The Energy Transition’s 3 Winning Themes of 2020

I am going to be writing a few 2020 summary notes / awards. Today is “the winning themes!”

Theme 1: Infrastructure Development

Hard assets get a bad reputation in VC. This negative reputation is self-inflicted by the early stage venture community: investing in infrastructure and expecting venture returns. The fact is that there are better financing sources for the infrastructure layer. And in 20200, renewable infrastructure went into overdrive. Here are just a few of the headlines.

Invenergy announced a 1.3 GW utility scale solar project in Texas, the largest utility-scale solar farm in North America.

Orsted and others are building the first sizable, offshore wind farm in the US. The site outside of New Jersey, is targeting 2.4 GW and the winning bidder will build a $250M+ manufacturing facility in the state.

Hawaiian Electric announced 460 MW of solar and 3 GWh of energy storage with a number of winners: AES, Longroad Energy, Onyx, Hanwha Energy…

Theme 2: Hardware

Installed wind, solar and batteries are expected to increase by >10x over the next decade. TLDR: A lot of hardware and components are going to be installed. The last generation of energy had dominant energy brands. This generation’s brands are being established now:

Array Technologies became the first publicly traded solar tracker and received incredible interest with record-breaking follow-on issuances.

Enphase Energy shattered the “inverters are commoditized” notion, gained market share and margin as the #1 systems hardware firm supporting utility scale solar’s undeniable growth.

GE re-establishing dominance in wind and is building a stunningly effective and iterative new Haliade-X turbine platform with recent indications of a 13 MW unit.

NextEra dethroned Exxon in terms of public market value and captured national attention with potential take-overs.

Tesla’s dominance in the electric vehicle and infrastructure market has gained market appreciation.

ChargePoint went public and revealed a path to $150M in revenue through hardware, services and software products. The firm’s trajectory makes it clear they are going to be the pillar of electrification of mobility for the next generation.

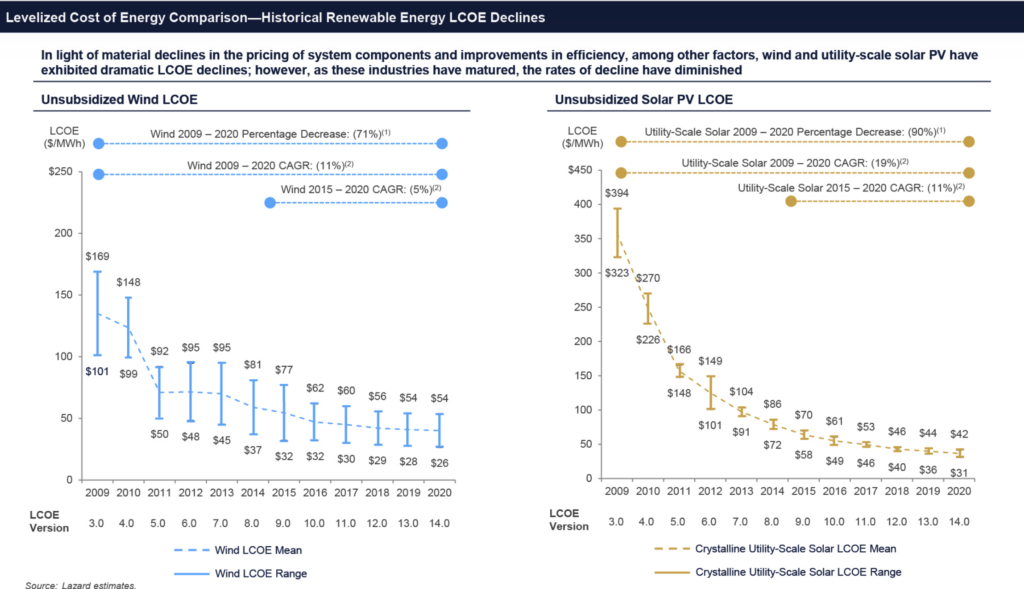

Theme 3: Cost Curves

Over the past decade experts made bold claims about how scientific advancements and engineering accomplishments will drive the cost of new energy products to decline. At times we take this stunning progress for granted. It is worth pausing and recognizing just how far we have come…

The cost for utility scale battery packs are in free-fall: lithium-ion battery pack prices, which were above $1,100 per kilowatt-hour in 2010, have fallen 90% to $137/kWh in 2020. BNEF projects the average price will be closer to $100/kWh by 2023.

Utility scale solar costs dropped by another 5-10% since 2019 and have dropped a cumulative 75% since 2010.

Utility scale wind continues to drop by about 5% a year and has dropped 71% since 2010.

Honorable Mention

JOBS: I actually do not believe the jobs topic gained enough coverage in 2020. The reason? No political party can take credit. The jobs created in industry are primarily due to corporate conviction and bottom-line decisions. Climate, renewables and the energy transition are being incorporated into P&L decisions. This is great for the industry but may mean the more easily trackable climate/energy transition jobs are less direct/trackable.

POLICY: We should have more insights into our congressional composition by February. I suspect policy will have a big impact in 2021.

In Summary …

We are still at the stage of market where the infrastructure layer has major runway. The dollars and assets going to the development and hardware space are going to reshape our energy landscape for the next 50 years. VC investors all want to run to software, but there is still tremendous growth and (near-term) margin in the infrastructure and hardware layer.