Yesterday’s post covered how software companies improve their marketing and pricing structures by framing value in revenue growth, as opposed to savings. For the industrial and unregulated energy markets, this framework works about 90% of the time. But, like all good rules, there are a few exceptions. Topline alignment does not work when the product’s value is allocated to any of the following:

Regulatory / compliance

Environmental impact

Cybersecurity

The value-based exception occurs here because the return on investment for each of these product types is either

government defined or

addressing a long-tail, difficult to price risk

Most energy & industrial firms look at spend in these areas like insurance policies. With this uncertainty, firms hire consultants to recommend resource allocation and ensure that the corporation is investing sufficient resources (not more, not less) versus their peer set.

This causes two unique dynamics:

Incredible purchasing influence by channel partners in these areas

Underinvestment in long-term risks… until the risk shows up on the front door. (Think: a cybersecurity hack, long-term emissions impact, etc.)

If you are a startup serving these markets, it is especially important to retain policy advisors, immediately double down on channel partnerships, and most importantly: find a supplemental way to quantify your product’s impact beyond the initial, seemingly arbitrary cost line item. By creating a new form of value, a start-up in these verticals has the potential to control their pricing. I call this “supplemental value” the “Rule of AND”. Here are a few examples:

The best companies in cybersecurity will offer their cybersecruity solution and also create an additional narrative around operational visibility. (positively impacting operational uptime = higher revenue!)

Similarly, the best companies in environmental impact reporting report impact and will attempt to make product and supply chain recommendations to lower materials costs. (positively addressing materials= lower costs)

Energy Transition is Graduating to a New Common Goal

Start-ups love a common enemy. Usually that villainous figure comes in the form of the old guard. And in the energy transition it is no secret that the old guard was the oil & gas industry.

Over the past decade, our newest energy companies have been in a grueling 10-round boxing match versus the old guard. The metrics that measured progress on the scorecard were terms like. “levelized cost curves”, “fully delivered costs”, and market share. Well, with the recent news that Exxon is halting employee contributions and Occidental Petroleum is selling assets to pay down debt it is increasingly clear that the battle is over. Renewables will win. Electrification will take over mobility. And even the most traditional coal utilities are accelerating their energy transition.

What happens next? How can we unite the old and new guard of the energy transition?

In the last battle the new guard’s tactics to beat the incumbents relied focusing on “reduction“: on lowering a cost curve to beat carbon-based power sources. I believe the focus for the energy transition has to move exclusively towards GROWTH metrics… and specifically economic advancement figures like jobs and training. Why? The most powerful industry movements find ways to simultaneously strengthen their local communities, amplifying the overall impact:

Energy transition requires major capital investment

Capital investment propels corporate growth

Growth creates jobs and economic opportunity

Jobs support families

Families support communities

As a community, we should be carefully tracking and celebrating every new 1 million people employed/supported by the energy transition. I believe we will be getting the best of the next generation to join this opportunity as very few career opportunities have aligned economic, environmental, and social impact. We should celebrate this generation’s arrival.

Recent data from the EDF shows that there are approximately 1 million people working in the new energy industries, while Clean Energy Trust points to over 600k jobs in the midwest alone. Assuming that our energy transition jobs number is 10x in 20 years, what systems can we invest in now to support personnel advancement? These are questions we are thinking about at Energize and if you are working on any of the following digital technologies and how they will educate and grow a workforce, please reach out.

If Detroit in its’ prime was the center of the auto industry, I can argue that there should be 50 smaller “Detroits” around the country at our renewable energy hubs. And each hub will create economic opportunity. That is a goal we can all hope to achieve.

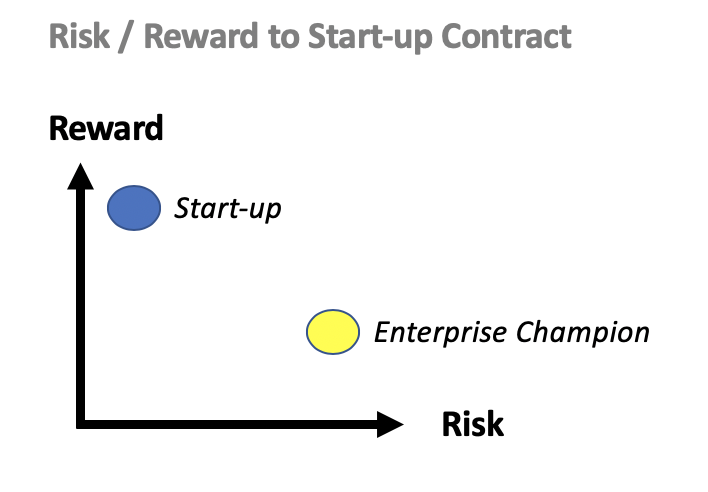

Why BD Partnerships work so well in Energy & Industry

Misaligned incentives make it hard for senior corporate executives to fully lean into championing any new software solution or digital technology. Here is a simple risk/reward matrix for the start-up and enterprise champion:

What is the biggest driver for the delta between the risk/reward of a start-up contract between the two parties? Time.

In the early stage environment the most rewarded moment is the close of the customer sale. In the corporate environment, the winningest moment is potentially years later when the product is implemented and Return on Investment is documented.

Given the big difference in time between the definition of success , employee tenure becomes the 🔑 issue: a Fortune 500 energy, utility or industrial company tenure is between 5-10 years, while a SV startup employee is approx. 2 years.

When an internal champion at at Fortune 500 energy & industrial company is willing to take a bet on a startup, he or she is looking to see if their counter-party will be around for a multi-year engagement. Product implementations on operating assets and systems are complex and require disparate integrations. Unfortunately, most large companies now have horror stories of identifying a start-up only to see the relationship manager … or even the entire company… vanish overnight.

With that scar tissue, most F500 now require channel partners to be the bridge and systems integrator for new technology products being added to their network. Big companies add these partners to buffer against the less stable start-ups. Therefore, I recommend that commercializing startups employ a few tactics to remove the mismatched TIME risk most corporates feel:

Build BD and channel partnership relationships early

Develop implementation and customer success teams early to show your you are committed to the long-term relationship

Feed your channel partner: bringing potential customers accelerates a partnership

Develop co-branded Go To Marketing stories with clear RoI

2 Sucker Sales Fails New Execs Make in Energy & Industry

I see startups make repeated mistakes when they scale in the energy & industrial verticals. Here are a few sales “No-Nos” to avoid…

#1 NO FREE PROOF OF CONCEPTS OR TRIALS...!….!

Energy and industrial firms broadly act like critical infrastructure providers. These firms are process oriented. Most of these companies thrive off of hierarchy, structure and process. Budget in these verticals for new technologies does not magically appear over night. If there is going to be budget for a real contract, there ABSOLUTELY will be budget for a Proof of Concept. If you are developing your sales pipeline and cannot identify the budget with your champion, move along. (And yes, I recognize that in some other industries a non-paid PoC can generate a contract more easily) In my decade within the early stage energy & industrial market, I can count on one hand the number of free pilots that expanded into an enterprise deal.

#2 Do NOT move your cloud provider for the promise of customers or a re-seller agreement.

I have seen some very lofty customer introduction and reseller promises from the cloud divisions of Google, Amazon and Microsoft. Every one of these firms will say something like this:

“Jeez, we have a Fortune 100 energy company that is asking us to help with their broader tech adoption. Those firms trust our recommendation. We would love to make that introduction for you, but you have to be on our cloud…”

These statements from the cloud sales execs are effectively hollow bribes.

And early start-up execs fall for it, subsequently invest a huge amount of money into transitioning their cloud provider… only to get crickets. You, Mr or Mrs. Start-up executive are the customer, not the provider. Unless they promise you years of free compute, stay away from these discussions.

Early on in my venture career I asked a very experienced VC investor why we were guiding our portfolio company executives to towards an 18 month runway between rounds.

The answer I received was that 18 months is the approximate time it takes for a company to hire and develop a team, and run two successful sales cycles. The reason? Two successful enterprise sales cycles should show market adoption, new feature feedback, cohort growth and, of course, revenue growth and early signs of operating leverage. With success, a company’s progress and team development over the 18+ months de-risks an investment. And the future upside and opportunities available to the company should be more clear, resulting in a higher valuation.

Unfortunately, this timeline prescription doesn’t fit well when a technology company serves the energy & industrial customer base. The fact is that these industries have longer sales cycles: usually around 9-12+ months. While accounts are ultimately bigger and worth the acquisition investment, the sales cycle is deliberately slow. Critical infrastructure firms use a slow decision process as a feature, not a bug. Everything has to work, perfectly.

Given these sales cycles and the need to better curate a startups go-to-market team, I generally recommend a minimum of 24 months runway between rounds for our investments. And for companies early in commercialization, I recommend that the execs slow down sales hires until more of the narrative and value proposition is quantified and marketable. These industries are slow to adopt technology, but once a solution proves value, the broader industry rushes to adopt the solution. And that ultimate payoff is worth the extended runway.

In recent weeks I have been speaking with an incredibly talented investment professional. Our discussions involved her correct observation about the slight evolution of the Energize investment thesis.

During the early days of Energize, our investment strategy was narrow and predefined: invest in digital technologies that make clean energy more affordable, reliable and secure.

Over the past few years we have intentionally moved from that predefined outcome and language. Rather than attempting to monetize a self-selected outcome (clean energy) we now focus our process on enabling the energy and industrial transition. Our new mission is: Accelerating digital innovation for energy & heavy industry. And with this mission, there is no goal line. There is no preordained, final outcome. Just continued improvement and adaptation.

These are big, complex markets that are under stress and technology-imposed change. And when big markets undergo change, technology firms can rewrite existing economic pathways and generate great returns.

I am comfortable saying that we are not smart enough to know how energy & heavy industry’s story will meander over the coming decades. But Team Energize is smart enough to monitor, research and maintain industry connections along the way so that we can make the most informed decisions. Coupling that learning approach with our Energize Engine approach to investment decisions and I am pretty excited for the part that Energize will play in the energy & industrial transition.

There are nearly 300 companies within the Fortune 1,000 that are broadly characterized by an industrial focus. The medium revenue for these economy-anchoring firms is nearly $4.9 billion, resulting in over $9 trillion in market capitalization. But revenue growth in this space is a far cry from the 20%+ range of the high-tech software companies beginning to dot the economy.

Given the total addressable market and slow-moving perception of these industries, many market-hungry start-ups attempt to attack (or serve) this industry. But, running a technology company to serve the industrial verticals contains many hidden traps. In fact, the slow operating and decision pace employed by industrial or critical infrastructure companies is a feature to their modus operandi, not a bug. Due to the large installed or operating asset base, industrial companies think in decade-long, multi-cycle returns and the capital and customer decision procedures are not meant to reflect one particular market moment.

The entrepreneurs that best address the industrial verticals tend to bring some domain-specific frustration, and many are returning to their materials-heavy industries with innovative software services and platforms in an attempt to modernize operations and add value to customers. And while meaningful change can appear frustratingly slow, industrial incumbents that operate primarily in atoms are beginning to feel the attention of bit-bearing software companies.

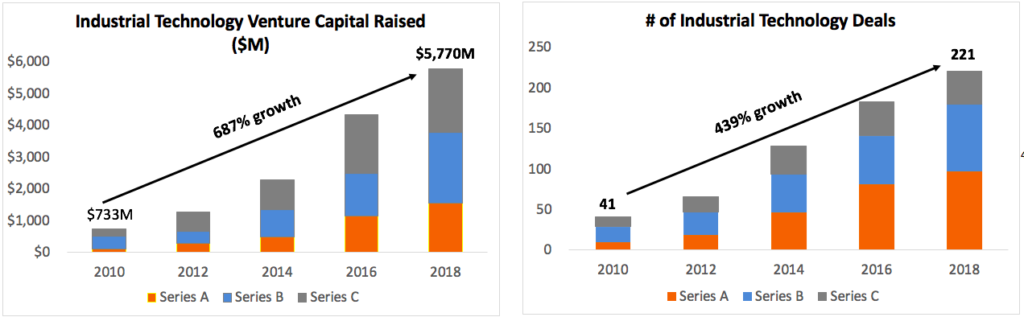

But just how much Series A-C venture capital attention have the construction, power, & energy, logistics & transportation, advanced manufacturing, and resource industries received?

That’s right: last year nearly $6 billion went into Series A, B & C start-ups within the industrial, engineering & construction, power, energy, mining & materials, and mobility segments. Venture capital dollars deployed to these sectors is growing at a 30% annual rate, up from ~$750M in 2010. And while the $6 billion figure is notable due to the growth of VC dollars invested, this early stage investment figure still only equates to ~0.2% of the revenue for the sector and ~1.2% of industry profits.

The number of deals in the space shows a similarly strong growth trajectory. But there are some interesting trends beginning to emerge: the capital deployed to the industrial technology market is growing at a faster clip than the number of deals. These differing growth trajectories mean that the average deal size has grown by 45% in the last 8 years, from $18 to $26 million.

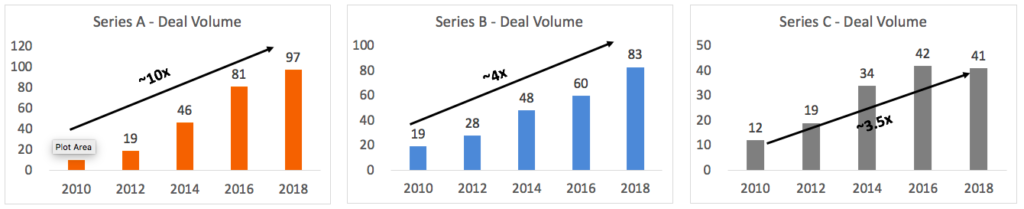

The Detail by Stage

Median Series A deal size in 2018 was $11M, representing a modest 8% increase in size versus 2012/2013. But Series A deal volume is up nearly 10x since then!

Median Series B deal size in 2018 was $20M, an 83% growth over the past 5 years and deal volume is up about 4x

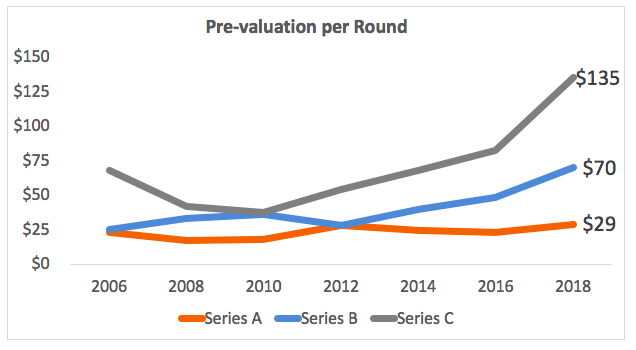

Median Series C deal size in 2018 was $33M, representing an enormous 113% growth over the past 5 years. But, Series C deals have appeared to reach a plateau in the low 40s, so investors are becoming pickier in selecting the winners

These graphs show that the Series A investors have stayed relatively consistent and the overall 46% increase in sector deal size growth primarily originates from the Series B & Series C investment rounds. With bigger rounds, how are valuation levels adjusting?

Growth in pre-money valuation particularly acute in later stage deals

The data shows that valuations have increased even faster than the round sizes have grown themselves. This means that management teams are not feeling any incremental dilution by raising these larger rounds.

The average Series A round now buys about 24%, slightly less than 5 years ago

The average Series B round now buys about 22% of the company, down from 26% 5 years ago

The average Series C round now buys approximately 20%, down from 23% 5 years ago

Some of my conclusions

Even with the growth in capital deployed, dollars invested as a portion of industry revenue and profit allows for further capital commitments. More entrepreneurs (& VCs supporting them) are likely to come knocking on the industrial gate

There is a growing appreciation for the industrial sales cycle: investor willingness to wait for reduced risk to deploy even more capital in the perceived winners appears to be driving this trend

Entrepreneurs that can successfully de-risk their enterprise through revenue, partnerships, and industry hires will gain access to outsized capital pools. The winners in this market tend to compound

Uncertainty still remains about exit opportunities for technology companies that serve these industries. While there is anecdote (PlanGrid, Kurion, OSIsoft), we are not hearing about a sizable exit from this market on a weekly or monthly cadence. This means that we won’t know for a few years about the returns impact of these rising valuations. Grab your hard hat!

*Data pulled from Pitchbook, scope available by request

With the digitization of traditional industry, software solutions are increasing their focus on the energy and industrial verticals. At the Invenergy Future Fund we are seeing many pitches a week for companies seeking capital to grow their business. As part of our diligence, we like to sit in on a few sales calls – usually to prospective customers that we introduce. Through those calls, we have seen three common mistakes that start-ups make while pitching traditional industrial firms. We list them below to serve as a guide of pitfalls to avoid:

1) Buzzword blockers: Many sales decks pitching the operations, maintenance and security divisions of traditional industries read the same… some newly formed version of technology (MACHINE LEARNING! ARTIFICIAL INTELLIGENCE!) could dramatically improve business results. The problem is that these buzzwords talk about your company’s solution, and not the customer’s problem. The customer does not necessarily care how the problem is solved, just that the results will improve. To paraphrase a statement I recently heard from an energy executive: “what makes this solution better than the 20 other AI software companies I have been pitched this year?” As a growing start-up you are better served cutting the jargon and delving straight to results and focusing on how you will get to a proof of concept within the customer’s desired timeframe. Remember, your technology is merely a tactic to serve the customer. The real product is the problem you are solving for the customer.

2) Hubris hurts: Energy and industrial firms have been solving maintenance, throughput and security problems for decades. Yes, the technology environment is changing. But within these Fortune 500 companies there are seasoned executives who have developed impressive IT and software systems based on an accumulation of historical technologies that manage billions in assets. No new technology solution is going to completely rip & replace existing software. Start-ups that expect to dramatically replace existing software architectures and make generalizations about weakness of existing solutions simply have not done their homework. Respect the reasons that current solutions are in place by identifying existing strengths and demonstrating new, complementary capabilities. The professionals who made those architecture decisions were operating with then-existing resources and are likely still somewhere in the organization.

3) Deliberate (business) development: In-the-ground or under construction assets have detailed, expected lifetime performance metrics based on the technology and environment for when the asset was implemented. Given those strict performance expectations, a large company will only trial a new, unproven technology on a select number of assets whereby the test will not materially impact overall results. It takes time for the prospective company to identify those sites for your software and it takes time to encourage the internal P&L owner to take on the potential risk. Bake that “discovery period” and longer sales cycle into your revenue projections. The beauty to this structure is that if the software does work as expected, then the concrete data enables implementation across the rest of the asset fleet within a surprisingly abbreviated timeline. As a result, the longer sales cycles of the energy & industrial world can actually be a feature, not a bug of the purchasing decision.

We hope you find these insights helpful. If you are a software company targeting the Industrial IoT segment looking to scale your business, please reach out as we would love to share thoughts, make some introductions and help further optimize the industry.

As I wrote about last week, Choose Energy was sold earlier this year. Beginning in 2015, Choose Energy had multiple casual M&A discussions. But, we did not formally engage until we knew we were ready as a company.

With a few months delay giving me a bit of clarity, I wanted to share some advice / insights that stand out to me about the process and how to prepare for our own deal:

M&A is hard. Very, very hard. Finding the right buyer, at the right price at the perfect time in their strategic initiative game plan is rare. Choose was lucky in that the company had inbound interest. And even then, not easy. (Jason Lemkin at SAASTR has documented just how hard this can be for companies with ARR type revenue and how they should aim to sell at local maximums.)

A clear internal deal champion at the acquirer is required. And you need that individual and their team to have a clear path to continued success after the deal.

Deal fatigue is real. – for both sides. I have raised Series B & Series C capital from a combination of strategic and VCs. Those processes are time consuming. M&A is double or triple that. Have a great team in place, hire great advisors and have an experienced CFO. (We were lucky to have David Yi, a serial KPCB CFO) The amount of work is unexpected, even for someone like me that expected it. To get through it you really do need to create a bond with the acquiring team and “gang up” on the advisers. Part of their job is to be fall guy so the buyer & seller can rally around a common enemy 🙂

Be prepared for regulatory requirements. For companies in the energy & industrials space that capture proprietary data and engage with federal and state level regulatory bodies, be prepared! Good process as you grow the company saves you from some major headaches down the line as lawyers dig through diligence and process documentation. Again, hire a great CFO, even part-time.

Enjoy the ride. There is something very odd about the completion of a sale. You go from being independent and controlling the asset to suddenly having a disbanded board and an entirely new organization structure, reporting structure and incentive structure. Even if your acquirer provides barely any oversight post acquisition, there is still a mental change. For me, this was one of the oddest feelings… and I liked our acquiring team! Enjoy those last few months of corporate independence.

Once a deal is complete there is an entirely new set of issues to address around corporate communications for employees, customers, service providers, and regulatory agencies. I will write about that experience in the coming weeks.