our “Energize Order of Operations”. We had incredible talent in the recruiting process. The reason we shared some of our internal materials with the potential hires was so we could screen for the ambition, culture and trajectory alignment. Our internal team expects to work together for decades to come. We wanted each new hire to see how and why they fit into the team.

The transparency in our recruiting process helped us really find the optimal individual across skillsets and I can’t wait to introduce them to you in the coming weeks. Each individual brings added intellectual, interpersonal, and geographic complementarity to our team. Hiring is also a signal to the market about the direction of the firm – and I look forward to hearing your feedback on what we are building over here at Energize.

Last week was pretty exciting for Volta. On Friday they celebrated their first day of trading under their new stock symbol, VLTA. I was at the New York Stock Exchange with the cofounders, Chris & Scott, other board members and many of their employees. We were there for the first trade and the closing bell ceremonies. It was my first time at the NYSE and Volta is now Energize’s first public company.

There are a lot of reasons to be excited about Volta’s future. I am excited to be staying on the board of the company for at least the next year. Why? The people. Working with Chris and Scott and the rest of the amazing Volta team is truly energizing.

(And as a note: as a public director I won’t be able to share much more about Volta in my ongoing posts. So don’t take my lack of coverage as lack of interest…!)

About 12 months ago the Energize team met Corey Capasso, the cofounder & CEO, of Urbint. He was raising a small, interim financing. We liked the company and we liked the management team’s practical approach to climate change mitigation. Urbint helps critical infrastructure providers asses and mitigate risk in their in-field project development. If you are long the energy transition you are long construction and replacing old, aging assets. Urbint helps critical infrastructure providers execute this building and replacement strategy more safely.

At the time we decided not to invest but gave Corey a list of 5 items that we thought he could improve for us to lean into a future round. The Energize team stayed in touch with Corey and one day a few months back he called us up (no emails with Corey!) and listed off the company’s step by step progress against our earlier benchmarks. The structure of the deal was complete in a few days and Energize and our LPs represent ~$40M of this $60M round. Why?

Energize is excited to announce we are leading the oversubscribed $60M Series C investment in Urbint, a leading operational risk management software platform. American Electric Power and OGCI Climate Investments also joined the round alongside existing investors Energy Impact Partners, National Grid Partners, Blue Bear Capital, and Salesforce Ventures. Energize principal Tyler Lancaster joins the Urbint board, and associate Eileen Waris joins as a board observer.

Aging critical infrastructure and climate change pose an existential risk

Our nation’s critical infrastructure is at an inflection point. Companies across the utility, oil and gas and telecommunications industries rely on vast networks of physical infrastructure that have been built out over time. Today, these assets are aging past their intended useful life, causing a host of new challenges for owners and operators. As critical infrastructure ages, assets fail at increasingly high rates and operations and maintenance costs balloon. All the while, asset productivity wanes. These effects are compounded by more frequent fire and flooding damage due to climate change.

As the U.S. makes commitments to improve and electrify infrastructure at scale, utility, telecom, and other critical infrastructure operators will need to make significant improvements to their maintenance practices. Urbint helps customers in these industries prevent incidents and reduce O&M costs by making risk-based decisions across core operational programs.

Predicting and stopping costly threats with AI

Urbint is the next-generation operational risk management software platform serving critical infrastructure industries. Urbint’s platform leverages real-world data and artificial intelligence to deliver a clear picture of risk in advance. Their software helps critical infrastructure operators and managers assess O&M-related risk based on probability and magnitude, enabling them to take action in the right place, at the right time, before an incident occurs.

Urbint’s suite of solutions offers energy and infrastructure customers products that enhance performance in three areas that matter most: cost savings, worker safety, and prevention and resiliency related to climate change.

Cost savings

In the U.S. alone, damages to underground assets cost midstream gas and utility companies $30 billion annually. Urbint’s risk management software helps utility customers reduce annual damage costs by 40 percent.

Worker safety

Only 45 percent of job-related safety risks are detectable by workers themselves. Hazards related to visible factors such as suspended loads, uneven work surfaces, or moving equipment are often easily identifiable to the naked eye. However, risks caused by unseen factors like temperature, pressure, or mechanical failure pose a bigger threat. Urbint uses AI to identify safety hazards and reduce the risk of serious worker injuries.

Climate change prevention and resiliency

In addition to Urbint’s cost-savings and safety-enhancing benefits, we are also excited about their ESG impact. The oil and gas industry is the second largest source of methane emissions. One of the leading sources of these emissions are leaks caused by aging natural gas infrastructure. To date, Urbint has prevented methane emissions equivalent to more than 80,000 metric tons of carbon dioxide from leaking into the atmosphere, by preventing third-party excavation damages to underground assets and identifying leaky or corroded pipes.

Sales-forward team with industry expertise

Energize first met the Urbint team more than a year ago. Since then, they’ve proven their ability to expand existing customer relationships and add logos with impressive capital efficiency. They’ve also cemented their position as a leading solution provider of risk management software for critical infrastructure industries like electric, gas, and telecom.

Urbint CEO Corey Capasso

Urbint has assembled a world-class team of entrepreneurs, engineers, and energy sector veterans. CEO Corey Capasso has successfully scaled and sold multiple technology companies. Urbint’s leadership team has decades of combined experience helping utility companies design and implement asset management strategies and scaling high-growth data-driven software companies. As they’ve grown, Urbint has continued to add their roster of experts in software, AI, critical infrastructure and energy.

What’s next for Urbint and Energize?

This new round of funding will fuel Urbint’s growth as it continues building a category-defining risk management software platform. With the Series C capital infusion, Urbint is well positioned to further build out a robust sales and marketing team. They will continue to grow market share in the utilities space, expand into new critical infrastructure sectors where risk management is a top priority, and invest in adding to their suite of world-class risk management tools.

We are excited to partner with this team and help them scale to meet growing global challenges posed by aging infrastructure and climate risk.

Electrifying Everything: No sun, no wind, no problem

The final piece of the renewable generation puzzle lies in geothermal, hydro and nuclear power.

The post below, released today, was written by Energize investors Tyler Lancaster and Mark Tomasovic. We are believers in the “electrification of everything movement” but far from ideological in our support of wind/solar/batteries. The fact is that the energy transition needs a menu of power sources to deliver quality, cleanliness and volume. The post below reveals how we think about geothermal, nuclear, and hydro power. Link found here as well.

By: Tyler Lancaster, Principal at Energize Ventures & Mark Tomasovic, Associate at Energize Ventures

Electrification is a key theme to Energize’s investment thesis. We invest in software and business model innovation, many of which directly contribute solutions towards decarbonization by means of electrification. In this blog series, we’ll explore this critical transition and the technologies driving and enabling it.

Solar, wind and storage: A killer combo, not a panacea

Solar, wind and storage are a killer combo. Together, they can decarbonize at least 80 percent of electricity supply in the U.S. Leading experts agree that “rapid cost declines for wind, solar, and battery storage have enabled a transition towards 80 to 100 percent clean electricity in the 2030 to 2035 timeline at a modest cost to electricity customers,” per a meta-study conducted by Energy Innovation: Policy & Technology LLC.

To transition the remaining 20 percent of electricity to zero carbon, we’ll need a combination of technologies that also can provide non-intermittent, dispatchable electricity. Nuclear, hydropower, geothermal, biomass or biofuels, or natural gas plans paired with in-situ carbon capture and sequestration (CCS) are prime candidates.

Where to find “zero-carbon, dispatchable, high-capacity factor” power?

We believe the first of these three — nuclear, hydropower and geothermal — will play the most important roles in complementing solar, wind and batteries over the next 10 to 20 years. These technologies display the necessary combination of input resource abundance (uranium, water, and the Earth’s heat, respectively), technology maturity and compelling economics.

Nuclear: Keep the plants running

When it comes to nuclear power generation, simply keeping existing plants open is the key. Today, 20 percent of power generation in the U.S. comes from nuclear. Solar and wind are not yet able to fully replace the energy provided by nuclear plants that are turned off. Unfortunately, most existing nuclear plants are increasingly uneconomic as levelized costs have ballooned by 23% in the past decade. However, turning them off can be massively costly for the climate.

Because it is so difficult and expensive to build new nuclear plants, we have essentially stopped building new nuclear in the U.S. for commercial operation. Novel nuclear technologies such as small modular reactors and fusion hold immense promise, yet are unlikely to be technologically de-risked, commercially available, or cost-effective in the next decade. When they are, they can join the decarbonization party. In the meantime, we should keep existing nuclear plants running even if subsidies are required. The alternative usually means higher emissions in the short-run, as we’ve seen in New York with the closure of the Indian Point nuclear facility.https://cdn.embedly.com/widgets/media.html?type=text%2Fhtml&key=a19fcc184b9711e1b4764040d3dc5c07&schema=twitter&url=https%3A//twitter.com/drchrisclack/status/1416180201424293893&image=https%3A//i.embed.ly/1/image%3Furl%3Dhttps%253A%252F%252Fabs.twimg.com%252Ferrors%252Flogo46x38.png%26key%3Da19fcc184b9711e1b4764040d3dc5c07

While keeping nuclear plants online is important, hydropower and geothermal are poised to play the largest role in filling out the remaining 20 percent in the more immediate future. Both rely on renewable resources — water and heat — that we already know how to use in electricity generation. The technology risk is therefore low, and simultaneously costs are dropping thanks to new technology-enabled approaches to increase efficiency, such as data analytics and edge computing.

Hydropower: Reinvigorating the original turbine technology

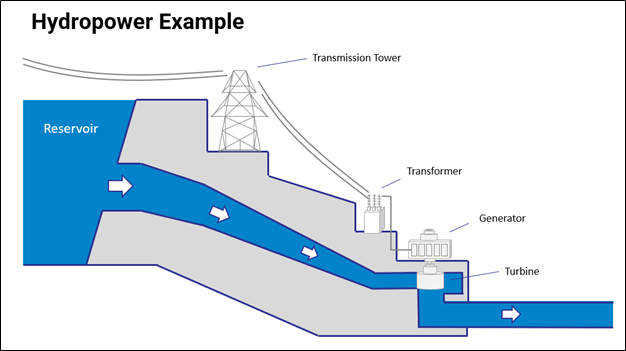

Today, hydropower generates about 16% of the world’s electricity usage, according to National Geographic. The energy source is clean, easy to ramp up or down to match electricity demand, and constantly renewed by snow or rainfall.

While there are a few types of hydropower, the most common type is called an impoundment hydroelectric plant. Impoundment plants consist of three parts: a reservoir of water, a dam to channel the water, and a turbine generator. Water from the reservoir is released through the dam to generate power and meet electricity needs (via Energy.gov). In fact, impoundment plants are incredibly efficient: modern hydro-turbines can convert as much as 90 percent of available energy into electricity. This is on-par with capacity factors for nuclear power, and twice that of typical gas and coal plants. Additionally, the life cycle of a hydro plant produces very little carbon emissions (USBR.gov).

However, there are still a few challenges associated with operating hydropower facilities. Just as generation of solar and wind energy is dependent on environmental conditions, hydroelectric potential relies on an adequate water level in the reservoir, which can fluctuate monthly depending on precipitation. For example, climate change is depleting water resources via decreased snowmelt in areas like California, thereby reducing hydropower output when it is needed most during high periods of energy demand in the summer.

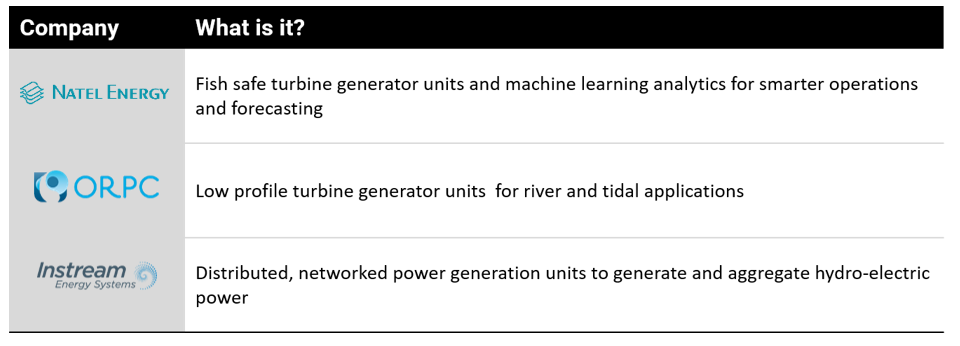

Like other critical infrastructure, maintaining and monitoring asset performance is key to operating hydropower facilities. Digital sensors connected to edge analytics platforms like ZEDEDA (an Energize portfolio company) can create feedback loops for predictive maintenance on turbine equipment. Companies like Natel Energy are even developing their own connected, fish-safe turbine generators that can operate in shallow rivers and communicate together to provide distributed baseload energy.

Hydropower is already one of the largest renewable resources in the world, producing more than 4,300 TWh of energy globally, and new technologies are enabling hydroelectric plants to improve system reliability and safely access new resources. Hydropower will continue to play a significant role in the energy landscape, providing a clean and increasingly reliable source of flexible electricity for decades to come.

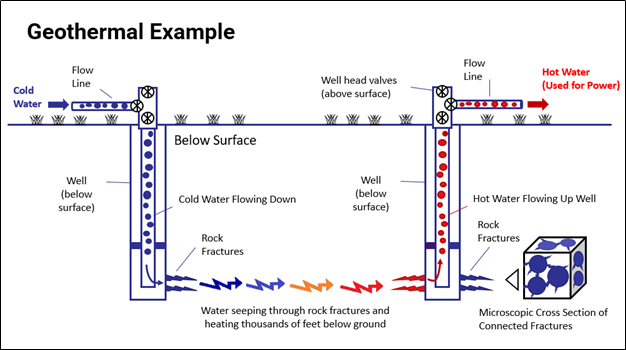

Geothermal: An underdeveloped renewable resource

The inside of the earth is hot. Deep within the mantle of our planet, radioactive elements are constantly decaying, generating over 30 TW of energy (An Introduction to Nuclear Waste Immobilisation). In fact, the earth produces so much energy that if we were capture all of its heat, we could power more than 20 billion homes every year. Geothermal energy is clean, green and reliable. So, the only question now is — how do we make it affordable?

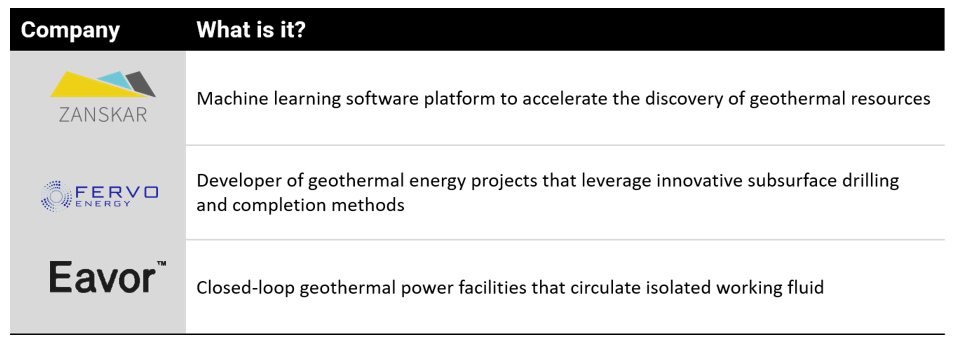

Geothermal projects must balance cost with resource quality. Drilling deeper to access better, hotter resources often increases the overall cost of the project. The goal is to find a hot enough resource close enough to the surface so that the project economics make sense. Using existing technologies, the U.S. has been able to find and develop about 3 GW of near-surface geothermal power. However, now that the obvious resources have been tapped, we need to improve prospecting capabilities to scan the earth for less obvious reservoirs. Companies like Zanskar are building data-driven software platforms to de-risk this geothermal exploration process.

Geothermal companies like Fervo Energy are using innovative drilling and completion methods to maximize the heat captured from the earth. For every mile we drill down beneath our feet, the temperature increases by about 75 degrees Fahrenheit. Using the earth as a heat exchanger, these companies inject cold water into wells thousands of feet deep. The water is warmed by the heat of the earth, and then exits through a production well where it can be used to generate power. These projects must precisely design the right size and depth of these systems to produce substantial energy while managing the overall cost of the facility.

“Fervo Energy incorporates proven technologies, like horizontal drilling and advanced distributed fiber optic sensing, into a novel geothermal system that delivers more predictability and lower costs than previously possible,” said Tim Latimer, CEO of Fervo. “This opens up new areas for geothermal development, right at the time when customers are demanding more 24/7 clean power. Geothermal has a key role to play in a fully decarbonized electric system, and recent technology breakthroughs will make that a reality.”

Finally, beyond using geothermal to generate power at a central plant, you may be able to offset some of your electricity usage by installing a geothermal system in your own backyard. Whether it’s summer or winter, the earth maintains a relatively constant temperature at a few hundred feet deep. New companies like Dandelion Energy have capitalized on this consistency by building ground loops to heat (or even cool) residential homes.

Geothermal is at a turning point. As with other renewable energy sources, regulators are now driving adoption of geothermal energy. The California Public Utilities Commission approved its plan to install 1,000 MW of geothermal energy by 2026. At the same time, new technologies are entering the market that support scalability — helping to decrease the cost of capital for geothermal projects and attract new capital to meet net-zero goals.

From energy generation to transmission and distribution

Solar and wind energy paired with battery storage are dominating the grid at an accelerating pace. If the renewable energy transition were a Broadway show, these three would be the rising stars. But we can’t get to 100 percent no-carbon electricity generation without several important supporting roles. Non-intermittent, flexible baseload power like nuclear, hydro and geothermal will be essential in keeping the lights on when the wind doesn’t blow and the sun doesn’t shine. We believe these secondary renewable energy sources are here to stay, and venture-backable technologies that can increase efficiency, lower costs and support scalability have the potential to capture outsized market share.

As I’ve iterated on before, decarbonizing by electrifying everything reduced to its simplest form depends on four key tenets:

I have covered the first bucket across solar, wind, batteries, geothermal and hydro. I argue these technologies are most critical to decarbonizing electricity generation over the next 10 to 20 years. Enabling digital solutions and software are playing a key role in reducing “soft costs,” accelerating deployment, and engineering new form factors of no-carbon electricity.

Casting forward, if we can “make” massive amounts of zero-emission, renewable electricity, then we’ll need a way to “move” it from oftentimes rural locations to the places it will be used — our homes and businesses.

In my next piece, I’ll cover the imperative to invest in electricity transmission and distribution. Digital technologies and software are playing an essential role in getting the most out of our existing T&D infrastructure. More to come!

Shanu Mathew is a Chicagoan whose interests overlap with the Energize thesis. I’ve been fortunate to know Shanu for a couple years now. Most recently he was at First Eagle, integrating ESG risks into their credit evaluations. Earlier this year he made the jump to Lazard, where he is now Vice President of Sustainability & Net Zero Research. My hunch is that he will be a well-known industry leader in the coming years.

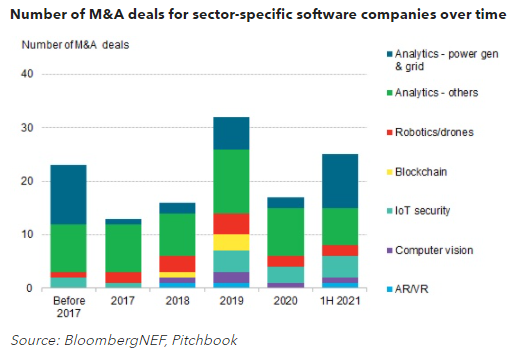

Just today he posted about a Bloomberg New Energy Finance report covering digital M&A. As his tweet link below shows, digital energy startup M&A is growing. We are on pace to hit 40+ exits this year, way ahead of the earlier record. The targeted verticals shown in the graph are our main areas of focus: power software, analytics, drones, IoT…

As industry’s digital transformation expands, I expect these themes will continue to be sought after M&A targets.

.@BloombergNEF analyzed 1,300+ digital energy startups and expects 2021 to be a record year for M&A

-25 M&A deals in 1H21, only slightly lower than 32 deals in the record year of 2019 -10 M&A deals in Power generation and Grid Software – main targets of acquisition pic.twitter.com/4DlUZGcgH5

Many of the best technology companies are product led companies. Why? Successful product led companies build product roadmaps by listening to customer needs. By delivering a product that solves a real and present need, the technology company can find a way to capture a portion of the expanded value being created for their customer. On the financial metrics side of the equation this results in strong net dollar retention and year-over-year (high margin) revenue growth per customer. As I have said on this site before, DroneDeploy is a pinnace example of product led growth.

DroneDeploy’s goal is to make drone data available to anyone, everywhere. The company is the leader in aerial drone software and has grown to be the leading aerial mapping, control and analytics platform. With thousands of customers, DroneDeploy continues to add several new products per quarter. Through ongoing customer engagement, DroneDeploy started to hear interest in having DroneDeploy expand to a more robust inside/on-the-ground product suite.

Enter Rocos, the leader in ground-based robotics management… and yesterday DroneDeploy revealed they acquired the company. The combination of DroneDeploy and Rocos is going to accelerate digital transformation for our critical industries. Large firms in the construction, agriculture, and energy industries are looking to simplify reality capture and this acquisition will allow DroneDeploy to present a single ground-to-air drone mapping, control and analytics platform.

Mike Winn, cofounder & CEO, is an extremely thoughtful leader at DroneDeploy. During the M&A process Mike focused as much on the product expansion, as well as the culture fit. It is clear that with David Inggs (cofounder & CEO) and the Rocos team now onboard, the teams are well-aligned and we are going to see even faster customer-led product innovation.

DroneDeploy has acquired Rocos, a New Zealand-based robotics software company. The acquisition will enable DroneDeploy customers in construction, energy, agriculture, and more to deploy and orchestrate both aerial and ground robots on their job sites. This acquisition will make physical workflow automation possible, creating more efficient and safer workplaces.

“Companies are undergoing a digital transformation accelerated by challenges surrounding labor shortages and COVID-driven remote operations. As a result, the market demand for automatic site documentation and digital twins has soared,” said Mike Winn, CEO and co-founder of DroneDeploy. “With the Rocos acquisition, we are enabling our customers to automate ground-level data capture, moving several steps closer to a complete automation solution.”

DroneDeploy is already the market share leader in drone software, powering the world’s largest companies to capture an instant understanding of their assets and operations through aerial imagery. Now, with the extension to on-the-ground robots, workers will soon be able to establish automated routines within the platform from both the air and the ground. For example, a solar technician could program a drone to fly over a solar power plant, identify thermal hotspots, and automatically activate ground robots to walk under the hotspot to identify the exact problem – no human intervention needed. This process will save time, resources and human labor, freeing workers to focus on other tasks.

“A few years ago, drones made the leap from hobbyist toys to enterprise tools. Now, ground robotics is on a similar trajectory,” said David Inggs, former CEO and co-founder of Rocos, now DroneDeploy’s Head of Ground Robotics. “With the addition of the Rocos’ ground robotics technology, DroneDeploy can now automate critical data workflows across both air and ground use cases, enabling greater safety and efficiency for the whole worksite.”

DroneDeploy has already begun integrating Rocos’ robotic control with its indoor data processing technology to deliver autonomous 360 Walkthrough and inspection at scale. The company will launch the new offerings at its annual DroneDeploy Conference this October.

The acquisition follows DroneDeploy’s recent $50M Series E funding round and continued growth, as enterprise drone data collection operations increased 95% in Q2 2021.

Energize has recruited a group of Summer Associates every year since 2017. We run a rigorous recruitment process and try to give the rising associates as real a full time investor experience as possible.

This summer we had two MBA interns and one undergraduate intern. The effort and contribution from this year’s group has been exceptional and complementary to our existing skillsets.

Both of our MBA candidates are from Columbia Business School and have made intermittent trips to Chicago. Each Summer Associate worked on active investment opportunities (new & follow-on) and created a lengthy deep dive. We begin our summer experience by sharing as much about our thesis with the group and then have the Associates interpret our areas of interest for a “greenfield research idea” that will encapsulate their internship through a 10-week deep dive. I just got the final work product from Honour Masters as she is presenting it to our team later this week. She covered how satellite related applications will impact the sustainability transition. The work product is ⚡️ and we can’t wait to share it with you in a few months. There is no doubt an Energize investment within the thesis and I am sure she has the company in her market map.

I parlayed my undergraduate summer internship into a full time role at UBS. And I had a similar outcome from my first hiring at KPCB and my eventual joining Choose Energy. I believe these programs are the best way to get to know a candidate over a lengthy period of time and imagine Energize will leverage this extended internship structure for all of our post-MBA hires going forward.

(I will cover the other summer associates over the coming weeks)

Energy Transition M&A: Aurora Solar acquires Folsom Labs

The next generation energy software firms are going to look quite different than yesterday’s leaders. Aurora Solar is the pinnacle of the next generation and the company’s leadership understands the importance of our increasingly distributed energy landscape. As a result the firm has been investing heavily in building great software products to accelerate that future.

While the energy industry is physically changing, another important change is the arrival to energy of the unique value creation and concentration structure of software companies: the leader in a software market delivers and captures the majority of value creation. With that framework in mind, Aurora Solar today announced the acquisition of a complementary platform and is compounding their lead in the solar software market.

Energize led the Series A in Aurora Solar and participated in the Series B and Series C. Outside of the cofounders, Energize is the largest shareholder and we have invested across our ventures fund, our growth fund and a number of SPVs. We will continue to invest in the company until they reach the public markets.

The details and links are below:

Aurora Solar, the industry’s leading software platform for solar sales and design, today announced the acquisition of Folsom Labs, the developer of HelioScope, the leading software solution for the commercial solar sector.

“Aurora Solar and Folsom Labs share a common mission to build a future of solar energy for all. We built our business to help the solar industry scale through technology, and adding the Folsom Labs team puts us in an even better position to drive the digital transformation of the solar industry.”

Christopher Hopper, co-founder & CEO of Aurora Solar

“Today is a big day for solar. As a result of this acquisition, solar professionals from the residential and commercial sectors can look forward to faster product innovation and an unparalleled customer experience. I’m delighted to welcome the Folsom Labs team to Aurora.”

This morning President Biden and a number of US automakers announced a target of 50% EV market share for new car sales by 2030. The target is voluntary … and mostly meaningless. Why?

#1- Auto OEMs like Ford and GM were already spending towards that figure. GM has indicated a $30 billion budget for EV development. Ford followed suit with a $25 billion EV capex budget and is positioning their iconic F-150 and Mustang vehicles as EVs.

#2- These targets are (correctly) voluntary and OEMs still need to convince the public to purchase these cars. To help consumers make the gas to electric habit shift, these OEMs need to deliver on their platform promises with GREAT cars … but also must better enhance the EV network. That enhancement means providing greater certainty of charging networks and EV-specific services. Gaining mass market momentum is not just about the car, but about creating a travel ecosystem that consumers can trust. I believe all areas will require investment.

There is an article this morning from the Wall Street Journal on this target:

Perhaps the highlight of the article was the quote below, that just shows how hard it is to predict the future – and how much federal targets have changed in 15 years.

“A decade ago, we were talking about reaching around 50 miles per gallon of gasoline in 15 years,” the official said. “Today for new autos, we are talking about reaching around 50% of vehicles that don’t require even one gallon of gasoline to go a mile in less than a decade. This is a paradigm shift.”

Energize runs our investment process by focusing on deep dives. We engage our broader network (many of which are LPs) to figure out what problems that they are trying to solve, and the location & scale of the budgets available to solve those problems. We use these unique insights to then identify and map market deep dives.

A 2020 engagement with our network led to interest and budget allocations for GHG tracking and implementation solutions. Eileen Waris, an incredible associate on our team, took the lead on the research effort and put together what I believe is the most comprehensive emissions tracking market review and company map.

Yesterday Eileen posted a summary blog of her deep dive on our Medium Page. You can find it here: What is Driving a New Wave of Carbon Emissions Platforms. The deck our LPs will see has nearly 60 pages of analysis and I am certain we have a couple future investments from her analysis.