The times they are changing… for the better. Late last week, Energize announced that we hired Lauren Densham as our Head of Impact and ESG. Lauren comes to us from KPMG, where she was most recently a Director of Infrastrucutre & ESG Strategy. In that role, Lauren brought a corporate strategy mindset to the public sector, helping infrastructure owners to evolve their strategies and maximize impact. She also spent time advising investment firms on their strategies in the space.

This new role is a natural fit here at Energize. We believe that the top tier, next generation asset managers will embrace the impact potential of their portfolio, and accordingly track and improve the ESG metrics for each company. At Energize we believe that great returns and great impact are aligned and sacrifices are no longer required to independently attain each return target. When we were evaluating the landscape of clients, Lauren quickly rose to the top of the list. She quickly grasped the opportunity that early stage investors can play in helping establish consistency and centrality in the metrics and targets that our industry aspires to achieve.

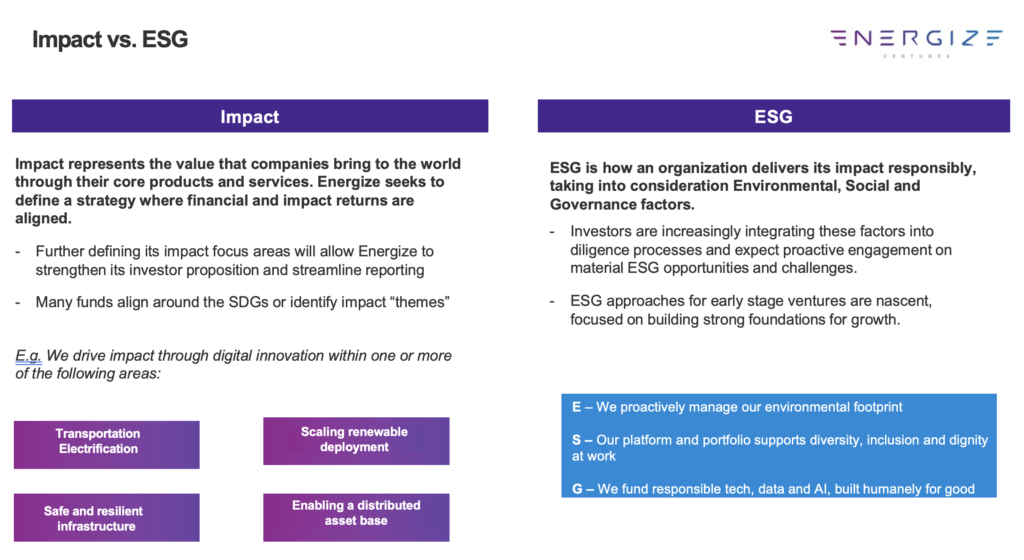

One of my favorite recruiting strategies is to have candidates help define both their role and the success of the role. Energize is (currently) a small team early on in our journey. At this stage we need professionals that can both create and own the upside potential for their area of expertise. During the interview process, Lauren began educating our team and the page below was the start to her framework. So many individuals intertwine “Impact” and “ESG” and this chart shows the purpose of each area.

What happens next with Lauren here at Energize?

She is already going full-speed with us here and you will see a lot of research, data, and planning coming from our team on this topic in the coming year. In her role, Lauren is going to help our investment team track ESG metrics and hurdles in our investment process. She is also going to help our portfolio companies set their impact strategies and track and improve their ESG metrics. As if that isn’t enough, Lauren is also going to help these firms and other stakeholders in the Energize ecosystem more consistently message our aligned ESG metrics so that the impact investing thesis can be aligned towards a real, tangible definition of success. At Energize we encourage our entrepreneurs to “own the problem” and become associated with delivering a technology/solution that serves a market movement. With Lauren, we intend to grow into that impact leader role by delivering impact strategies to our portfolio and creating and executing an ESG best practice playbook for our budding ecosystem. Given Lauren’s experience and teamwork attitude, I am excited for you all to follow her lead on this theme.

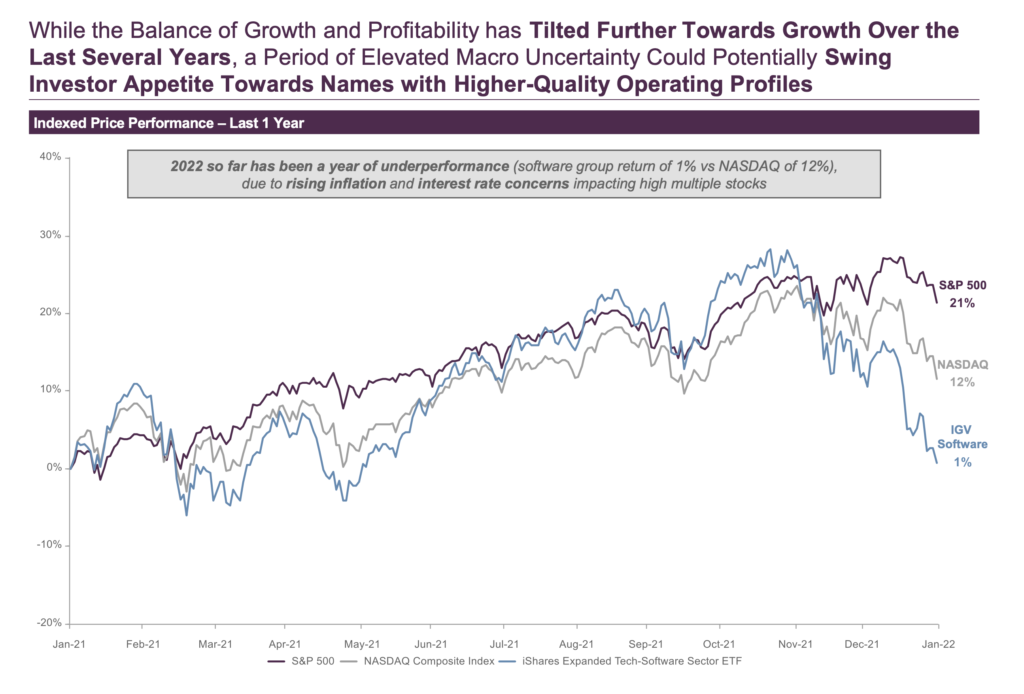

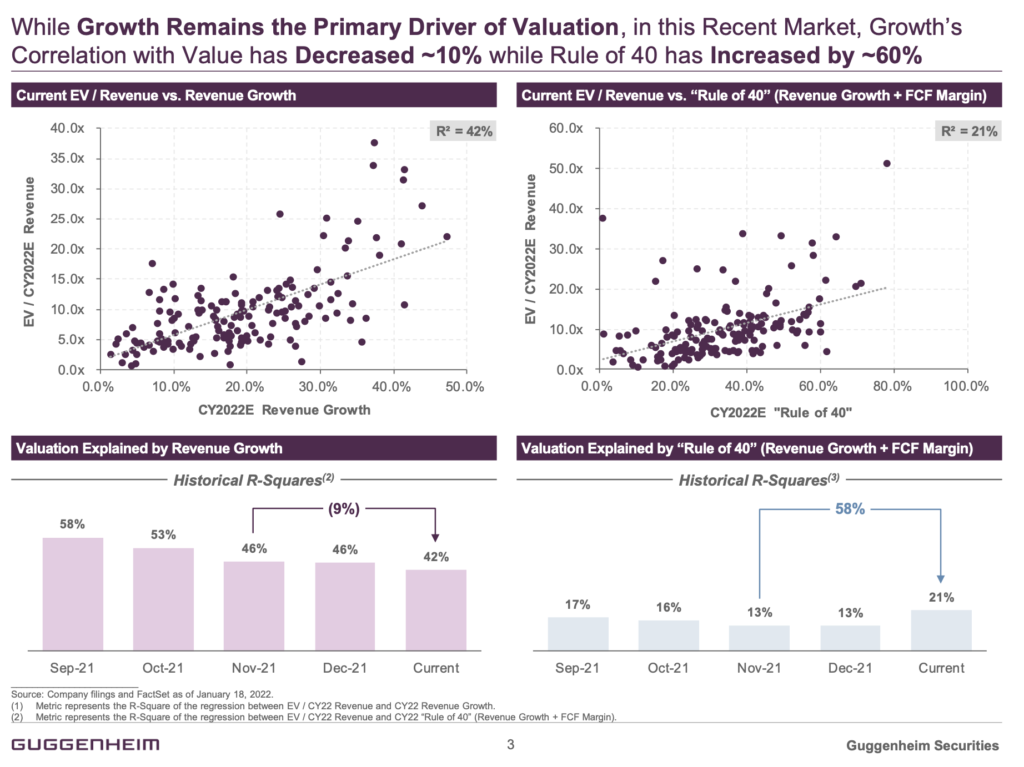

Over the past year, the markets have gone all-in growth and a “growth-at-all-costs” drove valuation multiples higher. Well, for a number of reasons, the market’s position on growth has somewhat broken free from that unconstrained mentality.

Guggenheim releases a great monthly report on these market trends and the takeaways on the second page below show the most important update: the market is finally re-aligning to cash efficient growth. At Energize we like to say either “Cash is King” or “Cash Efficiency is King” … so we welcome some of this return to normalcy.

My two cents on the commentary: Two of the largest industries in the world are colliding: mobility and digitization. 40% of the cost of today’s cars are electronic systems and 90% of cars sold in 2022 will be internet connected. The application layer to serve the drivers or owners of these vehicles is taking off, and Smartcar’s API plays a foundational role at connecting these applications to the car, and driver. Applications in EV charging, insurance, new mobility business models are all emerging, and Smartcar is enabling that growth. With this investment I joined the board and am thrilled to work alongside the legends of Bill Krause (now with Andreessen Horowitz) and Forest Baskett of NEA.

Sahas and Sanketh are the type of founders you dream about partnering with as an investor. Smartcar is their passion and they saw the future of mobility well before anyone else. They have the bold goal of wanting to advance the mobility ecosystem and Team Energize is going to do everything we can to help them accomplish their goals.

Why We Invested in Smartcar

Energize Ventures is proud to lead the $24 million Series B investment in Smartcar, the API developer platform for connected vehicles. Existing investors Andreessen Horowitz and New Enterprise Associates (NEA) also participated in the round. Energize Ventures managing partner John Tough will join the Smartcar board of directors and principal Eileen Waris will join as a board observer. This investment marks Energize’s fourth investment in the future of mobility.

Today’s vehicles are driven by data

The automotive industry is undergoing a period of rapid technological change.

Vehicles are evolving to provide better performance, comfort, and convenience—all while auto manufacturers are facing environmental pressure to reduce emissions and transition towards electrification. Driving this shift are innovations in software and an increasing number of electronic components in vehicles.

More and more, cars are resembling computers on wheels. Never has this been more clear than now, as the auto industry grapples with new car shortages and production halts caused by a heavy reliance on increasingly scarce semiconductor chips. Today, more than 40 percent of the cost of a new car can be attributed to its electronic systems. These systems are spitting off hundreds of gigabytes of data per car per day, creating rich fodder upon which an ecosystem of connected car applications can be built.

For developers working with this data, integrating across dozens of brands’ operating systems is repetitive and tedious work. Smartcar offers a developer-friendly suite of APIs making it easy for businesses to seamlessly connect apps to cars across 22 different vehicle makes with a single integration point. This is the largest selection of any connected vehicle API, providing access to 112 million vehicles globally.

Smartcar’s customers build software applications that leverage data or create actionable outputs from the functionality of the Smartcar API network. Examples of Smartcar’s rapidly growing customer base includes developers of applications that verify vehicle mileage, issue digital car keys, manage EV charging, track fleets, track driving behavior, and more.

The electric vehicle ecosystem will require a software backbone

At Energize we invest in solutions that further the energy transition. When it comes to electrification of transportation, we’re still just getting started. As electric vehicle adoption scales, the load burden on the power grid becomes greater. In order to achieve the full decarbonization potential of electric vehicles, we need to unlock managed charging—and Smartcar’s API platform is the key.

Managed charging refers to the utilization of electric vehicle batteries to optimize the flow of electricity and reduce emissions. This means charging up when renewable energy supply is high and pausing charge when demand on the grid is high elsewhere or when renewable output it low— all while making sure you’ve got a full battery in time for your morning commute.

This balancing act requires utilities, consumers or third parties to remotely control the charging process using software applications—something that is now possible thanks to Smartcar. Through their API platform, solution providers can remotely measure a vehicle’s state of charge and overlay that with real-time grid performance to determine optimal charging time. They can then leverage Smartcar’s charge/discharge function to control the charging process. This leads to higher grid efficiency and enables more renewable energy to be directed towards the world’s growing fleet of electric vehicles.

Built with developers in mind

Smartcar was founded in 2015 by brothers Sahas and Sanketh Katta. While attempting to build a software application for connected vehicles, the two discovered a gap: there was no standard way to connect applications across multiple OEM interfaces.

The cofounders created a developer-friendly API platform to minimize the work and frustration of building, integrating, and launching applications across multiple car brands. Their suite of APIs enables developers to build new products and services and their Smartcar Connect platform streamlines user consent so that customers can safely and securely authorize applications to access data generated by their vehicles. When they began building the Smartcar platform, fewer than 20 percent of new vehicles were connected vehicles. In 2022, 90 percent of new cars will be connected vehicles. As the digital ecosystem around connected vehicles grows, their solutions will pave the way for developers to build the future of mobility.

What’s next for Smartcar + Energize

Smartcar will use this fresh round of funding to further improve their platform and secure their position as the leading API platform for connected vehicles—building new capabilities and better developer tooling to unlock new functionality in the world of connected vehicles. They will continue to grow operations in the U.S. and accelerate expansion in Europe, adding more makes and models to reach even more connected vehicles.

Earlier this week I flew down to the Nozomi Networks 2022 SKO (“Sales Kick-off”). The event, a 4-day gathering, including great talks from company and industry leaders. I was excited to be the voice of the investor and spoke to the company’s sales & marketing teams for about an hour. I really enjoy speaking to sales teams. Why?

The phrase “product sells itself” is not true when you are selling to enterprise accounts. Even the best products require great sales execution: from demand generation, pre-sales, proof of concepts, sales conversion, post-ops, and account management. Sales teams at Nozomi, along with most of the companies in our portfolio, are global. These primarily distributed teams rarely get unified time. This is the SKO’s impactful opportunity: where the company mission, culture, goals, lessons,… and compensation structures can be communicated.

I believe most start-ups begin having SKOs far too late in their development. Alignment for a growing sales team on customer messaging, company values, product roadmaps, successful and failed sales stories… this is how the fabric of a revenue operation grows. I had my first talk to Nozomi back in 2017 when there were 10 people in the room. This year Nozomi had over 100 in the room or dialed in. Building a values-aligned (and non-mercenary) sales team elevates a company’s likelihood of commercial success and is a great investment of internal resources. My guidance is for our portfolio to start those SKOs early, and have them every 6 months into perpetuity.

Here Comes The Sun: How Software Makes Solar Energy More Profitable

The first wave of solar innovation was focused on getting costs down. Now, the industry must look to software and automation to unlock the next phase of growth.

The solar industry is massive – and still growing rapidly

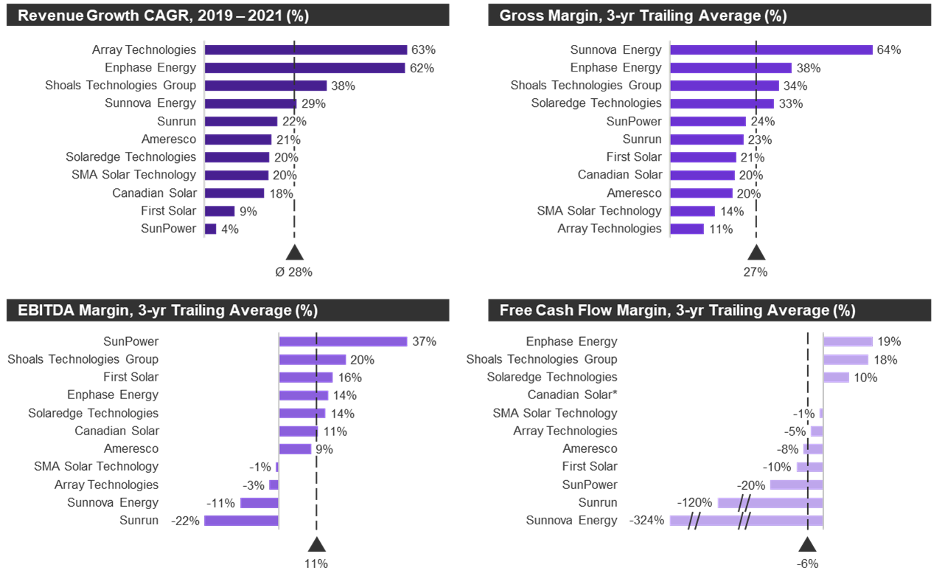

Solar is a $100 billion industry by enterprise value in the U.S. alone. In 2021, the solar industry installed 191 GW globally, more than six times the scale from 10 years ago. In that time, lighthouse success stories have emerged in the public markets. As of 2021 year-end, there are handful of solar companies publicly listed on U.S. stock exchanges with a total combined enterprise value of $86 billion, according to data from Pitchbook. Among them are Enphase, First Solar, SunRun, Sunpower, Shoals Technologies, Sunnova, and Array Technologies. Several large privately held firms focused exclusively on solar or with large business units devoted to the sun are achieving success as well.

Despite its exponential growth, the solar industry is still in the earliest of innings. In the U.S., less than 2 percent homeowners have installed solar on their rooftop. Solar accounts for only 3.4 percent of global energy production today. That figure is expected to increase tenfold or more by 2050. Even with further cost declines across the value chain, solar could easily become a multitrillion industry globally over the coming decades.

So, what could possibly slow it down? Despite impressive topline revenue and unit growth, many solar companies struggle with profitability. From 2019 to 2021, the top 10 public U.S. solar companies by market cap generated a median gross margin of 27 percent, EBTIDA margin of 11 percent and free cash flow (FCF) margin of -6 percent … not quite yet cash flow generating machines.

Many private solar companies face similar financial challenges as their public peers, including low gross margins and high OpEx budgets to drive growth, therefore requiring large amounts of cash to fund marginally profitable operations. Although significant negative cash flow is not uncommon among early-stage, venture-backed companies focused on building a product, developing customer relationships and scaling revenue, we’re seeing solar players up and down the value chain face similar challenges when it comes to achieving scale and profitability.

The primary challenges solar faces today:

Solar customer acquisition is insanely costly, especially here in the U.S.

Solar financing innovation has stagnated since early pioneering efforts in third-party ownership and solar loans

Interconnection permitting is crippling close rates, whether large-scale solar connecting to the transmission network or small-scale solar feeding local distribution power lines

Utility-scale solar developers need more than headcount, with talent shortages and lack of streamlined processes threatening future scale

The solar industry’s best chance to continue its torrid growth, while concurrently flipping on the profit spigot, is to embrace software and automation.

In particular, there are four software-based innovations I believe will transform the solar value chain:

Machine learning software can help automate and lower costs of customer acquisition

Customer acquisition is the single largest contributor to solar soft costs. In 2020, U.S. residential solar companies spent between $800 million and $1.5 billion on sales and marketing alone. Much of that expenditure still resides in traditional techniques such as cold calling, door knocking, radio ads, and the like. With homeowners spending $20,000 or more on residential solar arrays, there is no doubt that buying solar is a significant financial decision – and one that requires a human’s touch prior to close. However, I believe a considerable portion of the upfront customer qualification, lead generation, initial sales interaction and formal proposal generation can be done digitally, remotely, and much more efficiently.

Energize portfolio company Aurora Solar recently launched a groundbreaking new product that leverages satellite data, computer vision and machine learning models to identify optimal solar customers. Innovation like this will be key in solving solar’s customer acquisition cost problem.

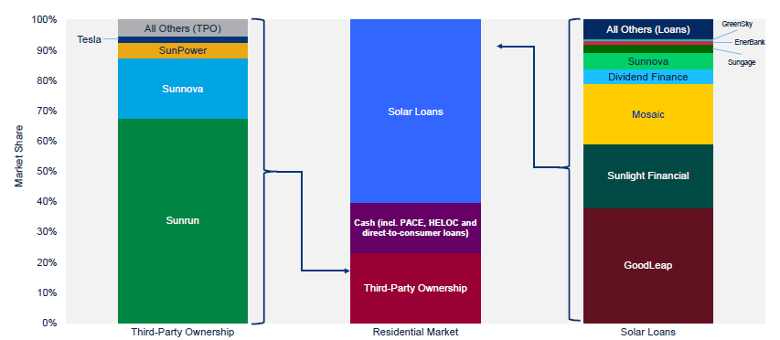

The solar financing market is ripe for disruption

Most U.S. residential solar projects employ financing of some form. As of 2021, cash purchases account for less than a fifth of all projects, while loans and third-party-owned Power Purchase Agreements (PPAs) are utilized in a majority of cases. The solar financing opportunity is lucrative, and a host of increasingly large-scale, dedicated solar financing companies have emerged, from GoodLeap and Mosaic for solar loans, to SunRun and Sunnova for PPAs.

However, a lack of innovation in solar financing over the past five years combined with low interest rates has led to excessively high financing costs being passed through to the customer. Solar loans, for example, have an average origination fee as high as 15 to 20 percent. This fee goes to cover things like customer acquisition, underwriting analysis, and kickback to the installers that bring financiers deal flow. Put into perspective, home mortgage dealer fees range from 0.5 to 1 percent, while auto loan origination fees (a similar ticket size purchase) range from 1 to 2 percent. Today, most solar financiers employ complex structuring techniques that ultimately benefit the financiers and the installers they provide kickbacks, at the expense of the customer.

Solar financing represents a ripe opportunity for software innovation. Employing a more transparent sourcing approach and data-driven underwriting that reduces loss ratios could bring these fees down to as low as three percent for the solar customer. Dramatically lowering solar financing costs would improve the accessibility to a broader demographic group, encouraging more widespread adoption. At some point, a software-enabled disruptor will see the vast amounts of revenue generated by leading solar loan providers as an opportunity that can’t be ignored.

Simulation techniques can drastically improve interconnection inefficiencies

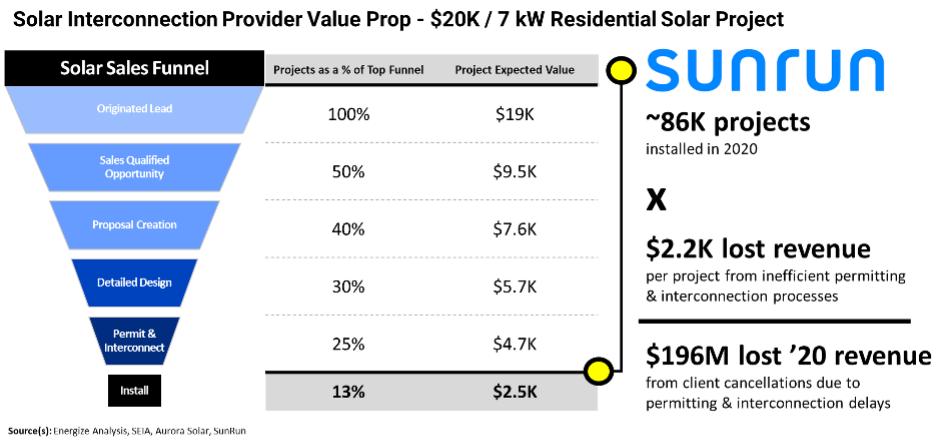

Getting solar energy connected to the existing power grid is not easy nor cheap. Nearly half of residential solar customers cancel their solar purchase due to delays in permitting and interconnection. Large-scale solar farms in the U.S. currently wait two or three years for interconnection to the transmission network. As a result, only 25 percent of proposed solar projects that apply for interconnection ultimately make it to commercial operation.

Why? Utilities and transmission operators must evaluate and study renewable energy interconnection to ensure power grid reliability before approving any interconnections. Unfortunately, this process is anything but efficient – relying primarily on manual engineering efforts and outdated analysis tools. The slow and clunky interconnection process can have a significant impact on solar providers’ bottom line. In our own analysis of SunRun, we estimated $200 million of revenue lost due to interconnection and permitting delays. Add to that another $30 to $50 million in customer acquisition costs for projects never installed, and we’re looking at a potential net profit loss between $70 and $100 million.[1][LK1]

The good news is that readily available software tools that leverage cloud computing advances and AI-based simulation techniques can compress weeks or months of analysis time to minutes. If you’re interested in learning more about software innovators addressing interconnection, this blog post covers the topic in detail.

Utility-scale solar developers finally adopt software and automation at scale

Utility-scale solar developers have traditionally been slow to adopt dedicated vertical solar software. Most firms have employed a mix of home-grown applications with off-the-shelf software from legacy vendors or new cloud-entrants. Oftentimes, these tools are combined with in-house customization and bespoke integrations.

Instead of investing in software and automation, fast-growing solar developers have responded to rapid growth with equally rapid hiring. Careers in engineering, supply chain, finance, legal and data science have boomed in the large-scale solar industry. More jobs in solar is a win-win, but hiring is not the solution for achieving long-term scale and sustained growth, especially with talent wars at an all-time high. The solar industry simply cannot scale to the level needed to meet U.S. clean energy goals by relying on headcount growth alone.

So what is the solution? Dedicated, holistic efforts to embed software and automation that is tailored for the utility-scale solar value chain. Some examples:

Satellite-based computer vision techniques to rapidly assess land feasibility for solar

Purpose-built engineering and design software that incorporates the nuances of large-scale solar farms like land grading, vegetation and local weather patterns

The latest technological advances such as bifacial modules, advanced tracking systems and novel inverter technology

We have seen early signals that leading solar developers are dramatically expanding IT and analytics budgets, from single digit millions to tens of millions of USD annually for the largest firms. A solar software unicorn could be built by solely focusing on utility-scale plants – the recent acquisition of AlsoEnergy by Stem for $695 million is a recent indicator that we are close!

The sun also rises

Solar’s first wave focused on bringing PV module and power electronics equipment hardware costs down through materials R&D and manufacturing scale. The second wave will be about embracing innovative, customer-friend business models to stimulate adoption by homeowners, businesses, and power companies. My prediction: solar’s next wave of winners will be defined by embracing software to generate profitable growth as the industry matures.

[1] These are Energize’s own estimates and are based on nonproprietary, publicly available information.

Blackstone Invests $3 Billion into Invenergy Renewables

On Friday Invenergy announced a $3 billion minority, growth equity investment from Blackstone. Existing capital provider, CDPQ, and Invenergy management retain majority control, and Invenergy’s management remain in control of all operational decision making. The press release can be found here. Invenergy was a founding partner to the Energize Ventures story. The Invenergy cofounders, Michael Polsky and Jim Murphy, have seats on the Energize investment committee and provide me with invaluable firm-scaling insights.

Blackstone is at the pinnacle of private markets investing. Blackstone has traditionally focused their infrastructure investments on the traditional hydrocarbon markets, but that focus is changing. The firm has actively discussed (as recently as their Q3 earnings announcement) their intent to deliver more capital to the energy transition.

On ESG. So, what I’d say on that is I think the most relevant areas for us are three areas. We actually talked about this at our Board meeting this week. In the energy credit and energy debt areas, if you went back in time, there was much more orientation toward hydrocarbons and E&P. That — a lot of those activities we’ve deemphasized in a significant way over the last 3 years or 4 years. And we’ve been doing much more around the energy transition and have great success. We announced a big transmission line of hydro-power from Quebec to Queens a few weeks ago. We put an investment into a public company called the Array Technologies, which moves solar panels. We did a preferred with warrants. So, we’ve had a lot of success in that state.

And I would expect the next vintages of our energy equity and energy debt funds will be heavily oriented toward the transition, toward sustainability. I think investors will react well. And I think similarly, we’ll do more in infrastructure, another way investors can play it with us at Blackstone. So, there is a lot of investment demand. And then I would say in some of our more liquid structures and areas, some of the things we do in insurance on asset backs, I think you’ll see more there. So, I think overall as an asset class, the demands for capital are enormous and I think a lot of it will come from private capital. So, I think that bodes well, but it’ll be expressed at our firm in multiple areas.

Jonathan Gray, President & Chief Operating Officer @ Blackstone

Invenergy Renewables is now one of the largest (if not the largest) privately held renewable energy developer in the world. To-date, Invenergy has built 175 projects totaling 25,000 MW and Invenergy is currently developing the largest wind and solar sites in North America.

With more of Invenergy’s customers: utilities, corporations, banks… all looking to own more renewable assets to meet their decarbonization goals, Invenergy is in a fortuitous position where demand for energy assets exceeds the current development cycles. This investment pairs Blackstone with CDPQ as the two premier capital partners enabling Invenergy’s growth.

The Invenergy team is pleased to welcome Blackstone, a leader in the renewable investment space, as our partner. We greatly value our long-term relationship with CDPQ and are thrilled to continue to accelerate the clean energy transition with Blackstone’s additional investment and capabilities.

Jim Murphy, President & Corporate Business Leader at Invenergy

For Energize, we are quite fortunate. We have had a tremendous learning relationship with Invenergy. We get to learn what technology their engineers need to meet the scale of the renewable energy revolution. CDPQ, a premier pension fund, has also already been a foundational partner for Energize and we continue to learn and provide value to their global footprint. With Blackstone now as a new “cousin” I am looking forward to how Energize can begin to become a thought partner to Blackstone and their infrastructure portfolio. The energy transition is still in the early innings.

Why big financial firms are scooping up climate modeling companies

Energize made an investment in the space in early 2019 when we led the Series B in Jupiter Intelligence. Our belief then was that new climate modeling techniques, enabled by the newest data sources and latest machine learning models would outperform older systems.

As evidenced by this article, the incumbents: mega firms like S&P, Moody’s, McKinsey… they are all scrambling to keep up with the changing expectations of their own customers. Most of the incumbents have now acquired a newer generation technology start-up. The prices for these M&A events range from undisclosed to $2 billion.

We still believe Jupiter is the best of this generation and that they will be a big, standalone company. Here is a snippet from the article on Jupiter.

If you have followed this site, you have seen me post some positive endorsements about Ford. I’ve been quite consistent that I think they are the most proactive incumbent automotive OEM to pivot to the electric vehicle movement. In addition to taking their flagship vehicles and making them EVs (Ford F-150 and Ford Mustang) the firm also made a commitment with Sunrun to deliver full-home electrification solutions. The net is that they are “burning the combustion engine bridge” and making the commitment to electrification.

I think Ford will be successful because they are a trusted brand with a diehard following and they aren’t being subtle about their interest and dollar commitment to EVs.

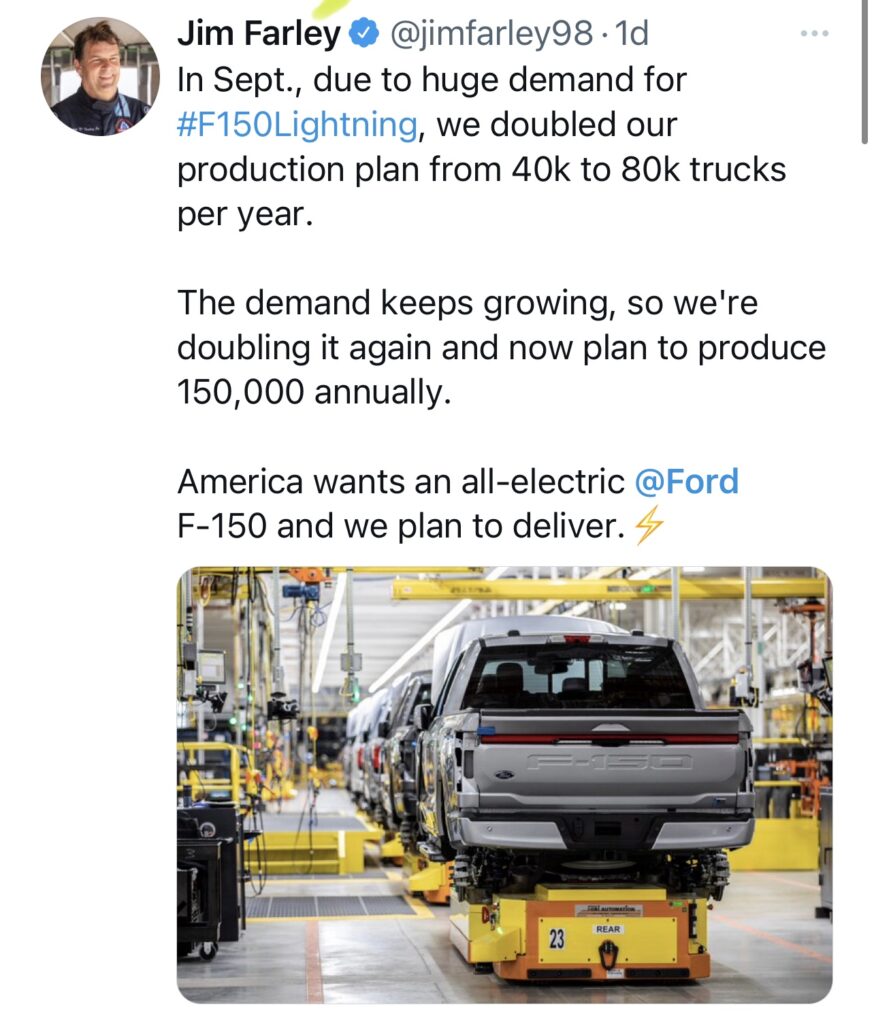

When Ford CEO, Jim Farley, launched the electric Ford F-150, he projected 40,000 cars per year in interest. In September they increased that total to 80,000 vehicles and just yesterday they nearly doubled the figure again: Ford is now building capacity to meet over 150,000 electric Ford F-150s per year.

While Tesla is the undisputed leader in electric vehicles, I think Ford’s trajectory is the most exciting and is going to be the clear #2 player in EVs over the next decade. And they might even make the move to #1. The company’s stock is up 181% in the past 12 months, so I think the market is starting to realize the company’s commitment and opportunity.

Yesterday I wrote about the return profiles for emerging managers. That Pitchbook data showed how emerging, specialist managers outperformed the market. This morning one of my teammates shared an article about how LPs are thinking about Fund allocations in 2022.

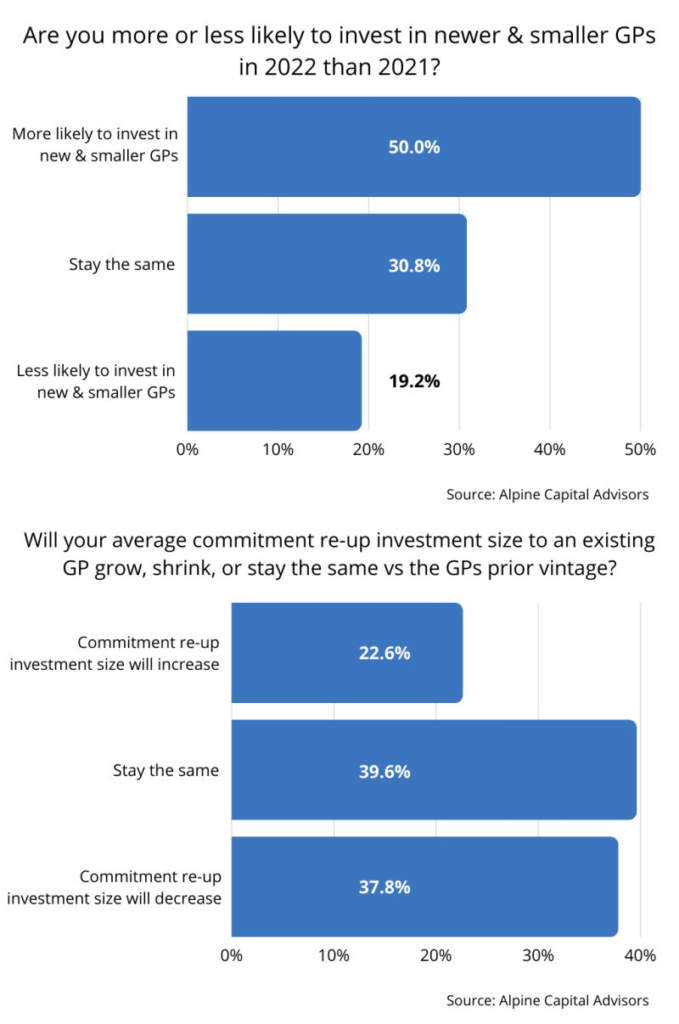

This data, shown below, indicates that LPs are looking to allocate more capital to emerging managers. Given that most investment firms in the broader energy and sustainability markets are on a newer vintage fund, this likely means more capital coming to the sustainability and technology markets. Energize is seeing an increasing number of excellent investment opportunities, so I firmly believe this capital can be deployed successfully over the coming years.

Performance and Fundraising Progress of Emerging Managers

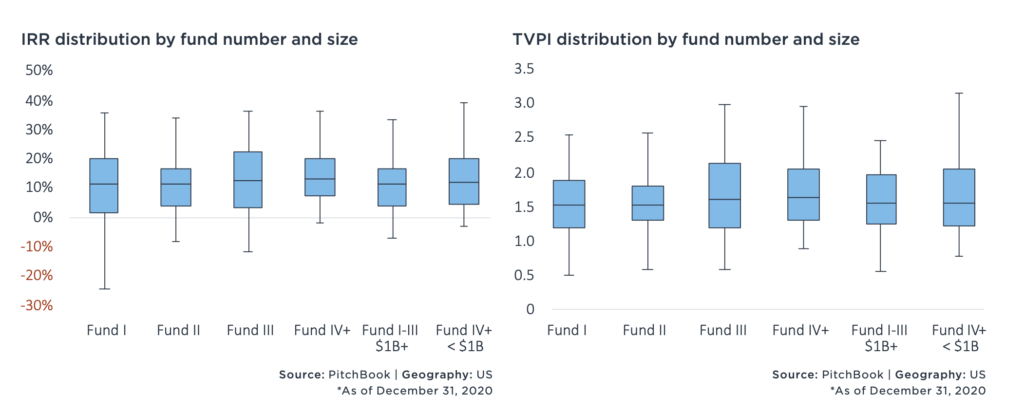

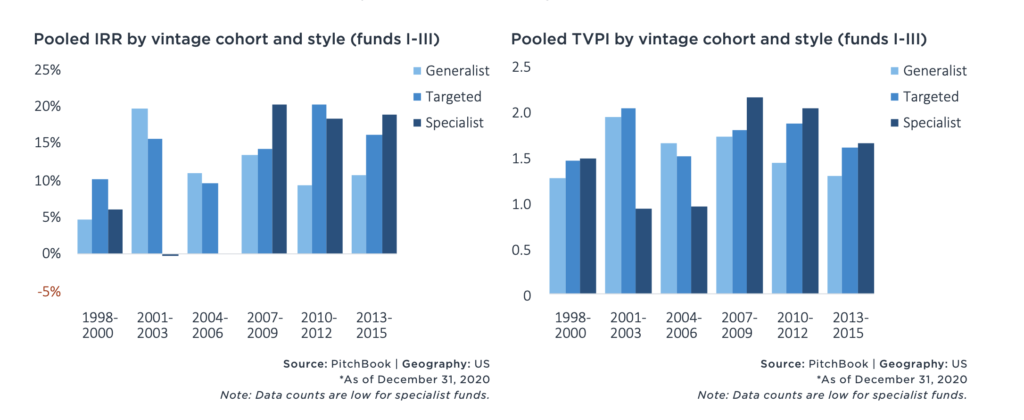

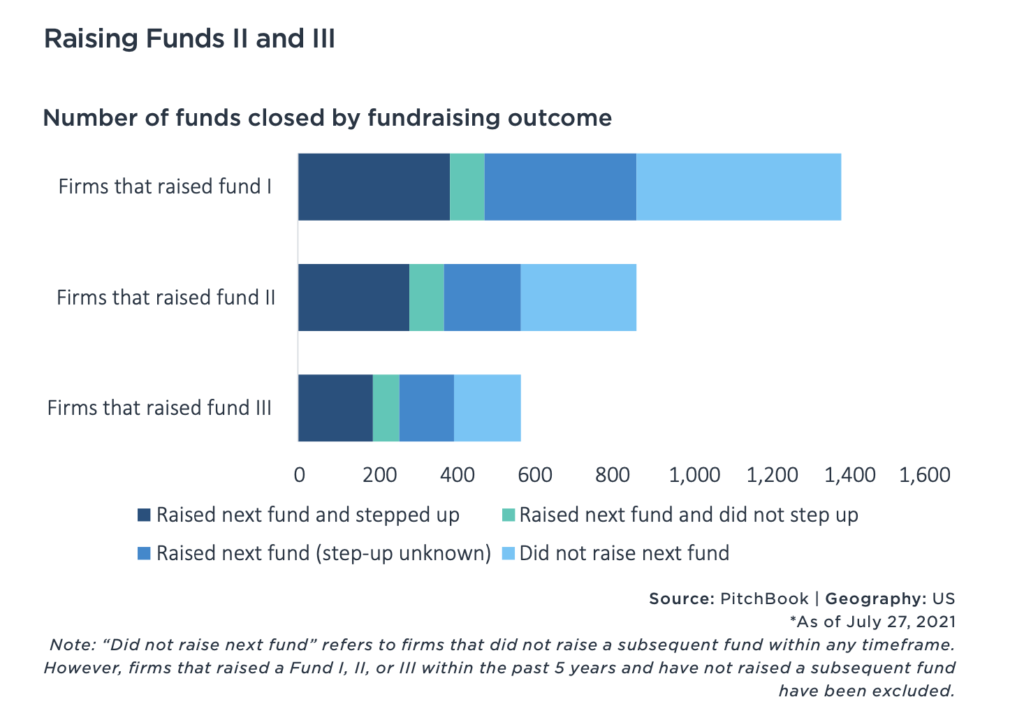

I saw an analysis recently on performance details around “Emerging Managers”. Emerging managers are investment firms, like Energize, that are in the first 3-4 flagship funds, and within 10 years of founding. Most of the below data came from Pitchbook, a data platform owned by Morningstar. The key takeaways are below:

• Contrary to conventional wisdom, there is little differentiation in step-ups between larger emerging manager funds ($500 million+) and smaller funds.

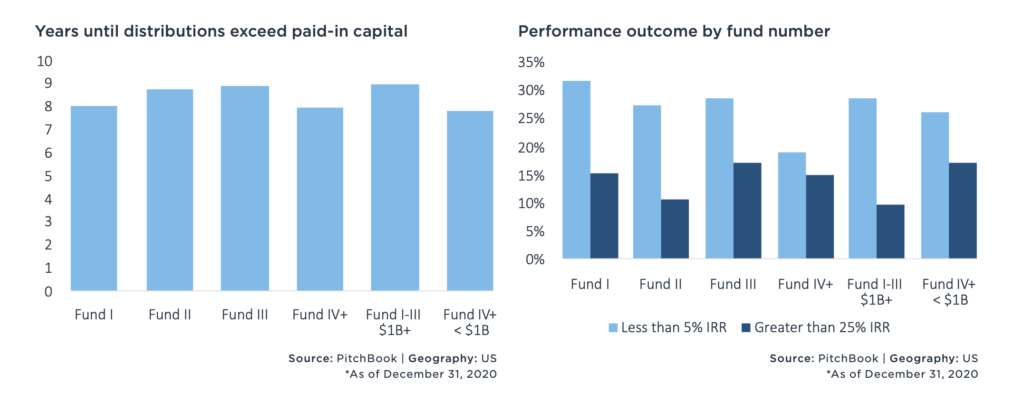

• Also contrary to conventional wisdom, emerging managers do not consistently outperform established managers, although there are some nuances. First funds exhibit the most performance variation, while second funds underperform and third funds slightly outperform. However, these trends vary significantly by vintage. Very large emerging manager funds ($1 billion+) perform in a tighter band, with less outperformance. Additionally, first-time funds return capital more quickly than second and third funds.

• Since the global financial crisis (GFC), specialist emerging managers have outperformed generalists. (This point is a pillar for Energize – industry expertise and access is a big driver of our returns)

• At each stage of progressing from Fund I to II, III, and IV, about one-third of managers fail to raise the subsequent fund. The success rate for subsequent fundraises increases modestly as fund number increases.

• Because managers often begin fundraising well before they have realizations from their previous fund, LPs primarily look for persistent strategy execution when deciding whether to reup with an emerging manager. Failure to raise a subsequent fund can often be traced to early portfolio losses or key personnel turnover. (Do what you told your LPs would do!)